Italian Referendum: Yes or No to Renzi? More political turmoil for the markets?

An Introduction to the Italian Referendum: Yes/No camps, polls and market reaction

Next December 4, Italy will vote on a referendum to reform its constitution. PM Matteo Renzi seeks to strengthen the power of his government by making it easier to pass laws.

Captaining the ‘Yes’ campaign, Renzi has made this referendum as much about his person as it is technically about reforming the Italian constitution.

On the opposide side, several parties are asking for ‘No’ as a harsh critic to a bill they claim to be badly written and that it would make the government too powerful.

The referendum might be read by the markets as another potential political turmoil event, with Brussels and the European leaders worried that a ‘No’ could add further problems to the European Union crisis already fueled by Brexit.

EURUSD and EUR crosses, Italian bonds and stock markets will be broadly impacted by the referendum result.

Polls are showing lately an advantage for the ‘No’ camp, that seems to have opened a bigger lead during the last weeks, according to the following chart.

Source: Wikipedia

___________________________________________________________________________________________________________

Table of Contents

1 Italy decides – will it be Armageddon for European markets?

2 First Brexit, Now Trump, is Italy next? By Dean Popplewell

3 Italian Banks and BTPs: a dangerous liaison, by Edoardo Fusco Femiano, CFTe

4 The Italian Job, by Marc Chandler

5 How Unpredictable Will the Crack Heads be About Italy?

___________________________________________________________________________________________________________

Italy decides – will it be Armageddon for European markets?

Are the markets under-pricing the risk from this referendum, and does it matter for markets? Considering the political shocks that have been delivered in 2016 already, we think the markets would be wise to keep a close eye on Sunday’s referendum outcome. Two things matter for markets, in our view:

1, The No camp wins and this causes the collapse of the current government. If a government cannot be formed then this could trigger an election, which may give the anti-establishment Five Star Movement Party some momentum to secure a larger majority in the Italian parliament. This may trigger a wave of market volatility due to the Five Star Movement’s anti-EU stance in the past.

2, The banking sector: Italian banks are in terrible shape, and had been subject to a bailout plan agreed by Renzi’s government. If he loses the referendum and resigns, then the big question for traders will be if the bailout plan still stands. If not, then eight of Italy’s lenders could be at risk of collapse. Due to the interconnectedness of the global banking system, and the weakness of some other European lenders notably Deutsche Bank, a collapse in Italy’s banking system could lead to intense pressure on global financial stocks in the aftermath of a No vote.

A win for the Yes-camp, could trigger a sigh of relief for the markets, particularly for Italian bond yields, which we would expect to retreat back to the 1% mark, where they were back in August, they are currently just under 2%. We would also expect a large rebound in Europe’s banking shares, particularly Unicredit and Banco Monte dei Paschi di Siena SpA. These banks, in particular, could benefit from a win for the Yes camp as it could facilitate a rapid share pricing for these banks early in 2017.

Is a win for the No camp really that bad?

Even if the No camp wins on Sunday, the market could initially misinterpret the result just as we saw with Trump’s victory in the US, for three reasons:

Just because the Italian people vote No doesn’t mean that they don’t want change, in fact, it could signal that they want a new more reform-minded government than Renzi, especially if a No vote triggers a general election.

Even if the Five Star Movement wins power under a hypothetical election post the referendum, this does not mean that Italy will leave the EU. Italy’s constitution does not allow referendums on international treaties, which could put some investors’ minds at rest.

The Italian finance minister warned that a win for the No camp would not necessarily mean that Italy’s banks would be at risk, as the bailout plan could still go ahead. When it comes to Italian banks, no matter who wins on Sunday, they have a period of painful readjustment ahead.

We would expect further soothing words from Italian and EU officials if there is a win for the No camp next week, which could dampen any spike in volatility on the back of this referendum.

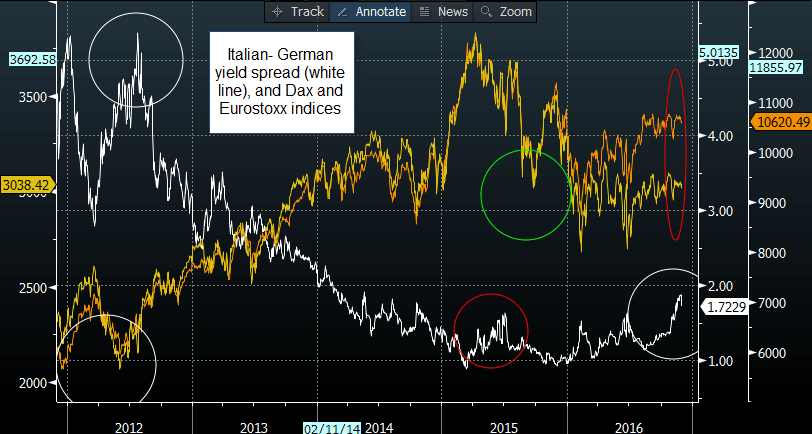

What the Italian – German yield spread could tell us about equities

In terms of market action, the chart below is a good indication of how markets could react to any referendum-inspired spike in Italian bond yields. The chart below shows the Italian – German 10-year sovereign yield spread, the Dax and the Eurostoxx index. Since 2012, the Dax and the Eurostoxx index have suffered sharp falls when this yield spread has spiked. This happened again when the yield spread started to wobble in 2015. In recent weeks, as the yield spread has risen to its highest level since 2014, European stock markets have started to wobble although they have not fallen off a cliff.

Although historical price action does not predict what may happen in the future, one could assume that the same may happen after a win for the No camp on Sunday/ Monday, with a spike in the Italian – German yield spread triggering a decline in Europe’s two major stock indices. Below we go into more detail about specific trading opportunities.

___________________________________________________________________________________________________________

First Brexit, Now Trump, is Italy next? By Dean Popplewell

European policy makers have been warning for months that they see Italy as the biggest risk to the financial stability of the eurozone and the market is beginning to agree with them – 10-year German bund/Italian BTP’s spread has widened to more than +1.6%, the widest it has been in 18-months when the ECB began its bond buying program.

What can investors expect?

Worst-case scenario: PM Renzi’s referendum is soundly defeated which would lead immediately to a period of political instability. He may have two options, either resign (which he promised, but may be convinced not to do) or be forced into a new coalition until elections are held in two-years.

Market reaction: Either choice, capital markets would certainly interpret a “No” victory as further proof that Italy is incapable of reform, raising doubts about the country’s ability to deliver the kind of growth needed to put its debt burden of +135% of gross domestic product on a sustainable footing.

This will put pressure on the Italian financial system. Investors will be reluctant to put capital into the Italian banking system, which in turn could force banks to impose losses on “individual” bondholders (a third of all bank bonds are held by Italian taxpayers). A scenario like this would most definitely ignite a populist backlash that could bring the anti-establishment, anti-EU 5 Star Movement to power in the next general election in 2018 and then Italy’s Euro membership will surely be called into question.

Italy’s banks are drowning in nonperforming loans (NPL’s). Official data puts the total amount of NPL’s, at around €200B, or around +8% of total loans (some analysts peg it higher at +15%).

Simply put, Italy has failed to restructure its banks in a meaningful way and the banking sectors’ problems have only been exacerbated by persistently sluggish economic growth – a low yield environment does not help a banks bottom line.

There is an alternative viewpoint to a referendum defeat, in that the referendum does not really matter. A period of political instability would not be unusual for Italy. Some analysts believe that the market should not worry about a lack of reforms, since PM Renzi’s own reform efforts have run out of steam over the past 12-months and that few expected any major initiatives before the next general election in 2018.

Regarding the banks, the money required to recapitalize the Italian banking system is “small” relative to the country’s GDP (Europe’s fourth largest economy), making it likely that Brussels and Italy could/would find an cordial solution.

Current market thinking is that the truth may lie somewhere in between. Italy will cope with the referendum, while being financially protected by the ECB’s government bond buying program. The ECB conveniently meets a few days after (Dec 8), and the market reaction will most likely dictate whether Euro policy makers need to expand and extend its QE program (fire blanked approach).

Note: A Euro backstop may pressure Rome to reach a compromise with Brussels in its current standoffs over bank bail-ins and its 2017 budget.

However, Europe’s real headache will/could come later. The potential of Italy’s inability to reform would most likely see a changing of the political guard in 2018. For now, current polls put Renzi’s Democratic Party ahead of the 5 Star Movement, but that would all change with his resignation.

A second moment of stress is likely to come whenever the ECB finally decides to remove its “fire blanket,” exposing Italy to the market. When? If the eurozone recovery continues and inflation returns toward its target as expected, the ECB will find it impossible to persist with its QE program and keep buying Italian bonds.

___________________________________________________________________________________________________________

Italian Banks and BTPs: a dangerous liaison, by Edoardo Fusco Femiano, CFTe

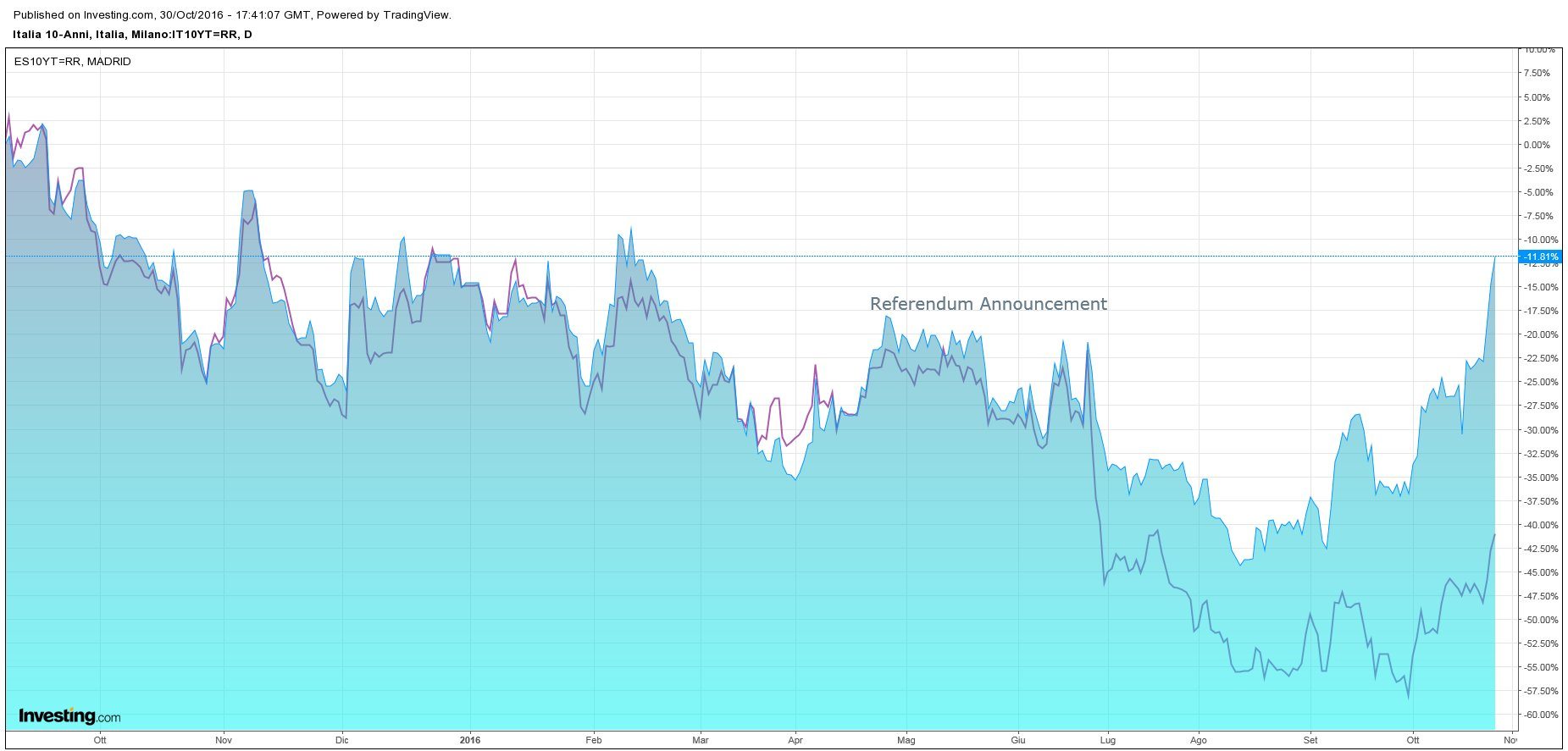

Italian government bonds remain constantly under pressure and the underperformance of the Italian 10Y generic BTP versus the Spanish 10Y generic BONOS, since the referendum announcement day (April 2016), already sent a clear message in that sense.

The credit spread widening of Italian government bonds has also negative implication for Italy's fragile banking system, still trying to deal with the non-performing loans (NPLs) issue, estimated to total 360 billion euros ($400.7 billion). As indicated by the most recent Financial Stability Report (Bank of Italy), since 2008 total foreign holders of Italian BTP’s strongly declined while holdings of Italian banks, insurance companies and the Bank of Italy increased.

Comparing the FTSE Italia All Share banks, the main index on the Italian banking sector, and the 10Y BTP's yield we main find a clear negative correlation, with some time lag. In addition expectations of a limited extension of the ECB quantitative easing program and the uncertain political scenario in Italy are likely to put addtional pressure on yield. In conclusion, the Italian banking industry is going through an intense reshaping of its business model, in some case with a clear need of capital injections. The recent sell-off in the government bonds space, Italian included, is unlikely that will provide some relief.

___________________________________________________________________________________________________________

The Italian Job, by Marc Chandler

Many investors are closely watching Italy. It is seen as the next flashpoint for the wave of populism after Brexit and Trump's success. The constitutional referendum will be held on December 4. Although the center-right Republican Party in France holds its first primary this weekend, ahead of next spring's presidential election, the Italian referendum poses a greater immediate risk.

Without exception, the 32 polls from 11 companies reported since October 21 all showed the referendum would be rejected. There is widespread mistrust for polls after the UK referendum and US election, but the common element was under-estimating the populist sentiment. In Italy, it is tempting to read the polls as showing the populist ahead.

The problem with that interpretation is that it is not just the populists that are opposed to Renzi's constitutional reforms that, especially in light of earlier political reform, would strengthen the prime minister. Italy has had over 60 governments since the end of WWII. Most recently, Renzi is the third unelected Prime Minister.

The argument is that without political reforms, and the ability to form stronger governments, Italy cannot mount the kind of economic reforms necessary to revive the moribund economy. Yet all the opposition parties, some unions, and even some members of Renzi's own center-left coalition are opposed.

Nevertheless, a defeat of the referendum is understood as strengthening the populist threat because of how Renzi has handled it. At first, he threatened to resign if the referendum failed. Then he seemed to backtrack and recognize the faux pas of linking his government to the referendum results.

Just yesterday, he was again suggesting he would leave: "If I have to stay on in parliament [after the defeat of the referendum] and do what everyone else has done before me, that is, to scrape by and just float there, that does not suit me." The reasons that the defeat of the referendum is seen as a boost for populist forces is that it weakens Renzi and the PD, and therefore strengthens the second biggest party in Italy, the populist 5-Star Movement, who wants to have a referendum on EMU membership.

There are a couple of things working in Renzi's favor despite him. Still, may not be enough to stem the tide. First, there is more than four million expats eligible to vote. They are thought likely to support the referendum. However, only around a third are expected to vote. This could make a difference in a close contest, but the recent polls show a 5-7 point lead by those wanting to reject the referendum.

Second, the wording of the referendum has been subject to much dispute and legal challenges. It is worded in a way that focuses on the favorable element. Some think this could be worth a few percentage points in Renzi's favor depending on the number of undecideds there are at that late date who decide to vote. Note that most recently the undecided have been breaking to the "No" camp.

Third, Italy reported an unexpected 0.3% growth in Q3 after a flat Q2. Consumption and industrial output were the key drivers. However, with unemployment at 11.7% (despite labor reforms in 2015), many Italian's may have not yet experienced the growth, which in any event remains less than 1% year-over-year. Moreover, early Q4 data warns that even the modest growth momentum may not be sustained. Nevertheless, the fact that Italian growth in Q3 outstripped German growth is noteworthy.

Fourth, Renzi has challenged the EC and submitted a mildly expansionary budget for next year. The EC pushed back, wanting more details about the additional expenditures stemming from the earthquakes and migrant/refugee relief. The EC says it still wants more information, but it will give Renzi more time to make his case, and won't make a final decision until early next year.

As we have argued, the European project is predicated on greater integration and the erosion of national sovereignty. If the populist moment is truly here, the European project is at risk. This is a force, as much as the prospect of tighter Fed policy or more US inflation, that is weighing on the euro.

___________________________________________________________________________________________________________

How Unpredictable Will the Crack Heads be About Italy?

Italy has a major referendum on December 4, the results of which could mark the start of an Italian exit… yet U.S. and most global stocks keep going up. They shot higher after a brief Brexit breakdown. They zoomed higher still after an even shorter Trump slump. Shock after shock is having no impact on markets. They just keep heading on up.

What do you think? Would a crack-addict be realistic about his or her chances of surviving a jump off a roof?

Polls are telling us that this referendum for constitutional reform by Prime Minister Renzi is likely to fail. “NO” is likely to win the day.

Of course, the polls haven’t exactly been a shining light of late… so we’ll see. But have you noticed how these events have tended to favor the far right and exit policies rather than the centrist and unifying parties?

Renzi has vowed to resign if “NO” takes the day and that opens the way for the far-right party to take over and move towards removing Italy from the euro and/or Eurozone, à la Brexit and Trump. And it’s the only way Italy can devalue, default, rebalance, and have a chance of coming out of its debt crisis – at the price of high short-term inflation, of course.

Right off the bat, they could default on their Target 2 loans, largely to Germany, of $344 billion. In total, the weaker Eurozone countries owe Germany $676 billion! So if Italy leaves the Eurozone, the impact would be way worse than anything we’ve seen (and will see) with Brexit.

The stock markets might have moved higher after Brexit and Trump… but what they’re missing is this…

They don’t yet appreciate that Brexit marked the beginning of a major anti-globalization movement that was seconded by the Trump victory. More importantly: Italy is the “death knell.”

Greece was bailed out because it was small enough and Germany and the European Central Bank (ECB) didn’t want to create a reaction of more euro exits in response if Greece was forced to exit.

But Italy isn’t small enough. In fact, it’s too big to fail… and to bail out. It’s the third largest country in the euro and the fourth largest in Europe. If it fails, all of Southern Europe will likely follow.

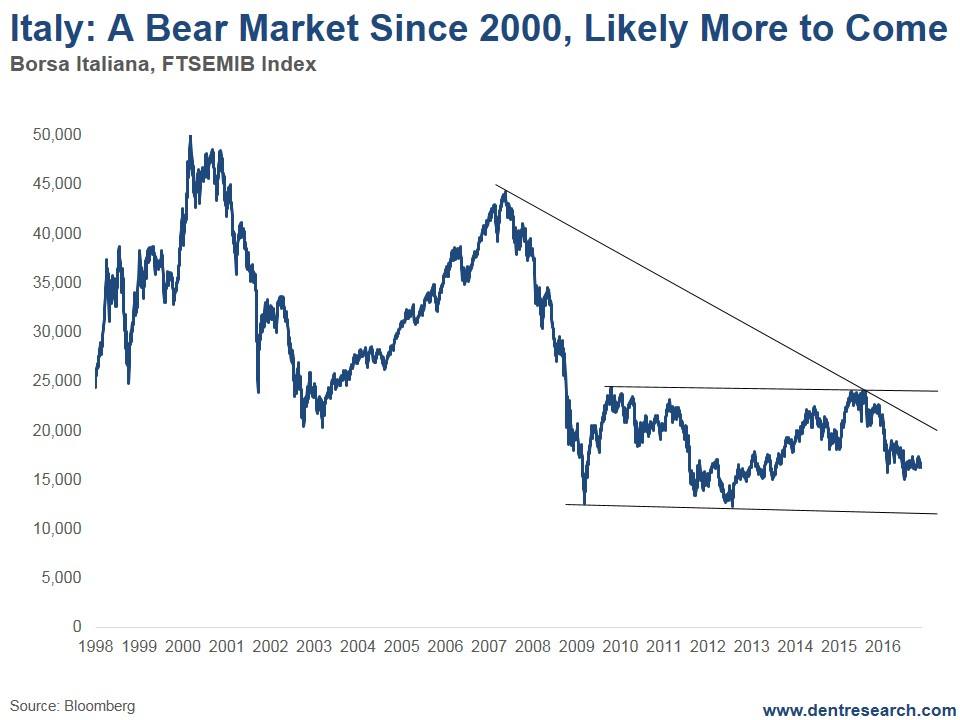

Italy’s stock market is already telescoping a major collapse in Italy, as is recent trends in its Sovereign bonds that have spiked a bit more than all the rest.

Look at Italy’s main stock index.

Italy and Southern Europe stocks peaked back i2000,as did the Stoxx 50. Italy has only seen lower highs and lower lows since then and that is the most bearish of patterns!

Italy’s market is presently down 65% from its all-time highs in 2000, and has been down 73% at its worst in early 2009.

It’s been in a long trading range since late 2009 that would be broken to the downside if it broke below 12,000. Should that happen, the projection would be down to near zero!

Does that sound like a totally bankrupt country or what?

Only a break back above 25,000 would be re-assuring… and I see almost no chance of that happening.

I’ve been warning that Italy is already bankrupt. It’s government debt is beyond 135% of GDP. And its biggest problem is its 18% and rising non-preforming bank loans. Normally, 10% indicates bankruptcy.

So why don’t Italian 10-year Treasuries rise back to the 7.2% yield spike they saw into late 2012? Because Mario Draghi keeps buying them (and others) like crazy. And he continues to threaten to buy more to kill any short traders.

Can you say “rigged market?”

But since August, rates have followed rising 10-year Treasury rates, which have risen 100 bps (basis points). They’ve risen 120 bps from 1.03% to 2.23% in just three months. We’re going to see rates rise to 10-20%-plus in the next year or so as Italy finally defaults!

Italy is the next Greece and there’s no way to bail it out, especially with Germany having a slower-than-expected economy (although it’s not unexpected to me… my demographic models forecast this slowdown long time ago, and it sees Germany facing the greatest decline of any country into at least 2022).

If Italy does exit, it will spell the end of the euro and Eurozone as it is.

The markets reacted irrationally to Brexit and the election of Trump, just as any crack head would. And, just like any crack head, they’re hard to predict in most instances but one: they’re always making the wrong decision.

My dear friend, Andy Pancholi of the Marketing Timing Report, has a major turn date around December 9. It’s likely the markets will turn down into the Italian referendum at first and then they could either accelerate down, or turn up one more time if it surprisingly passes.

This is an important time period to watch and to recalibrate investment strategies. Stocks continue to be harder to predict as they’re the most manipulated by QE policies and the last place for investors to go in a zero or negative rate environment.

We’ve been dead right about a spike in Treasury bond rates, a continued rise in the dollar, a continued fall in gold after a bounce to near $1,400, and a fall again in oil prices after a bounce over $50.

Hopefully this “market on crack” will become more predictable between now and December 4!

Stay tuned.

Author

FXStreet Team

FXStreet

Composed of a group of economic journalists and FX experts, the FXStreet content team produces and oversees all content published on FXStreet. It provides a purely journalistic approach to the Forex market.