FOMC Preview Minutes of the April 30-May 1 Meeting: Inflation, inflation, where's the Fed's inflation?

- Fed Funds target of 2.25%-2.50% unchanged by unanimous vote

- Economic growth stronger in May statement, with slower household and business investment spending and lower inflation

- Market looking ahead to the economic projections at the June 18-19 meeting

The Federal Reserve will release the edited minutes of the April 30-May1 Federal Open Market Committee (FOMC) meeting on Wednesday May 22 at 2:00 pm EDT, 18:00 GMT

FOMC Rate Policy Analysis

The better than anticipated US first quarter GDP of 3.2% received its due in the May FOMC statement where “economic activity rose at a solid rate” in contrast to the March note where “activity has slowed from its solid rate in the fourth quarter.”

The lexical oddity of referring to both the fourth quarter’s 2.2% growth as “solid” in the March statement and also the 3.2% growth in the first “Information [referring to the first quarter] received since…March indicates that the labor market remains strong and that economic activity rose at a solid rate,” leaves an observer a bit puzzled as to what constitutes solid growth for the Fed governors. For a vast and mature industrial economy like the US there is a world of difference in wealth, income and economic activity between a 2.2% and a 3.2% expansion. Perhaps the minutes will offer clarification.

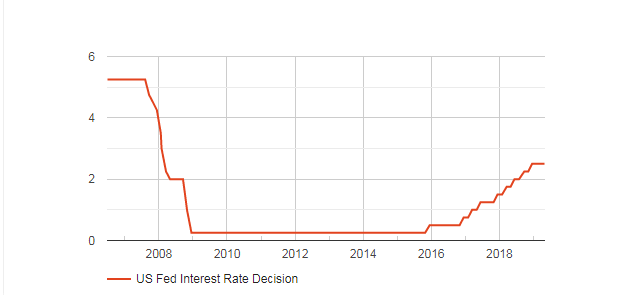

Rate policy has been on hold since the December 0.25% increase to the 2.25%-2.50% target range. The vote to raise in December and since to maintain have all been unanimous. There is little prospect for a change in policy driven by US economic fundamentals in the next several meetings.

FXStreet

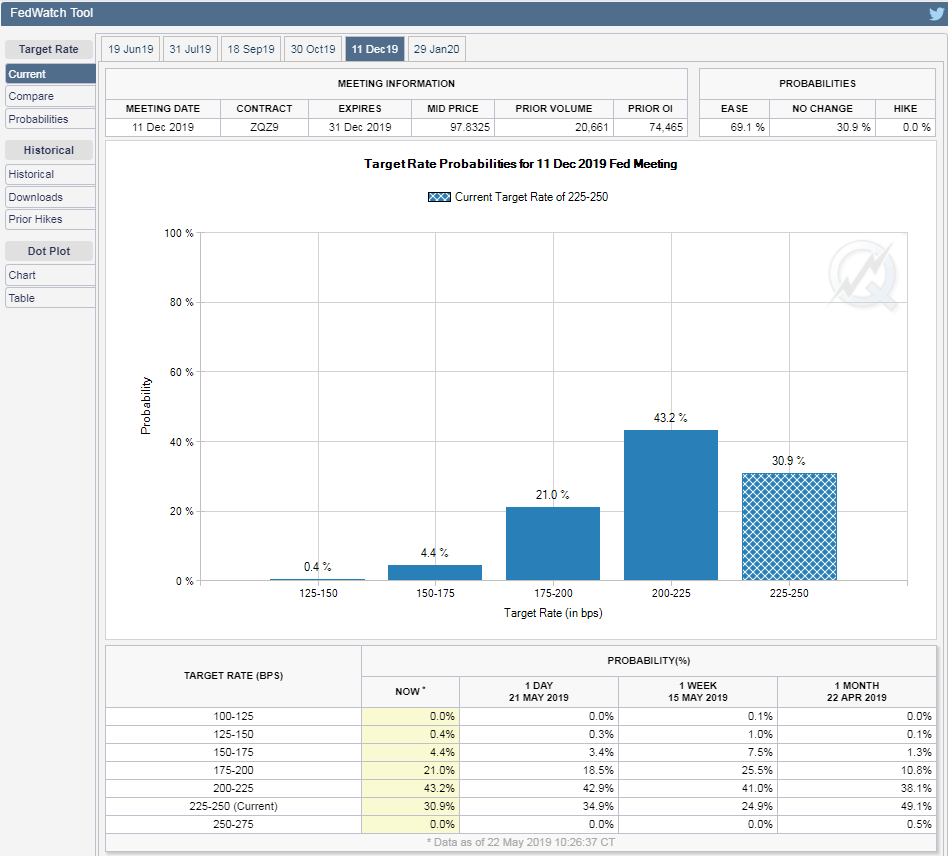

Nonetheless markets are convinced that the trade war with China, a global economic slowdown and perhaps presidential pressure will force the Fed to reduce rates by the end of the year. The Fed Funds futures show the odds of at least a 25 basis point reduction rising steadily at each subsequent FOMC meeting. Next month the chances of a cut are just 6.6%. At the July 31st meeting the odds are 16.7%, at September 18th 39.5%, October 30th 49.8% and last meeting of the year December 11th the chance of a cut rises to 69%.

CME Group

FOMC Economic Analysis

The FOMC statements of the last three meeting, January, March and May have offered little difference in their characterization of US economic growth and inflation. Within the FOMC consensus the market will be searching for hints of the governor’s future concerns.

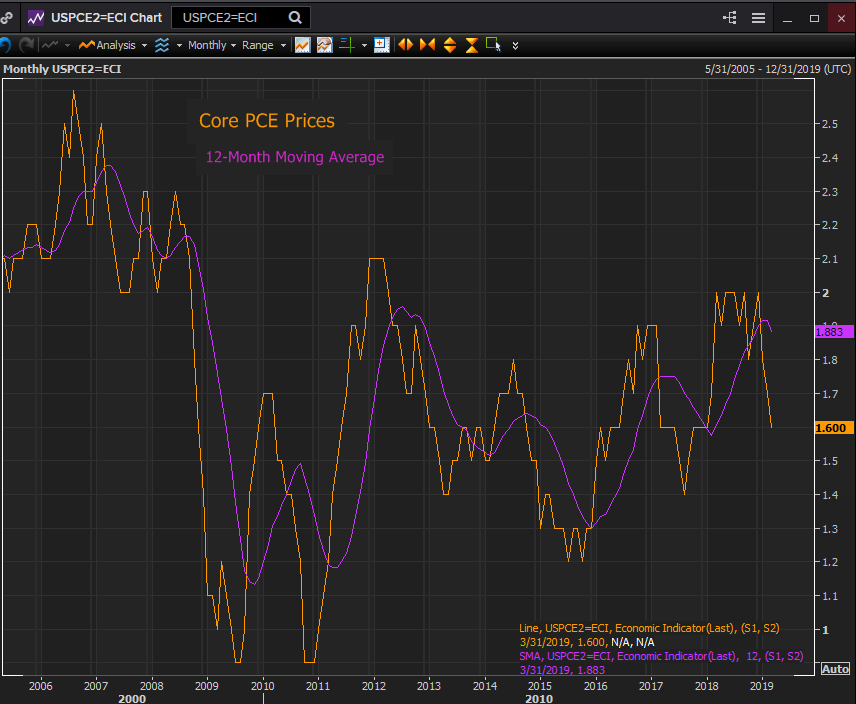

Inflation has received most of the speculative focus since the May meeting with the core personal consumption expenditure price index, core PCE for short, dropping to 1.6% annually in March and expected to be unchanged when the April figures are released on May 30th.

The steep decline this year from 2% in December and a 12-month moving average of 1.9% in the fourth quarter brought Chairman Powell several inflation questions at the May 1st press conference. He refused to be draw out on the Fed’s thinking saying that “Inflation will return to 2% over time and will be symmetric around our target.” That is the standard Fed position. He also said that the weaker inflation in the 1st quarter was transitory and that the current policy stance is appropriate, i.e. there have been no considerations of a rate cut. He did concede that if inflation stayed below the 2 % target that would be a development that the Fed would have to take into its analysis.

Reuters

Over the decade since the financial crisis the central bank has consistently underestimated inflation and over-estimated the effectiveness of its policies in bringing it to the 2% target.

The coverage in the minutes around the inflation discussion will be its most important market focus. How many governors expressed concern? Were rate hikes broached as an eventuality if inflation continues to be weak?

The edited minutes of the FOMC meeting permit a wider view into the deliberations of the FOMC governors. If they are growing wary about inflation this is where it will show. Any speculation or evident concern about low inflation will further boost market conviction that the next Fed move will be a rate cut.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.