Political risk continues to override fundamentals

Outlook:

The euro hit the high of the year so far on Monday at 1.0627. This fails to match-and-surpass the previous high at 1.0654 from Dec 30, but never mind. A retreat from the Mon-day high is normal, on either profit-taking or plain old position-paring. We can even image a drop as low as 1.0460 or so before the euro resumes the upmove. Or breaks out to the downside.

The pullback-within-a-pullback is only partly influenced by fundamental factors like the 10-year yield recovering a little. Pullbacks are generally a function of position adjustment by the big traders, as we wrote yesterday. We don't have volume data in FX as we have in equities to help judge, but we can bet that when the CFTC reports today's futures positions late Friday, we will see a big reduction in euro shorts.

Political risk continues to override fundamentals. In Mexico, the peso fell hard yesterday by almost 2% to another record low and the central bank admitted they had spent $2 billion last week intervening to prevent further devaluation. The WSJ reports the peso is down 15% since the Nov election, the benchmark equity index is down 5.3% and the 10-year yield has jumped to 7.76% from 6%. Trump's words get all the blame. We don't yet have any actual policies or actions. "Foreign investors were net sellers of $1.4 billion in Mexican short-term debt in December, reducing their holdings by 11.3%, according to data from Natixis and Banco de Mexico. That was the biggest one month selloff in nearly 10 years in percentage terms."

Is it overkill and a bottom-fishing opportunity? Not yet. Some 80% of exports go to the US and 30% of GDP comes from trade with the US. The Mexican economy could contract as much as 3.3% this year (after gaining 2.1% last year). Of course, Trumpism could backfire, cutting Mexican imports from the US and setting off more illegal immigration. And unlike 1995, the US would not rush to offer a credit line.

The Turkish lira is worse. Bloomberg reports it has fallen 8.6% "against the dollar in the year's first eight trading days, adding to last year's 17 percent slump. It's set a new record on six of them. The pace of the depreciation has been so steep, it's left all other major currencies trailing in its wake: the next worst-performer of 2017 has been Mexico's peso, and it's weakened about half as much." Devaluation pushes inflation. CPI is 8.53% in Dec, more than 3.5% over the central bank target and the 6th year the target has been missed. One big bank foresees 12%. So what's wrong with the central bank? Political interference. "With the economy contracting for the first time in seven years in the most-recent data, the central bank, led by governor Murat Cetinkaya, is under pressure from politicians including President Recep Tayyip Erdogan to support growth. They've made statements the traders are reading as a commitment not to raise rates, setting up the lira as an easy short."

In the UK, fairly good economic data had pushed the pound up from a spike low at 1.1950 on Oct 7 to a high of 1.2775 on Dec 06, about two months later. But the storm over hard Brexit started by PM May's weekend comments brought hard Brexit fears roaring back and today the pound hit a low of 1.2097, the lowest since Oct 25. It may wobble and waver before breaking the previous low, but a break is almost certainly in the cards. Even the normally astute Economist magazine can't find plausible reasons to rebut the idea that May is muddled. What does she stand for? She has already had to pull back on half-hearted social "fairness" initiatives.

And we consider Japan's demographic problem a somewhat political issue, too, although it's more a sociological one. Japan's birthrate is insufficient to replace those dying, and the country is losing one million persons per year. Other countries have lower "fertility rates," including Germany, but they have immigrants to keep the numbers up. The average age in Japan keeps rising, and one-third of Tokyo is already at pensioner age. The Economist says it's the oldest country in the OECD. Evidently Japanese men are lousy husbands, not to mention dictatorial mothers-in-law, and young Japanese women just say no. Public opposition to immigrants is stubborn. Not to be too simplistic, but economic growth depends on a growing labor market and in Japan, the labor market is shrinking. We can picture an empty country in which manufacturing and services are provided by robots and the only market for goods is overseas. When this is the trend, the country absolutely, positively needs a really weak currency.

What will happen to financial markets when Trump is actually in office? Well, nobody really knows but do know to expect a trainwreck. This is not to say the current dollar move lower can be attributed to Trump Terror. We continue to think it's position adjustment from the earlier over-enthusiastic embrace of the reflation trade. But having said that, we can't expect a dollar recovery and talk of euro parity until the yield pullback is over, and that could take one or more quarters. One Swiss banker said on TV he doesn't see the yield really making solid gains until June. Oh, dear.

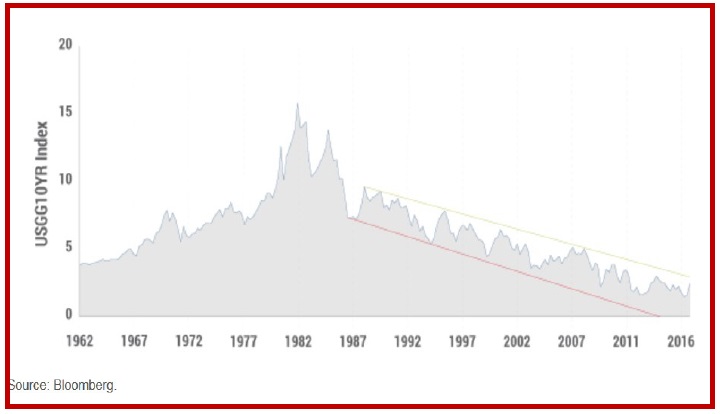

Let's consult Bill Gross. He says the long-running secular move down in yields is still in place. It must get broken to the upside. "....this super strong, frequently tested downward trend line is at risk of being broken. 2.55% to 2.60% is the current "top" of this trend line, and over the past few weeks it has held and reversed lower by 15 basis points or so. BUT----------. And this is my only forecast for the 10-year in 2017. If 2.60% is broken on the upside – if yields move higher than 2.60% – a secular bear bond market has begun. Watch the 2.6% level. Much more important than Dow 20,000. Much more important than $60-a-barrel oil. Much more important that the Dollar/Euro parity at 1.00. It is the key to interest rate levels and perhaps stock price levels in 2017."

Notice he says "if." And does not give a timeline. We find this very worrisome. It suggests the dollar in some kind of choppy limbo for months to come.

Gross writes that "30 basis point declines on average for the past 30 years have lowered the 10-year from 10% in 1987 to the current 2.40%." It's going to take more than animal spirits because of a new president to change that line.

Politics: The intelligence br iefing last week to Tr ump, Obama and senior Congr essmen contained a two-page summary of unsubstantiated reports from a former MI6 spy on "compromising and salacious information" collected by Russia during Trump's visits over the past five years. Putin and Trump deny it but the report is widely believed and it was already leaked by BuzzFeed. We await editorials.

It's not just disgraceful behavior on the sidelines of the beauty pageant. It's also claims that Trump knew all along about the Russians hacking the Dems (and didn't disclose or protest) and discussed business deals in return for going easy on Russia over Crimea. It's interesting that such a story would be dismissed immediately if it were about Obama, but we are all too willing to believe it's true about Trump.

The big story today is supposed to be Trump's press conference as which he will announce measures to avert conflicts of interest. Dream on. He doesn't have any. Self-aggrandizement is the only agenda. A small offset is the Congressional vetting of Tillerson for Secretary of State. He is likely to comport himself well. But offsetting is Trump appointing his son-in-law as a White House advisor in direct defiance of the anti-nepotism law from 1967. There is a court judgment that First Ladies are exempt and Trump's lawyer is trying to widen the loophole. The problem is that the guy seems sane and the only person Trump listens to, so a much-needed check on Trump's recklessness.

| Current | Signal | Signal | Signal | |||

| Currency | Spot | Position | Strength | Date | Rate | Gain/Loss |

| USD/JPY | 116.34 | SHORT USD | WEAK | 01/05/17 | 115.93 | -0.35% |

| GBP/USD | 1.2132 | SHORT GBP | WEAK | 12/16/16 | 1.2444 | 2.51% |

| EUR/USD | 1.0522 | LONG EURO | NEW*WEAK | 01/10/17 | 1.0587 | -0.61% |

| EUR/JPY | 122.42 | LONG EURO | STRONG | 11/03/16 | 114.30 | 7.10% |

| EUR/GBP | 0.8672 | LONG EURO | WEAK | 01/09/17 | 0.8649 | 0.27% |

| USD/CHF | 1.0198 | SHORT USD | WEAK | 01/05/17 | 1.0113 | -0.84% |

| USD/CAD | 1.3227 | SHORT CAD | STRONG | 01/05/17 | 1.3253 | 0.20% |

| NZD/USD | 0.6995 | SHORT NZD | STRONG | 12/19/16 | 0.6963 | -0.46% |

| AUD/USD | 0.7382 | LONG AUD | STRONG | 01/05/17 | 0.7343 | 0.53% |

| AUD/JPY | 85.88 | LONG AUD | WEAK | 10/06/16 | 78.48 | 9.43% |

| USD/MXN | 21.7787 | LONG USD | STRONG | 10/31/16 | 18.9054 | 15.20% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat