EUR/USD Forecast: The 1.10 area is seen holding the downside

- EUR/USD stays in the area of YTD lows just above 1.10.

- Developments from the Chinese coronavirus dictate the mood in markets.

- Markets’ focus now shifted to US data and upcoming FOMC meeting.

EUR/USD remains under pressure amidst the current environment of risk-off sentiment, where the safe havens remain broadly supported on the back of the developments from the Wuhan coronavirus and its potential implications on global growth, most particularly in China.

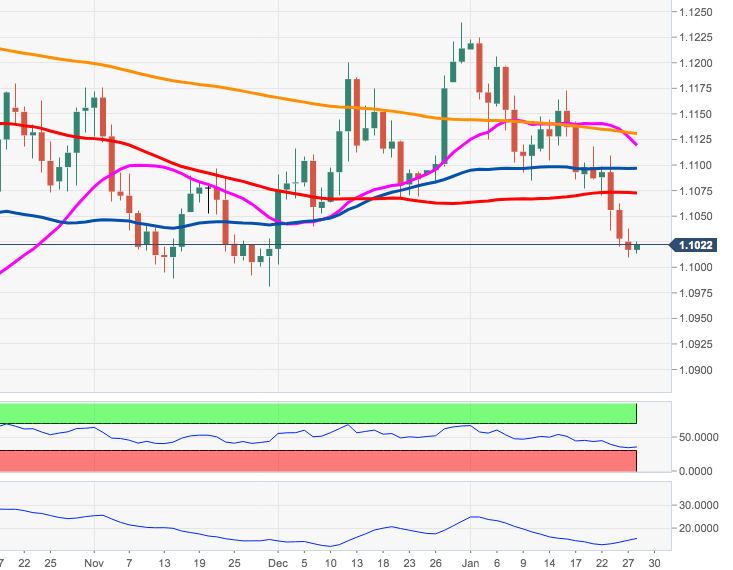

The pair has intensified the downside after breaking below key support levels, namely the 55-day and 100-day SMAs in past sessions, exposing the move to a deeper retracement. In addition, further weakness in the single currency came after the ECB delivered a somewhat dovish message at its meeting last Thursday.

Later in the day, US key data should keep the attention on the buck, while market participants warm up for the FOMC meeting due on Wednesday, as well as German/EMU advanced inflation figures, expected on Thursday and Friday, respectively.

Short-term technical outlook

The ongoing leg lower in EUR/USD appears to have met some contention in the 1.10 neighbourhood for the time being. However, if the selling impetus regains steam, then the 1.0980 region – where is located November’s low – should return to the traders’ radar. In the broader picture, as long as the 55-day SMA - today at 1.1089 - caps the upside, the bearish stance on the spot is seen unchanged. Although not favoured in the short-term view, if bulls regain the upper hand, interim resistance is seen at the 100-day SMA at 1.1068. This area of resistance is reinforced by the proximity of the 3-month resistance line. Something to keep in mind: the RSI is close to the oversold territory, while the ADX at around 15, shows the current downtrend lacks (proper?) strength.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.