![]() Mike “Mish” Shedlock's

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc

Last week we investigated nonperforming EU loans and an EU proposal to freeze accounts if a run on a bank starts.

Today let’s investigate the EU’s deposit insurance scheme with the likely result being a ban on cash.

On July 19, with little media publicity, the EU Single Resolution Board issued a statement with this exact title: Press Release – Banking Union – Single Resolution Board collects €6.6 billion in annual contributions to the Single Resolution Fund, now reaching €17 billion in total.

For starters, there is no “banking union” to speak of. That aside, let’s explore the deposit insurance goal and where things are now.

As of 30 June 2017, the Single Resolution Board (SRB) had collected €6.6 billion from 3,512 institutions in annual contributions to the Single Resolution Fund (SRF). In total, the SRF now holds an amount of €17.4 billion.

The SRF pools contributions which are raised on an annual basis at national level from credit institutions and certain investment firms within the 19 participating Member States. These contributions are calculated on the basis of the methodology set out in the Commission Delegated Regulation (EU) 2015/63 and Council Implementing Regulation (EU) 2015/81 and are collected via the National Resolution Authorities (NRAs).

The SRF is being built-up over a period of eight years (2016-2023). The target size is intended to be at least 1% of covered deposits by end 2023. 3,512 institutions banks and investment firms have to contribute to the Fund.

“The Single Resolution Fund ensures uniform practice in the financing of resolutions within the Single Resolution Mechanism. It is an important safeguard that can be accessed as last resort only. In addition we have Loan Facility Agreements with all Member States in place and are supporting the efforts of Member States to put in place an effective common backstop.” – Elke König, Chair of the Single Resolution Board

The Goal

That’s the entire press release, as written. The goal is to create an emergency “safeguard” that can only be used as a “last resort”.

The target goal is “at least 1% of assets” and it will take until 2023 to collect this reserve.

SRF vs NPLs

At hand right now the SRF has €17.4 billion in the emergency safeguard.

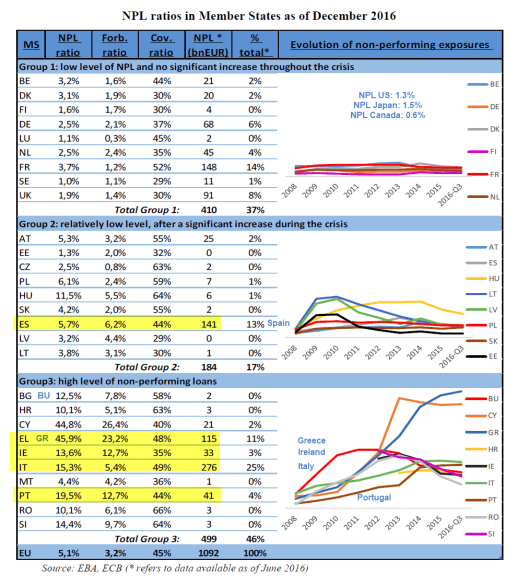

As noted last week, there are Over €1 Trillion Nonperforming EU Loans.

Italy alone has €276 billion in non-performing loans. Greece and Cyprus have NPL ratios of 46% and 45% respectively. Bulgaria, Croatia, Hungary, Ireland, Italy, Portugal, Slovenia, and Romania all have NPL ratios between 10% and 20%.

Spotlight Greece

46% of loans Greek bank loans are non-performing. The Greek sum is a very significant €115 billion.

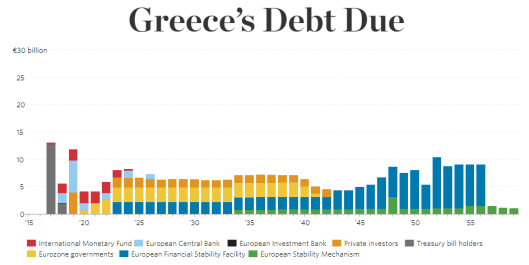

On December 21, 2016, John Mauldin noted Greece’s Debt Problem Has Reached a Dangerous Point.

Here is the key sentence: “Nearly seven years, 13 austerity packages, and three bailouts (worth a running total of $366 billion) later, the Greek economy is still struggling.”

Bailouts? Who? Where?

Not Greek citizens. Not Greet banks.

Rather, $366 billion was used to bailout Greek creditors, primarily Germany.

It will take until 2060 to pay back that “bailout” according to the Wall Street Journal’s report of Greece’s Debt Due, published February 19, 2015 and updated July 28, 2017.

Payback Timeframe

To pay back the alleged bailout, Greece is supposed to maintain a primary account surplus of 3% of GDP indefinitely. A primary account surplus means Greece will collect more in taxes than it spends, not counting interest on its debt.

The odds that will happen are roughly zero percent.

Even if the Single Resolution Fund threw its entire emergency fund of €17.4 billion at Greece, it would not do a damn thing for either Greek debt or Greek non-performing loans.

SRF is a Joke

Simply put, the SRF is a complete joke. It’s only purpose is to pretend that something meaningful is taking place when clearly it’s not.

Target 2

On top of it, a quick check of the Bundesbank Target2 Balance shows peripheral Europe owes Germany a new record high €860 billion!

EU Banking System is Insolvent

-

The deposit insurance scheme is a joke.

-

The Target 2 system is a fundamental flaw of the Eurozone. Target 2 debts will not be paid back,

-

Nor will Italy, Greece, and other countries collect on non-performing loans.

-

To prevent runs on banks the EU is investigating a scheme to freeze bank accounts. The next logical step is ban on cash altogether

-

The EU banking system is insolvent.

This material is based upon information that Sitka Pacific Capital Management considers reliable and endeavors to keep current, Sitka Pacific Capital Management does not assure that this material is accurate, current or complete, and it should not be relied upon as such.

Recommended Content

Editors’ Picks

EUR/USD trades with negative bias, holds above 1.0700 as traders await US PCE Price Index

EUR/USD edges lower during the Asian session on Friday and moves away from a two-week high, around the 1.0740 area touched the previous day. Spot prices trade around the 1.0725-1.0720 region and remain at the mercy of the US Dollar price dynamics ahead of the crucial US data.

USD/JPY jumps above 156.00 on BoJ's steady policy

USD/JPY has come under intense buying pressure, surging past 156.00 after the Bank of Japan kept the key rate unchanged but tweaked its policy statement. The BoJ maintained its fiscal year 2024 and 2025 core inflation forecasts, disappointing the Japanese Yen buyers.

Gold price flatlines as traders look to US PCE Price Index for some meaningful impetus

Gold price lacks any firm intraday direction and is influenced by a combination of diverging forces. The weaker US GDP print and a rise in US inflation benefit the metal amid subdued USD demand. Hawkish Fed expectations cap the upside as traders await the release of the US PCE Price Index.

Sei Price Prediction: SEI is in the zone of interest after a 10% leap

Sei price has been in recovery mode for almost ten days now, following a fall of almost 65% beginning in mid-March. While the SEI bulls continue to show strength, the uptrend could prove premature as massive bearish sentiment hovers above the altcoin’s price.

US economy: Slower growth with stronger inflation

The US Dollar strengthened, and stocks fell after statistical data from the US. The focus was on the preliminary estimate of GDP for the first quarter. Annualised quarterly growth came in at just 1.6%, down from the 2.5% and 3.4% previously forecast.