Federal Reserve October 29-30 FOMC Preview: Three and done

- Expectations for a 25 basis point cut in the Fed Funds rate are over 95% in the futures.

- US economy has not altered appreciably since the September FOMC meeting.

- Market focus will be on the policy prospects for the remainder of this year and next.

The Federal Reserve will end its scheduled two day policy meeting of the Federal Reserve Open Market Committee (FOMC) on Wednesday October 30th. The central bank will issue its decision for the fed funds rate at 2:00 pm EDT, 18:00 GMT. Chairman Jerome Powell will read his statement and hold a news conference beginning at 2:30 pm EDT, 18:30 GMT

Federal Reserve Policy and the US economy

The US economy has changed little since the September 18th FOMC voted to cut the fed funds rate a second time.

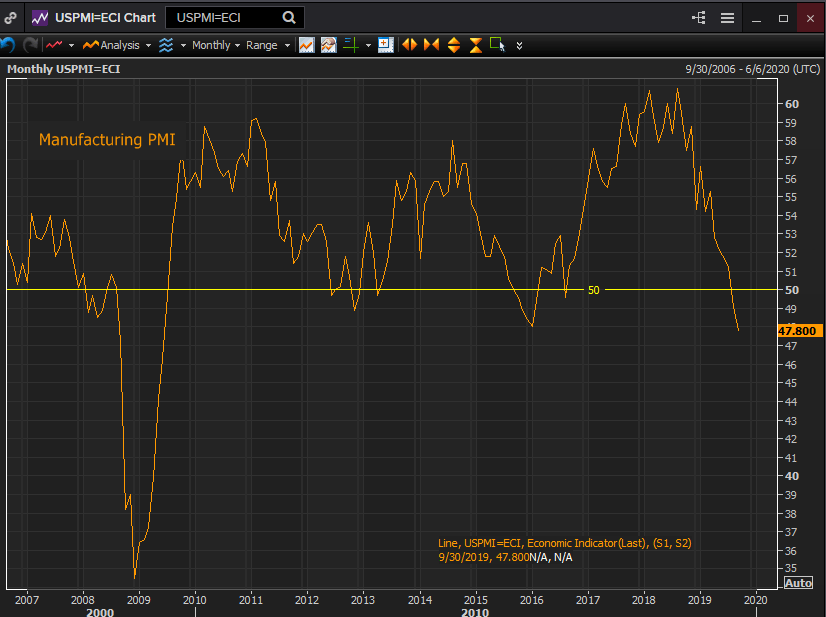

Third quarter growth estimates from the Atlanta Fed’s GDPNow were running at 1.9% the week of the September meeting. The current projection from October 28th is 1.7%. Non-farm payrolls had a three month moving average of 171,000 in August, in September it was 157,000. The purchasing managers’ index in manufacturing had been declining for almost a year, it has since extended its contraction to a second month into September.

Reuters

Business spending indicated by the non-defense capital goods category of durable goods was flat in July and negative in August and September.

Consumer spending was robust at the last Fed meeting. The retail sales GDP component control group had a six month moving average of 0.717% in August, in September that fell to 0.483% and the flat monthly score was the weakest since February. Consumer confidence on the other hand has revived. The Michigan Consumer Sentiment Index fell from 98.4 in July to 92.1 in August and 92 in September. It rebounded to 96 in October.

The two most prominent trending statistics, the decline of payrolls from a 3-month average of 245,000 in January and the yearlong descent in the purchasing managers indexes were already evident in September and have not appreciably worsened.

Reuters

In his rationale for the rate cuts at the last two FOMC meetings, Chairman Powell has stressed the external threats to the long-running US economic expansion, principally the slowdown in global growth, the US China trade war and the British exit from the European Union. The first of which is largely a function of the other two.

Mr. Powell said in September as he did in July that the US economy was in a good place and that the purpose of the Fed’s change in policy was to insure that the expansion and its labor market benefits continued. This estimate of the US economy is unchanged.

Federal Reserve policy and Treasury yields

Treasury yields have executed a sharp turn in the last two months. From the short-lived inversion of the 2-10 Treasury spread in late August, which reached 5 points on August 27th, rates have moved sharply in the opposite direction. The 2-year yield has gained 28 points to 1.64% and the 10-year return has risen 40 points to 1.84%. From the inverted recession signal of August the spread has resumed a relatively narrow but hardly recessionary 20 points.

Federal Reserve economic and rate projections

The September economic and rate projections anticipated GDP this year at 2.2%, which is almost exactly where it is tracking in the current Atlanta Fed estimate, and 2.0% next year. The fed funds rate is envisioned at 1.9% at year end and then no change through the end of 2020.

Conclusion

The economic and political factors that led the Federal Reserve to begin its support action for the US economy have improved sufficiently to justify a pause in rate increases. The Fed will pay only one more premium on its US economic insurance policy.

After almost two years of escalation in the US China trade dispute the two sides announced a preliminary agreement on October 13, just two days before a new set of US tariffs were to go into effect.

The formal deal will not be signed until November as the details are worked into an official agreement. Though the positive effect on business sentiment and investment will take time to develop, the promises from both sides to continue working to resolve the remaining issues will go a long way to defusing this paramount threat to the global economy.

The fear of a global trade war that has curtailed business investment on both sides of the Pacific Basin will diminish and spending should gradually recover to levels normal for the rate of economic growth in the US and China.

If the American and Chinese economies resume a stronger trajectory, the rest of the global will follow.

In the UK Parliament has approved a general election for December 12th. Prime Minister Boris Johnson’s Brexit deal and the British exit from the European Union will be the chief if not sole topic for the electorate.

If Johnson’s Conservatives win a majority his Brexit deal will be approved by Commons and the project that has bedeviled British politics for more than three years will fade into the details of execution. If Labor and the Liberal Democrats win, a second referendum is their stated goal.

Though the Tories have a strong lead in the polls, elections are chancy things as Theresa May discovered to her chagrin. But Boris Johnson is not Ms May and his chance of bringing the voters to back his Brexit arrangement and end the paralysis that has settled over British politics is probably better than the polls estimate.

Treasury rates also indicate a change in policy is on the way much as they did in November 2018 just before the Fed’s final increase that December. The rapid return to a normal 2-10 Treasury spread is a strong suggestion that the brief inversion in August may be one of those rare credit market occurrences that do not in the end predict a recession.

Chairman Powell and the FOMC will not surprise the markets by denying the rate transparency they have championed. But material changes in the US China trade dispute and the British exit from the EU and the market perception of diminished risks will halt rate cuts for the remainder of the year and probably beyond.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.