GBP: is it being unfairly targeted?

Monday was a bit like Deja-Vu for currency traders, and a keen reminder of how politics can play havoc with a currency. Sterling declined to its lowest level since October as political fears and the Brexit premium started to bite. The pound has managed to claw back some losses on Tuesday, but it remains at risk from a further decline in sentiment.

Why EUR/GBP is at risk

But, is the sell-off in the pound justified? Certainly the uptick in economic data at the end of last year makes it look like the UK economy performed surprisingly well in the second half of the year, even with all of the Brexit uncertainty. Even yield differentials suggest that the sell-off in the pound could be overdone, especially against the euro.

It’s all about yields…

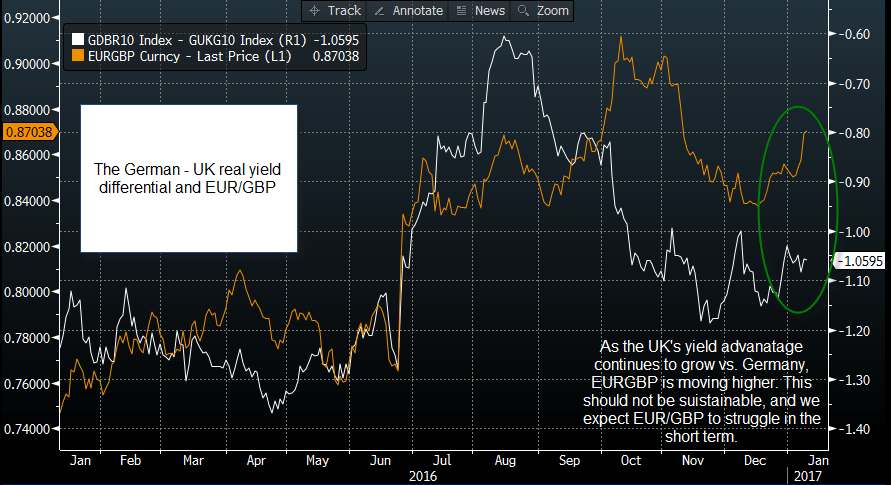

The chart below shows the real yield differential between Germany and the UK (the 10-year sovereign bond yield – the core rate of inflation), and EURGBP. As you can see, as the yield differential has continued to decline as real UK bond yields are 1.06% higher than real German bond yields right now, yet EUR/GBP is still pushing higher. This is counter-intuitive, higher yields tend to feed through to a stronger currency, and vice versa. So, the pound is weakening vs. the euro even though UK yields are higher than European yields, all because of politics.

Don’t mess with politics

It is worth noting that politics has a powerful influence on FX markets, and Brexit uncertainty is likely to remain a key theme as we lead up to the triggering of Article 50 at some stage this quarter. However, politics have hit the pound in fits and starts – immediately after the referendum result last June, in October after the Tory Party conference, and at the start of this year. After these sharp sell-offs periods of relative calm and recovery tend to follow. Due to the pound’s favourable yield advantage over the euro, we think that EUR/GBP could be more at risk from a pound recovery, once the market forgets about the latest May comments and moves onto something else.

Why EUR/GBP is at risk

The technical perspective is also not great for EUR/GBP, which has given back some recent gains on Tuesday. It hit key resistance at 0.87247 – the 38.2% retracement of the EUR/GBP uptrend from June to October at 0.8724, which may limit how far the euro bulls are willing to push the single currency versus the pound. If we get some strong manufacturing data out of the UK on Wednesday then a move back to 0.8553 in EUR/GBP – the 50-day sma – is not impossible.

So, even though we still respect the Brexit premium, we think that politics could take a back seat for the pound over the next few days - or until the next negative headline in the press - which may give sterling time to recover. If this proves to be correct, then yield analysis suggests that EUR/GBP may correct first as it doesn’t have the yield advantage to underpin its recent move higher.

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.