ECB Preview: Draghi set to play risks down and keep the path of QE ending in December clear

- The ECB is expected to confirm its firm path of monetary policy normalization by confirming this December as the end of its asset purchasing program, before moving on to rates.

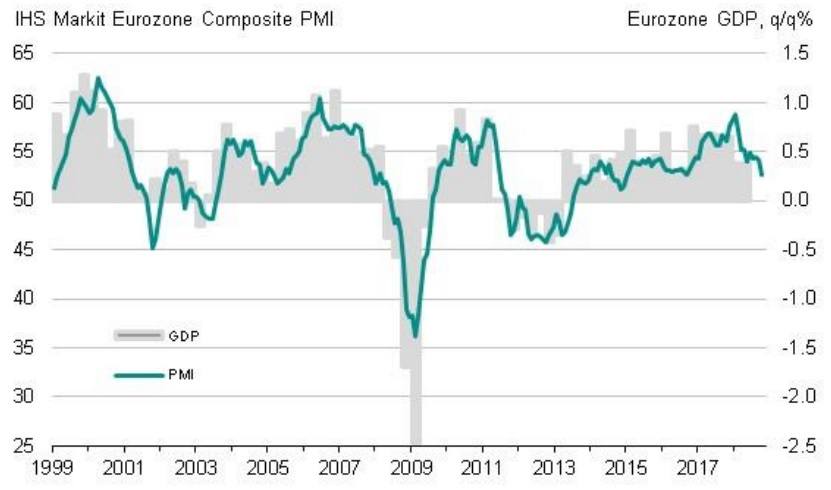

- The ECB President Mario Draghi will be confident in avoiding the political interference regarding his homeland Italy while downplaying the current economic slowdown in forward-looking indicators like PMI.

- The ECB’s stance of keeping the rates and the outlook unchanged is unlikely to support EUR/USD that fell to the lowest level since August 17 of below 1.1400 with any signs of monetary tightening by ECB will strongly support Euro.

The ECB is unlikely to alter its path of gradual removal of the economic support in form of scaling the asset purchasing program down with the definite end in December. While central banks in the US and in Canada are already firmly walking the path of the interest rates normalization the ECB is still in the phase of scaling the asset purchasing down with the first rate hike in Q2-Q3 next year.

The reason for the monetary policy stability is inflation related. Inflation is stable at the target, so there is no need for the ECB to act. The economic growth is possibly sliding lower as the business surveys report the lowest level of the economic activity in the last 2 years, but that might be easily blamed on Trump’s induced trade uncertainty that is particularly concerning Germany, the Eurozone’s largest economy.

In Germany, the private business activity PMI fell to the lowest level in three-and-a-half-year in October with manufacturing PMI down 1.3 points to 52.3 and services PMI fell 2.3 points to 53.6 in October.

The Eurozone business surveys indicate that the fourth quarter GDP is set to rise by 0.3% Q/Q only with sub-indices in new orders indicating further slowdown ahead.

While September the prospects of a possible economic downturn were less pronounced, this time it is different. Apart from the business activity slowing down, the budget discipline of the Italian government is a subject to increased uncertainty with the European Commission returning the fiscal plans back to Italian originators for corrections. Such a move is little seen in the history of the traditional fiscal sinners of the European Monetary Union that reflects the push for unity elsewhere.

The Italian fiscal position is also closely correlated with the financial market's moves. The Italian risk premium rose by 175 basis points since the previous Italian parliament was dissolved last December and the coalition of populists took the power. The risk is also reflected in the EUR/USD that fell ten big figures from 1.2300 level in March when the new Italian government was formed.

Regarding the FX market move, any hints of possible monetary tightening by ECB will be reflected in Euro strengthening with immediate effect as the gradual interest rate normalization in the US is already reflected in the FX rate.

The Eurozone PMI and GDP growth rate

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)