Federal Reserve Interest Rate Decision December 10-11 Preview: Watching for the Projection Materials

- No expectation for a change in the Fed funds target rate.

- US economy has strengthened since the October FOMC.

- Market interest will be on the Fed’s rate and GDP estimates for 2020 and 2021.

The Federal Reserve will finish its scheduled two-day meeting of the Federal Reserve Open Market Committee (FOMC) on Wednesday, December 11th. The governors will release the policy decision and economic and rate Projection Materials at 19:00 GMT. 14:00 EST. Chairman Powell will read his statement and hold a news conference starting at 19:30 GMT, 14:30 EST.

Federal Reserve policy and the US economy

The US economy has gathered strength since the last Fed meeting on October 29-30.

Third-quarter GDP rose from 1.9% to 2.1% at its first revision, unchanged had been the consensus forecast. The Atlanta Fed GDPNow estimate which reached a nadir of 0.3% on November 15th has rebounded to 2.0% as of December 6th.

The US labor market continues to produce jobs at near-record numbers, unemployment has again reached a 50-year low and wage gains are giving consumers higher disposable incomes.

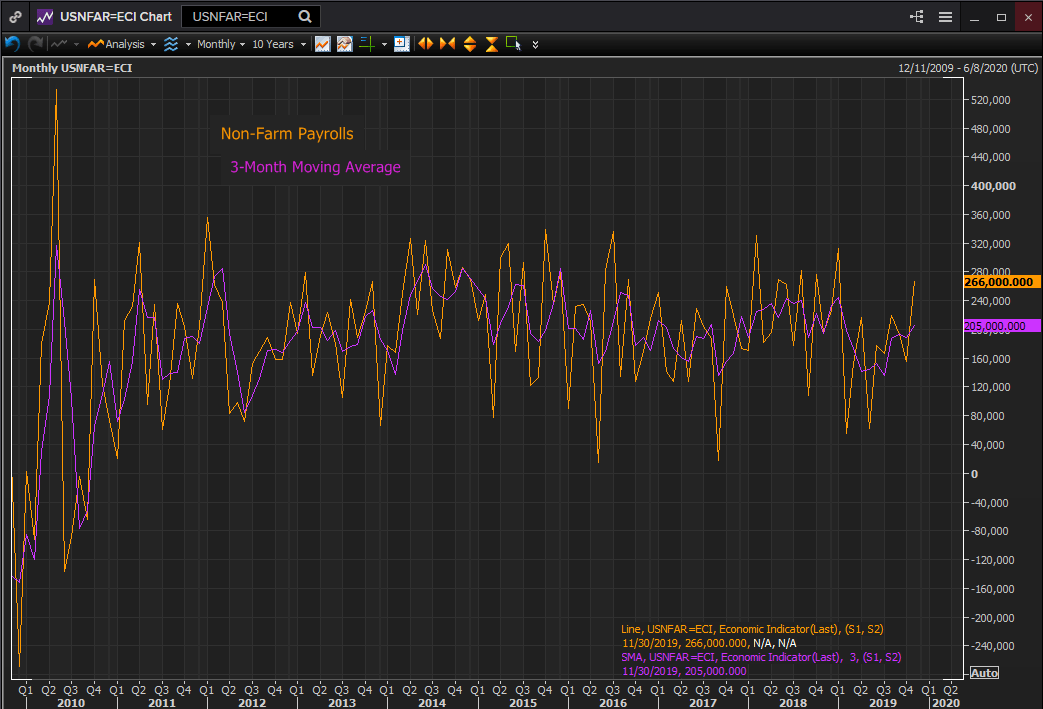

The three months moving average for payrolls jumped to 205,000 in November courtesy of its 266,000 new jobs. The decline in the three-month average from 245,000 in January to 135,000 in July has been convincingly reversed.

Reuters

The unemployment rate dropped to 3.5% for the second time in November, as in August it is the lowest level since 1969. Jobless rates for African-American and Hispanics were again at record lows. Annual average hourly earnings rose 3.1% in November and 3.2% in October making 16 straight months at 3.0% or better.

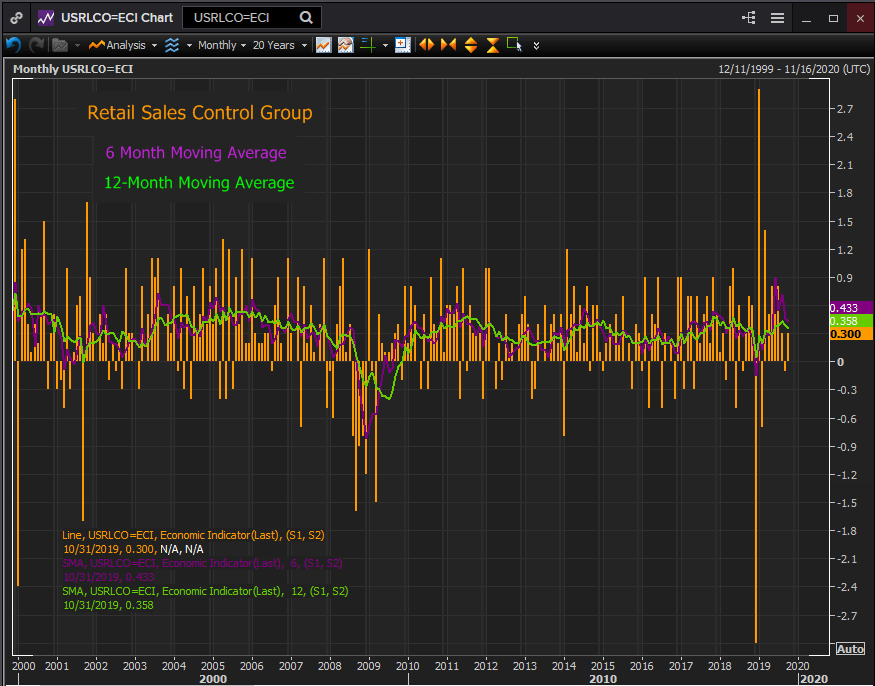

Retails sales in the control group rebounded to 0.3% in October after September's 0.1 loss, the first in seven months. They are expected to be 0.3% higher in November when its figures released on Friday, December 13th. The six-month average in this GDP consumption component is a healthy 0.43% and the 12-month average is 0.36%.

Reuters

Consumer sentiment remains strong. The Michigan Consumer Sentiment Index registered 99.2 in December it highest reading since May and a return to the elevated territory of the last two years after the August three year low at 89.8.

Business sentiment and spending are the main impediments to the economy, hostage to the yet uncompleted US-China trade deal.

The purchasing managers’ index for manufacturing was in contraction for the fourth month in November at 48.1, dropping from October’s 48.3. Indexes for employment and new orders also fell last month. Sentiment in the much larger service sector has recovered to 53.9 in November from September’s three-year low at 52.6 3 but commercials' attitudes are far from the 61.6 high last September.

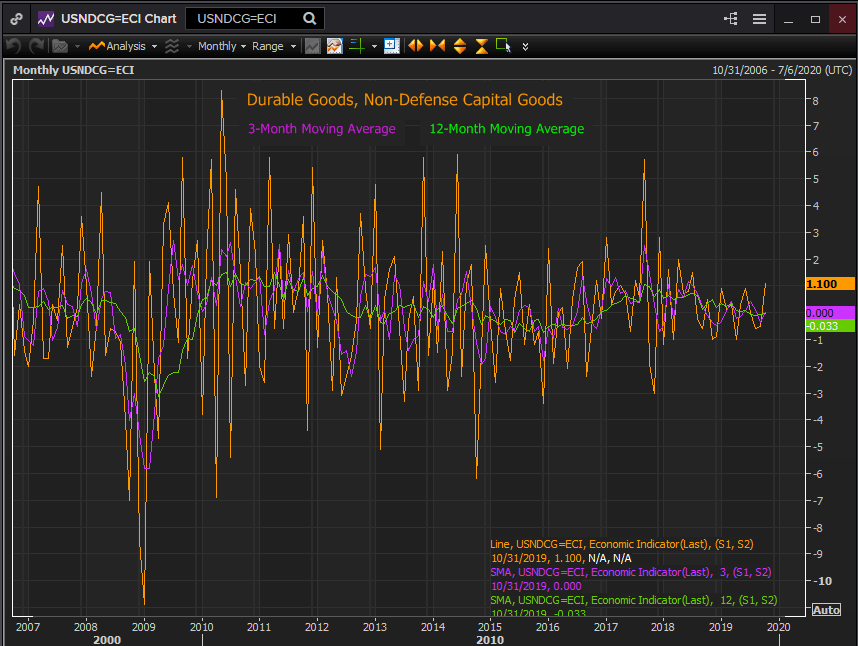

One positive sign for business may be the durable goods category of non-defense capital goods ex-aircraft, often cited as a proxy for investment. Spending here rose 1.1% in November after two negative months.

Reuters

Federal Reserve policy

The rationale for the Fed’s three rate cuts since July has been to protect the US economy from external threats primarily the slowdown in global economic growth and the impact of the long-running US-China trade war and the British exit from the EU.

The US economy appears to have weathered the mid-summer recession scare prompted by the brief inversion of the yield curve in late August and to have resumed a stronger pace of growth. Economic statistics over the past six weeks have fulfilled the Fed’s determination that the economy did not require more insurance. Mr. Powell’s optimistic assessment in October has been born out by the results.

Treasury yields

Treasury yields have moved slightly higher over the past six weeks, an indication that economic conditions have improved. The 2-year Treasury yield was 1.60 on October 30th, on December 10th it was 1.65%. The 10-year was 1.77% on October 30th, it is now 1.83%.

Federal Reserve Projection Materials

Although the Fed insists that its economic and rate estimates issued four times a year are not forecasts, that is exactly how the market sees them.

In September the median projection for the fed funds rate at the end of this year and next year was 1.9%. That was a substantial reduction from the June estimates of 2.4% for 2019 and 2.1% for 2020.

The GDP projections were 2.2% for this year and 2.0% in 2020. The US economy has grown at a 2.4% annualized rate through the first three quarters. If the Atlanta Fed fourth-quarter estimate of 2.0% is accurate the year would have a 2.3% average.

The June projections were calculated and issued before the Fed began its rate reductions at the end of July. Even the September projections 1.9% issued when the upper target was 2.0% implied the final cut in October.

Conclusion and the dollar

The Federal Reserve judgment at the last FOMC meeting that the US economy was heading for improvement and that global risks had diminished has proven to be accurate. Whether Mr. Powell’s assessment that the US-China trade dispute has moved closer to a conclusion is still undecided but it drags on the economy may be lessening. The Fed funds rate will be unchanged and the neutral stance will be affirmed for the near future.

A US-China trade agreement would provide the US and Chinese economies with a substantial boost. The change in business outlook from tariffs and declining growth to investment, from antagonism to cooperation will occur regardless of the details of the pact. The result will likely be a burst of GDP on both sides of the Pacific.

The apparent end of the three-year-old Brexit indecision will also add to global economic potential.

For the markets and the US dollar the key to this FOMC lies in the Projection Materials. Will the governors mark down their fed funds estimate for next year to take account of the current 1.75% rate or will they see a brighter future and raise their GDP and rate projections for 2020? This rather straightforward economic analysis will either propel or retard the dollar for the next several weeks.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.