Event Risk and Trump’s Weak Dollar Policy

Saxo Bank CIO and chief economist Steen Jakobsen sees event risks on the near horizon in terms of Trump policies and the US dollar.

Specifically, Jakobsen has a focus on a “Weak Dollar Policy” that he expects Trump to pursue.

Ready, Steady, Go by Steen Jakobsen

We stand in front of major event risks in the Dollar direction with three announcements:

-

February 28th: Trump to address a joint session of Congress

-

March 14-15th: FOMC meeting

-

March 17-18th: G-20 finance ministers & central banks meet in Baden, Germany

As background G-20 consider the G-20 Hamburg Summit Priority Agenda

The fact Trump is struggling to keep the “business” momentum going and is falling back to being Trump “the candidate” shows the limited range and output from the Trump administration.

By this time in February, all prior Presidents had their agenda and economic policy announced. Trump don’t seem to have a direction and strategy except for the “Tweeter-attack mode”

This means he is likely to refocus his effort leading into his address to a joint session of Congress. There will high expectations for a tax plan, repealing Affordable Care Act, Obamacare, and his trade policy which could include some comments on “the unfair FX policy by China & Germany alike”.

America first is the call to action used by not only Trump but also the majority leader Ryan when rallying behind Trump’s policies. It means “protecting” US jobs at any cost, at least case by case. But what is the overall strategy on trade and globalization?

A pressured Trump is a dangerous Trump. We are more likely to see “fall out” under the present condition than under a more smooth administration.

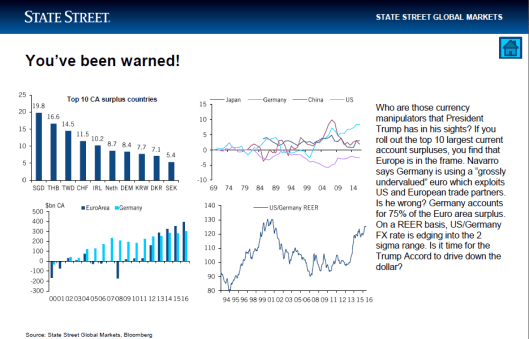

The focus remains on trade as Trump sees trade deficit as the main culprit in his narrative of the “US losing jobs”, despite having below average unemployment.

State Street has some excellent charts on this issue:

Germany vs. US REER [Real Effective Exchange Rate] basis being 2 sigmas cheaper will be an issue for Trump and staff to look at.

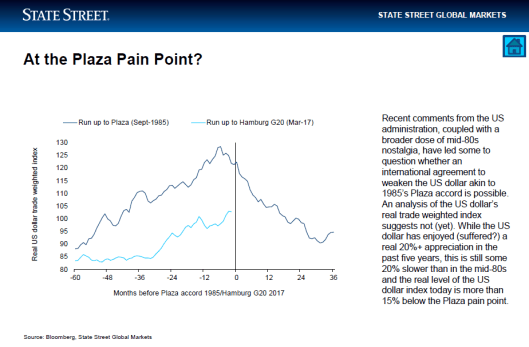

Tump Accord?

Not so fast says State Street.

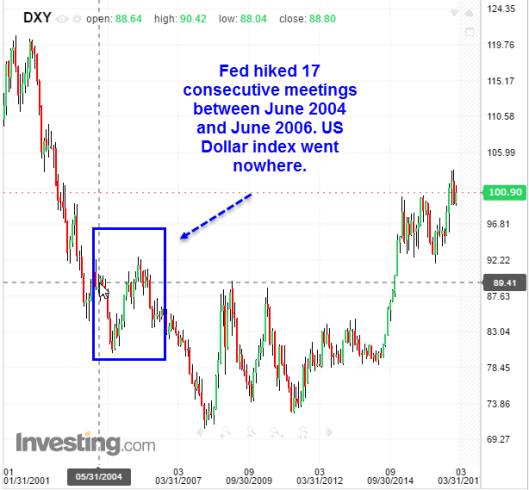

Weak Dollar Policy

We think Trump will pursue a policy of weaker US dollar.

Whether this will turn into direct policy, i.e.: announcing the end of US reserve status similar to Trump’s political hero Nixon taking the US off the gold standard in 1971, could be more clear by end of March.

In probability terms this is how we see this playing out:

-

20% – Stronger dollar through no change to policy and a Border Adjustment Tax estimated to make dollar 15-25% stronger.

-

60% – Indirect weaker dollar – Constant focus on other currencies being too weak, the Fed tightening (which historically means weaker dollar) & slowing US economic growth.

-

20% – Direct- announcing US dollar is no longer the reserve currency and forcing either New Plaza Accord or similar action by overseas exporters (1980s repeat).

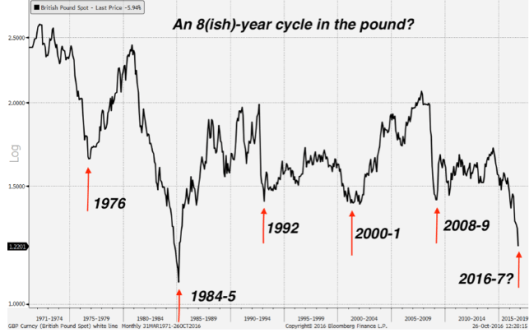

We see US dollar index testing the 96.00 level on unchanged policy. If confirmed that weaker dollar is the new policy of choice, the dollar cycle could be turning down in a traditional 8-year cycle.

British Pound 8-Year Cycle

This is our weekly “model” trade indicator.

Bearish on the Dollar

Next one month should give us major input to next direction in the US dollar, we remain bearish because:

-

Inflation is topping: Overall the peaking base effect in energy will reduce inflationary upside. The YoY net change in oil prices will come down from +85% now in January data to 5% in May.

-

The FOMC & economy will remain slow: Yellen repeat strong rhetoric talk based on dual mandate but overall the economy continues to sputter on productivity and hence growth.

-

The weighted risk of weaker Dollar policy is 20% to 80% depending on the definition. A stronger dollar will kill growth and inflation not only in the US but globally.

Safe travels,

Steen Jakobsen

End Steen Begin Mish

Some of my readers will not get to this point because of a perceived attack on Trump. That’s too bad because Steen presents many interesting ideas, some I agree with and some I don’t.

Politics

In regards to politics, I have lost readers recently because I recently supported Trump and because I didn’t.

I am issues based. I disagree with Trump on trade issues and on his handling of the travel ban. I generally agree with Trump on Russia.

Those looking for constant Trump bashing can easily find that elsewhere, as can those who seek constant praise for Trump.

Amusingly, One person said goodbye today, after accusing me of wavering.

Inflation

I discussed a spike in the PPI and CPI twice this week. Links are below. Oil was the culprit. If oil stabilizes here, it unlikely the CPI will continue the current spike. The CPI might even decline if oil prices fall back.

That said, the medical portion of the CPI is a total joke (way understated), as is housing portion. The latter is due to the BLS’ use of Owners’ Equivalent Rent (OER) instead of actual housing prices.

But the Fed lives and breathes this stuff, and it is their view, not mine, that matters.

FOMC

The market now expects at least one hike by June, and at least one more hike by December. Color me skeptical. The economic reports have not been that good. It’s been a profitable trade betting against spikes in rate hike odds.

Dollar

I am bearish on the dollar as well. If the Fed does not hike as much as expected, the dollar is likely to weaken.

The dollar may weaken even if the Fed hikes.

End of US Dollar as Reserve Currency

I fail to see how halting the US dollar as reserve currency can be accomplished by decree. How? This is not the reverse of Nixon closing the gold window by decree.

Would a plaza accord work? I have strong doubts. In the first place, do countries want stronger currencies?

Japan surely doesn’t. Germany might, but do Spain and France?

That said, an announcement by Trump, even if it could not be enforced, could weaken the dollar significantly, even if it did nothing in regards to reserve currency status.

Gold

Steen did not discuss gold, but it is an important part of this cog.

If the dollar weakens, gold rates to rise (all else being equal). Might gold rise anyway?

Yes, there is a very strong chance the eurozone breaks apart. A currency crisis is on deck. The Euro, the Yen, and the Yuan all have serious issues.

If the dollar rises because of Eurozone problems, I would expect gold to do well.

Related Articles

-

CPI Jumps Most Since February 2013 on Energy: Did Gasoline Prices Really Rise 7.8% in January?

-

PPI Spikes 0.6% in January, Largest Jump in 20 Months: Start of Inflation Run? Will February Repeat?

-

Farage Expects Another “Big Shock”, Warns EP on “More Europe”: Elites vs. Underdogs French Style

-

Vice-Chairman of EuroThinkTank States “Euro May Already Be Lost”

-

Diving Into the Medical CPI: Are Your Medical Expenses Up Only 5% from Year Ago?

Addendum

The source of the 8-year British Pound cycle chart is You’ve heard of Kondratiev waves – now meet the Frisby flux, the pound’s eight-year cycle by Dominic Frisby.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc