Federal Reserve Preview June 18-19 FOMC: Proto-Easing

- Fed Funds 2.25%-2.50% target range predicted to be unchanged

- Market expecting confirmation of easing bias into the second half

- FOMC statement wording, especially "patient" and the economic projections important

The Federal Reserve will finish its two day policy meeting of the Federal Reserve Open Market Committee (FOMC) on Wednesday May 19th. The central bank will issue it rate decision, policy statement and Projection Materials at 2:00 pm EDT, 18:00 GMT followed by Chairman Jerome Powell's statement and news conference at 2:30 pm EDT, 18:30 GMT.

Fed policy

The Fed has gradually moved to a policy stance one might call proto-easing. Beginning with the now famous use of “patient” to describe “future adjustments…for the federal funds rate” in the January 30th FOMC statement, the first after the December 0.25% hike, that description has remained official, identically composed in the March and May FOMC statements.

The change in mood at the Fed has been driven by the macro-economic environment. The US-China trade war, cold at the moment, Brexit in the UK and Europe and the general slowdown in growth, the “global economic and financial developments” of the May statement.

Mr. Powell and other Fed officials have been specific about these threats coming to the US economy from outside the continent.

Federal Reserve Chairman Powell seemed to open the gate for a rate cut as long ago as January when he said, “But what I do know is that we will be prepared to adjust policy quickly and flexibly and to use all of our tools to support the economy should that be appropriate to keep the expansion on track."

American economic growth does not appear to need support but sustaining that momentum is the Fed’s focus.

What is not on the governors’ radar is using the fed funds rate to boost inflation.

In response to a question about low inflation after the May 1st FOMC meeting Chairman Powell said, “We do not see a strong case for moving [rates] in either direction.” “The weak inflation performance in the 1st quarter was not expected...some of it appears to be transitory or idiosyncratic.” Mr. Powell did not offer an opinion on whether inflation could lead to lower rates saying only that the governors were united in considering the current policy appropriate.

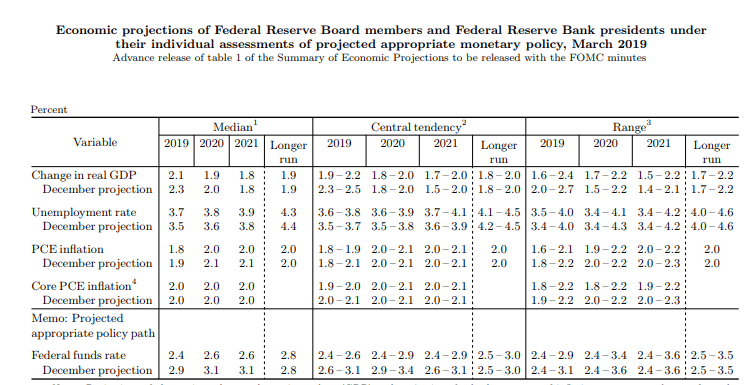

Projection materials

The pause initiated by the January statement took on much more concrete form with the March Projections Materials released with the FOMC statement on the 19th.

The Fed issues its economic projects four times a year, with the FOMC meetings in March, June, September and December.

The March materials posited a 2.4% fed funds rate at the end of 2019, 0.5% lower than the December 2.9% estimate, implying no rate increases or even one rate cut in 2019.

In three months the Fed had gone from two rate hikes to none. If you go back to September 2018 the rate call was 3.1% and three increases after the December move to 2.5%.

The GDP projection for this year fell to 2.1% in March from 2.3% in December. The core PCE rate was unchanged at 2.0%.

Markets will be looking for changes in the materials that indicate a second half rate cut, primarily in the fed funds, GDP and core PCE figures.

US economy

The American economy is showing few signs that the Fed’s external concerns are affecting growth.

Expansion in the first quarter was at a 3.1% annualized rate. The latest estimate of the Atlanta Fed’s GDPNow model for the second quarter on June 18th was 2.0% down 0.1% from June 14th but up from 1.4% on June 7th. The current average of 2.6% is notably higher than the Fed’s 2.1% March GDP projection.

Retail performance was generally better than expected in May with overall sales and the control group gaining 0.5%. But it was the revisions to the April results that colored the report. Headline sales jumped from -0.2% to 0.3%, control climbed from flat to 0.4% and the ex-autos number went to 0.5% from 0.1%.

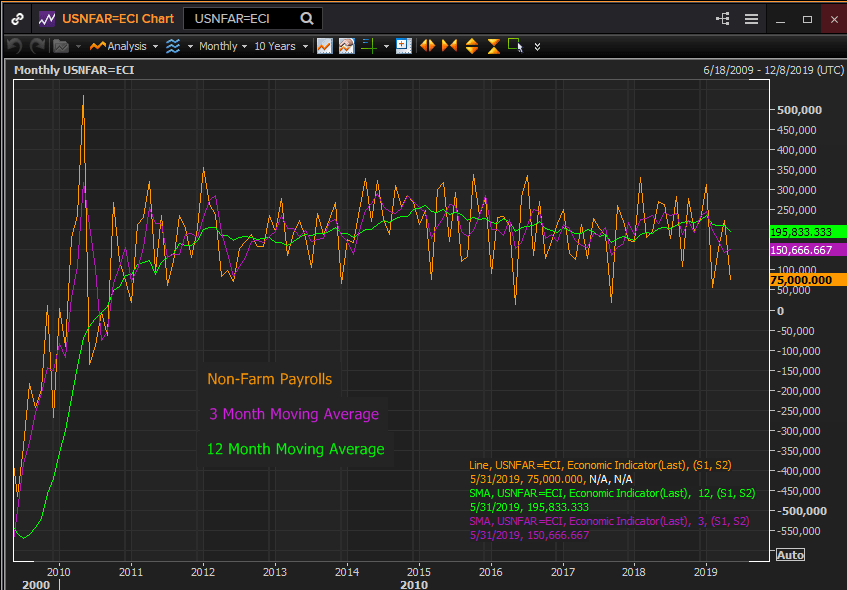

Job creation has declined somewhat. Two of the last four non-farm payrolls were below 100,000, February at 56,000 and May at 75,000. The three month moving average has dropped from 245,000 in January to 151,000 in May.

Reuters

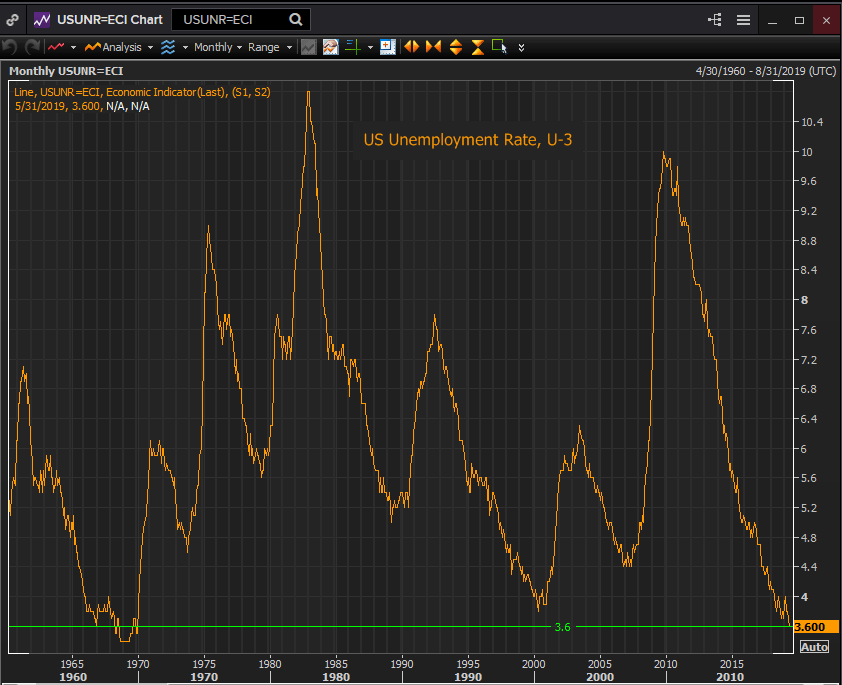

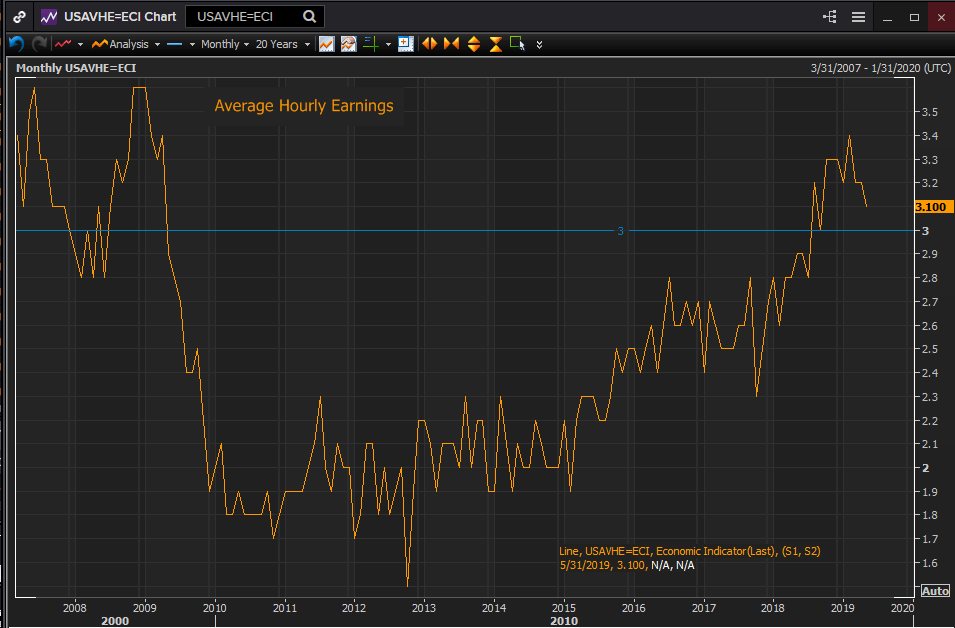

Other labor market indications are excellent. The unemployment rate at 3.6% and the 4-week moving average of initial jobless claims at 217,750 are at or near five decade records. Annual average hourly earnings rose 3.1% in May not far from the post-recession top at 3.4% in February. Wage increases per year have been above 3% for 10 months the best period since the second half of 2008.

Reuters

Reuters

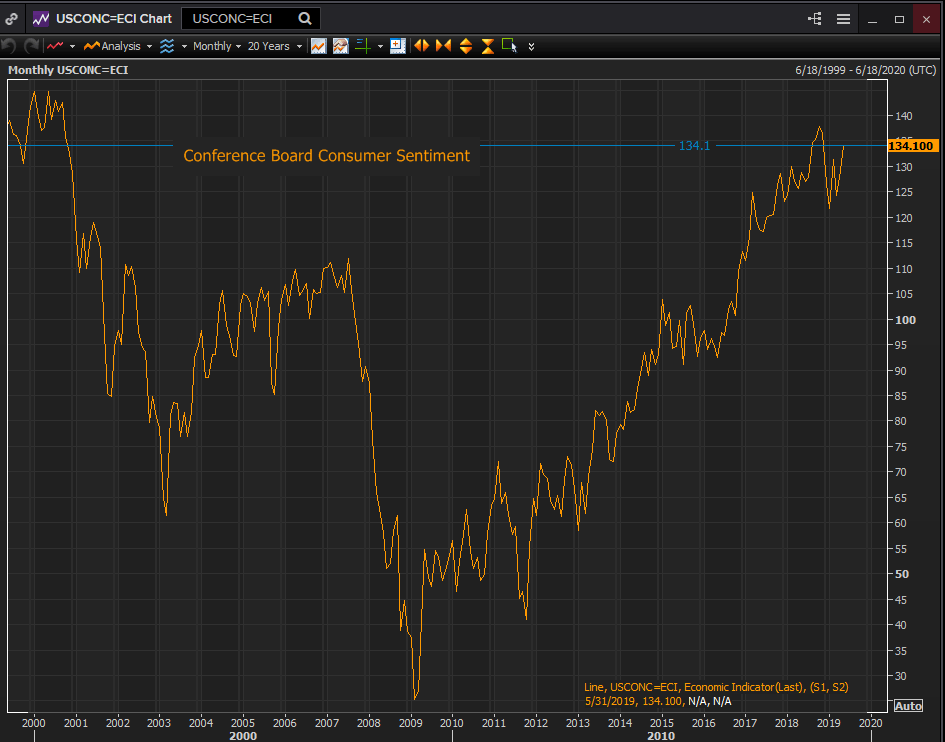

Consumer sentiment remains strong if down somewhat from its extremes of last year. The Conference Board Consumer Sentiment Index registered 131.4 in May, which, except for the August through November scores, is the best reading since November 2000.

Reuters

The core PCE price index was 1.6% on the year in April and is expected to remain there in May.

Treasury rates

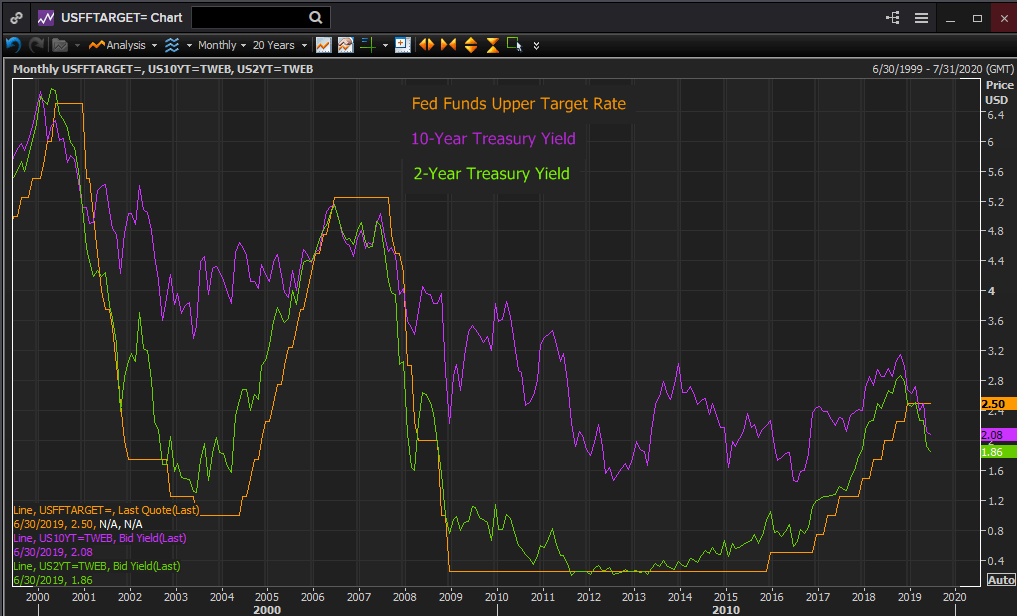

Yields on the 2 and 10-year Treasury bonds are below the 2.5% fed funds rate. The 2-year has been so since mid-March, and the 10-year since early May. This has happened twice in the past twenty years, in mid-2000 and in third quarter of 2006. Each time a Fed rate reduction cycle followed, in six months in 2000 and 13 months in 2006 and 2007.

Reuters

Fed policy

The US economy is performing well. Growth appears to be resilient despite the China trade dispute, the once and future Brexit and global doldrums. The recent volatility in payrolls which has the Fed’s attention is the only labor market indicator flashing pink let alone red. The phenomenal expansion of manufacturing jobs in the past two years has brought employment back to many rust belt communities.

Retail sales have departed the shutdown reporting volatility. They reflect the buoyancy in consumer sentiment and should remain healthy as long as employment is not a concern.

Notwithstanding the positive condition of the American economy the Fed has been deliberate in signaling its angst and, without saying so, preparing the markets for a change in policy.

Fed communication has an inherent risk in that as the governors’ views become clearer the policy is rapidly priced into the market. Treasury rates have been falling for eight months. Markets expect a clearer path to a July rate cut.

The risk of disappointment and an equity tumble and a dollar surge will be considerable if the FOMC does not produce a more definite indication that a rate reduction is coming at the July meeting.

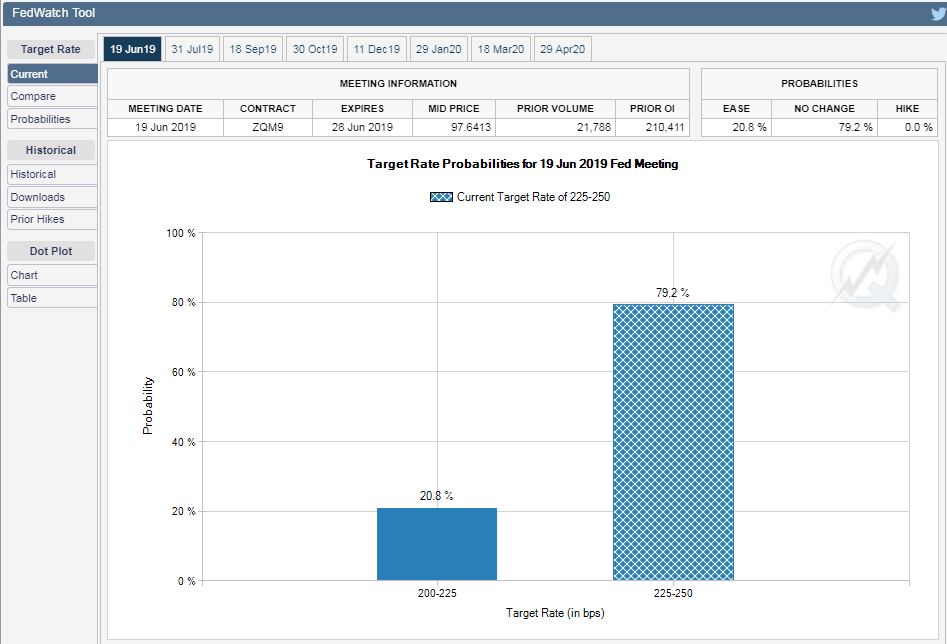

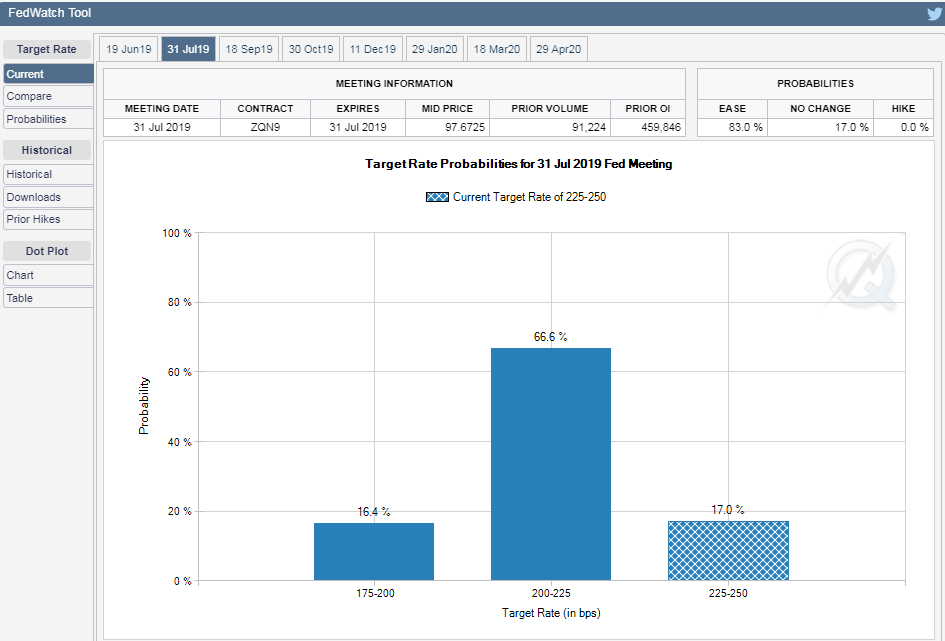

The reversal in the fed funds futures from the June FOMC meeting to July is remarkable. For the Wednesday meeting the odds for an unchanged fed funds rate are 79.2%. Six weeks later at the July 31st meeting the chance reversed, 83% for at least one 25 basis point cut.

CME

It is too early to tell if the Fed has been promulgating a one or two rate cut insurance policy or a full-fledged reduction cycle. The governors themselves probably do not know, there are far too many outstanding variables.

What the governors do know, and it is a tribute to the persistence of the Yellen and Powell administrations, is that the insurance premiums they paid for three years have given the Fed a flexibility and assurance that the ECB and the Bank of Japan can only envy.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.