ECB Preview: The end of the asset purchasing at the time of uncertainty may reposition Euro higher

- The ECB is almost unilaterally expected to end its asset purchasing program in December signaling no rate changes.

- The ECB is set to continue to reinvest the proceeds for "an extended period of time" that will not start until "after the ECB begins to raise rates."

- The ECB is also expected to leave the door open for rollover of TLTROs, but it is expected to launch it in Q1 2019.

- The macroeconomic projections should deliver minor revisions of a weaker 2018 growth and lower oil prices.

The ECB is widely expected to announce the end of the asset purchasing program on its December Governing Council meeting with the ECB President Mario Draghi emphasizing that the reinvestment should carry over until 2019 and well past the horizon of next rate increases.

The reinvestment profile should ease market liquidity and support the market sentiment with mild credit easing as the ECB may opt for reinvesting proceeds from maturing securities within a longer time frame than within two months as it is currently the case.

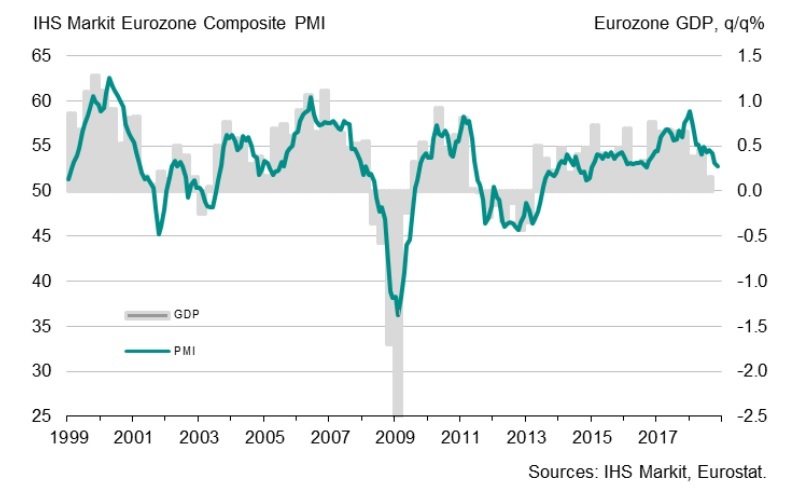

The ECB is unlikely to revise the macroeconomic projections dramatically, but the downward revision is expected. The forward-looking indicators like IHS/Markit’s PMIs being already at its lowest level since September 2016 and Germany, the Eurozone’s powerhouse, also recorded a steep deceleration in economic activity with composite PMI falling to the lowest level in last 47 months in November.

The level of the economic activity in the Eurozone is now indicating a fourth-quarter GDP slowdown to 0.3% Q/Q, suggesting the region remains stuck in a soft-patch. This should be also reflected in December ECB’s macroeconomic projections together with lower oil prices that fell -22% in November.

Given the combination of softer economic projections and smoothe end to asset purchasing program, the overall outlook for interest rates should be slightly bearish indicating no immediate rush in monetary policy normalization. This should see a rate hike expectations moved beyond 2019 to Q1 2020. Despite dovish rate outlook the Euro could be boosted on the pledge of further stimulus to come and take a lift higher as it is currently trading near its cyclical low of 1.1213. The repositioning past December rate hike from the Fed with the newest outlook for US rate could see Euro lifted towards the end of the year on repositioning.

The Eurozone PMI and GDP growth

Source: IHS/Markit

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.