EUR/USD Forecast: not all is lost for EUR bulls

- US data and trade war headlines conspired against the common currency at the end of the week.

- EUR/USD could extend gains next week, but sentiment keeps favoring the greenback longer-term.

The EUR/USD pair surged to a fresh September high, 1.1721, retreating from the level but anyway closing the week with solid gains. A bout of risk appetite sent the greenback lower, on hopes the EU and the US could resume trade talks before the US launches the next round of tariffs, boosting equities to fresh multi-month highs. Additionally, US inflation eased in August, with core annual inflation easing to 2.2% after reaching a 10-year high of 2.4% in July, cooling down modestly chances of four rate hikes this year, although with chances of a September hike unchanged at 95%. Monthly core inflation increased by 0.2% matching the previous reading and missing market's expectations of 0.3%. Despite coming below expected, US inflation remained above the Fed's target. Easing inflation, coupling with wages' growth in the same month as indicated by the Nonfarm Payroll report, is good news for American companies. Furthermore, it indicates that higher wages are not generating inflation, and therefore the Fed's future actions will be foreseeable.

The ECB had a monetary policy meeting, and for a change, President Draghi failed to weaken the EUR. The Central Bank left rates unchanged as expected, and added nothing new to what the market already knew. A modest downgrade in growth forecasts was no game changer, while inflation forecasts remained unchanged.

Trade war headlines and their correlated mood had their fair share of influence on the pair these days, but US President Trump has put the issue in pause, still focused in finding the mole within the White House, and the hurricane Florence that is hitting the country. Nevertheless, he made some time to said that the US doesn't need a deal with China, but China does need one with the US. A new round of tariffs has been put on hold ahead of possible talks.

Friday US Retail Sales hurt further market's mood, not because the readings were a miss, as the previous month was revised strongly up, but because they came alongside with a report showing that US import prices fell 0.6% in August, the largest decline in over two years amid global trade tensions, spurring concerns about inflation easing further.

The greenback got additional support by the end of the week, from an upbeat Consumer Confidence estimate, as the Michigan preliminary index for September jumped to 100.8, well above the 96.6 expected and the 96.2 in August.

The EU will release August inflation next week, and preliminary Markit Services and Composite PMI for the region, being the most relevant scheduled events.

EUR/USD Technical Outlook

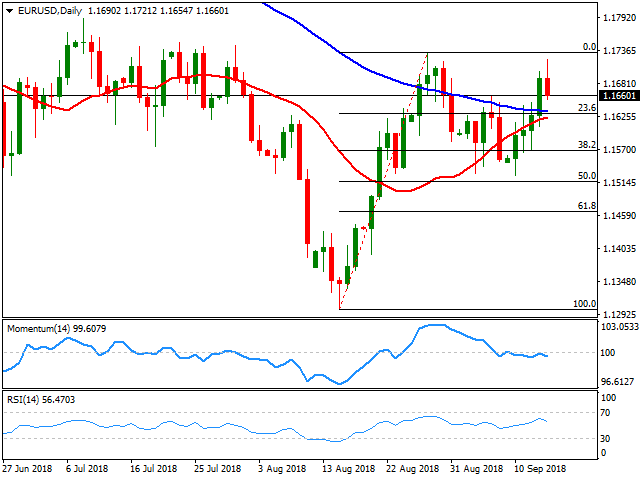

The EUR/USD pair neared August high before retreating but its set to finish the week above 1.1630, the 23.6% retracement of its August rally. The weekly chart shows that the pair is finishing below a strongly bearish 20 DMA, although above the larger ones. Technical indicators remain within negative levels, the Momentum flat for a third consecutive week as the price was unable to surpass the mentioned high, while the RSI has advanced just modestly, but lacks the strength to confirm additional gains ahead, currently at 46. A sustainable advance past 1.1700, is what it takes to discourage bears.

In the daily chart, the 20 and 100 DMA hover around the mentioned Fibonacci support, lifting the relevance of the support. The Momentum indicator, which failed to retake positive ground offers a modest downward slope, while the RSI also turned lower at around 56, leaning the scale toward the downside, which will be confirmed on a break below 1.1630. The next relevant support from there is then 1.1550, while below this last, the decline could continue down to 1.1490. To the upside, the 1.1730/40 area is key, as, above it, there's room for an extension up to 1.1860.

EUR/USD sentiment poll

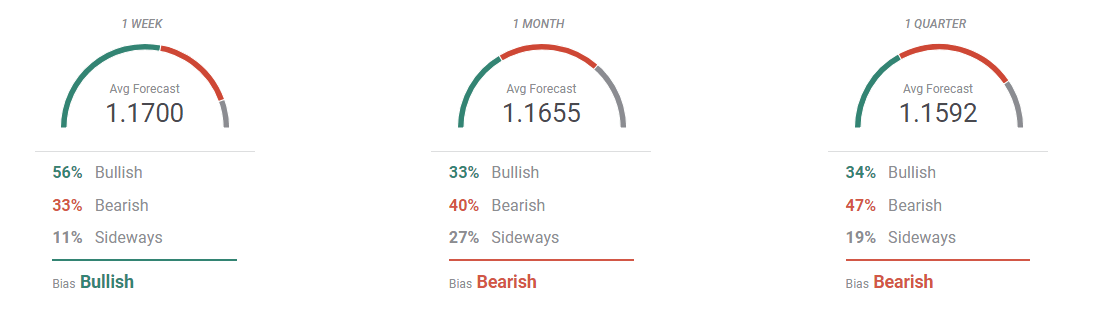

The FXStreet Forecast Poll shows that the bullish sentiment will likely prevail next week, with 56% of the polled experts going long, up from 50% the previous one, although with the average target lifted from 1.1612 to 1.1700. In the monthly and quarterly views, bears are the most, with the average target rising in the first, and decreasing in the second time frame to 1.1592.

The FXStreet Overview chart shows that moving average in the 1-week view heads sharply up and its highest in over a month, but that momentum fades in time, with the larger time frame moving average turning bearish, as, in this last, the largest accumulation of possible targets is around 1.1300.

Related Forecasts

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.