Commodities outlook: Can gold, oil and metals stay bullish in 2021?

It’s been an incredible year for commodities as the global pandemic has induced some historic moves in the prices of key commodities such as gold and oil. Growth commodities like oil and industrial metals, whose fortunes are more directly tied to economic performance, have rallied hard since March when markets were flooded with stimulus and look set to finish 2020 on a positive note. The safe-haven gold, which had been on the rise long before the pandemic, has not been having the best of times lately but is still on track to end the year with strong gains. But as everyone hopes that better times lie ahead in 2021, can these commodities sustain their uptrend?

Gold rally: from trade tensions to a global pandemic

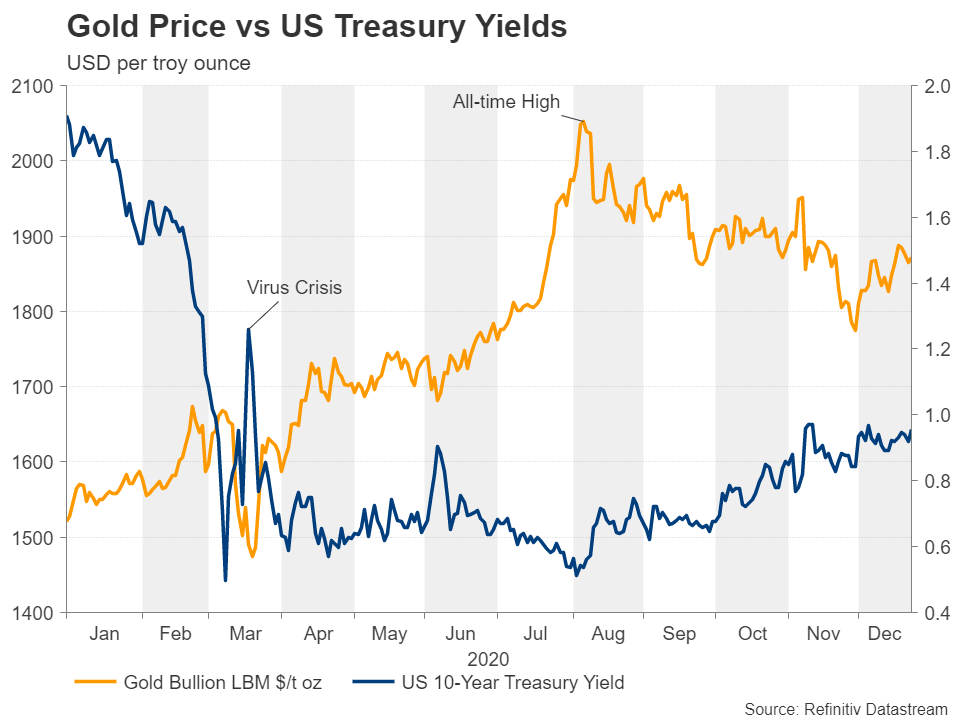

Gold has had a ball of a time during Trump’s reign as his administration’s trade fight with China and antagonistic behaviour towards both America’s allies and foes triggered a flight to safety. But the rally didn’t really kick off until the summer of 2019 when trade frictions boiled to a level that started to hurt economic growth. Although tensions had eased substantially in early 2020, by this point, a global round of monetary policy easing was already underway, which means there were other factors pulling gold higher. And as the year draws to a close, those factors are not only still at play, but they are more prominent than ever in driving the precious metal.

The outbreak of the coronavirus has sparked central bank intervention on an unprecedented scale, with interest rates around the world being slashed to near zero and massive bond purchases depressing sovereign bond yields. All this makes gold an attractive investment, even when the market panic has subsided and risk appetite is on the up.

Gold outlook may depend on Fed’s inflation tolerance

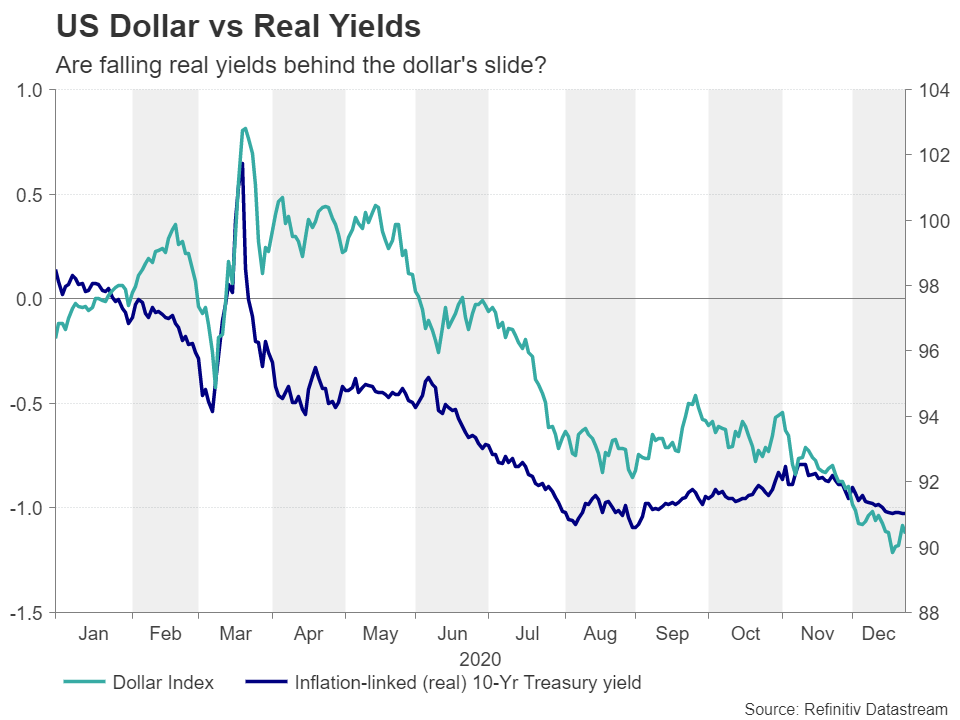

Amplifying gold’s allure during this period of unprecedented central bank action has been the weaker US dollar. A deprecating dollar increases the purchasing power of other currencies, boosting demand for bullion, which is priced in dollars. But this isn’t simply about the greenback’s fall from grace as there is also an inflation story here.

The Federal Reserve’s tolerance of higher inflation has lifted market expectations for future inflation in the United States, pushing real yields below those of other countries. Heading into 2021, how inflation expectations pan out, and if actual inflation does pick up, how soon it would be before the Fed starts to become uncomfortable are probably what will determine how much further the dollar will slide before hitting a bottom.

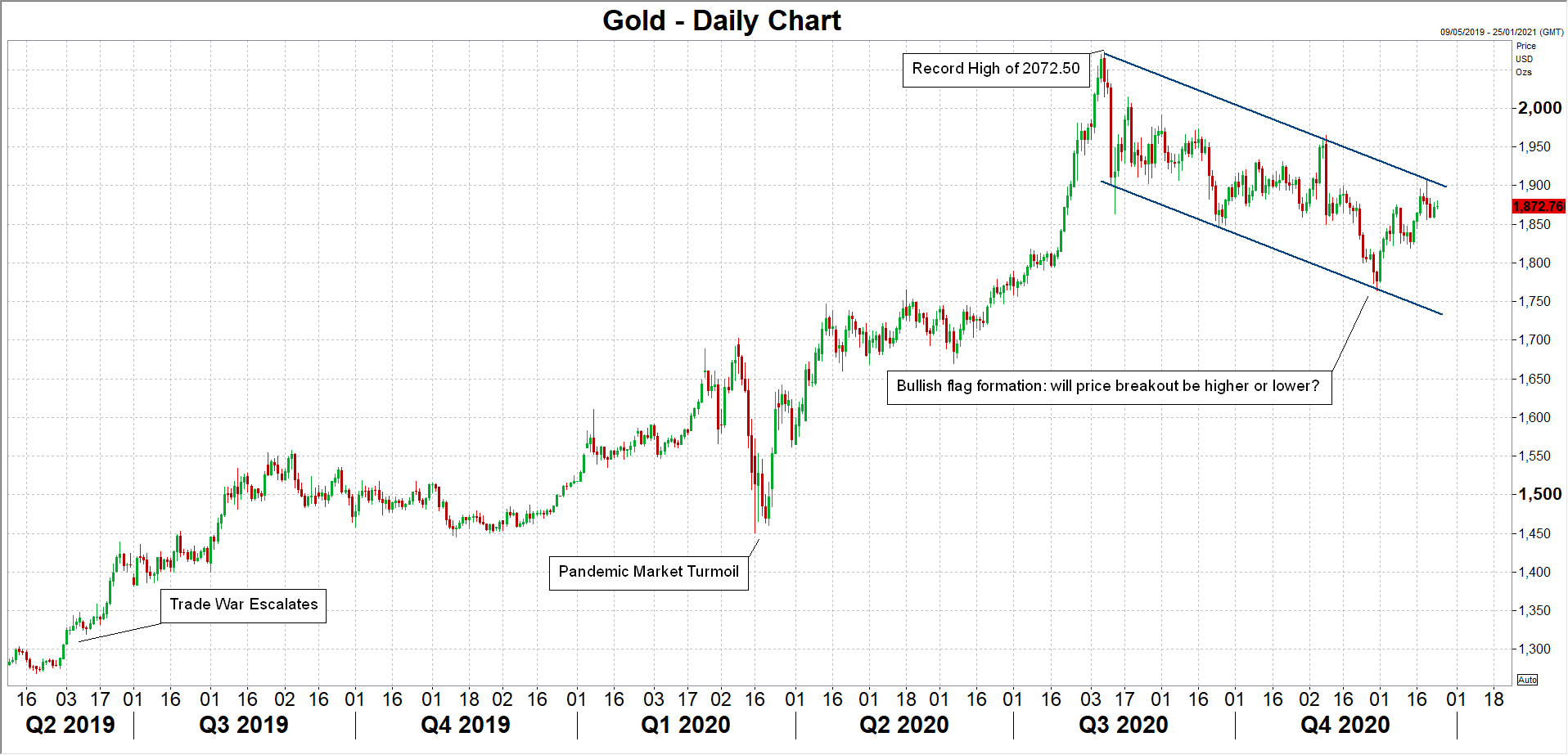

From a technical perspective, gold’s bullish flag formation suggests an upside break is more likely than a downside one – an indication perhaps that the dollar’s selloff is far from over.

Is the worst of the pandemic really over?

However, there are other reasons besides the retreating greenback that could boost gold. The global fallout over the discovery of a new and more contagious strain of Covid-19 in Britain has highlighted how the worst of the virus impact may be yet to come, despite the vaccine breakthrough. Even on that front, investors may have become over optimistic on how quickly mass inoculations can be delivered so that enough of the population has been immunized to allow significant rolling back of restrictions within the next 12 months.

On the brighter side, apart from there being no end in sight to the abundance of fiscal and monetary stimulus, which should keep the recovery going, it could be much quieter in the geopolitical arena following Joe Biden’s victory in the US presidential election. A continuation in the improving economic picture and calmer relations between the US and its partners could eventually turn gold’s current downside correction to a more permanent downtrend.

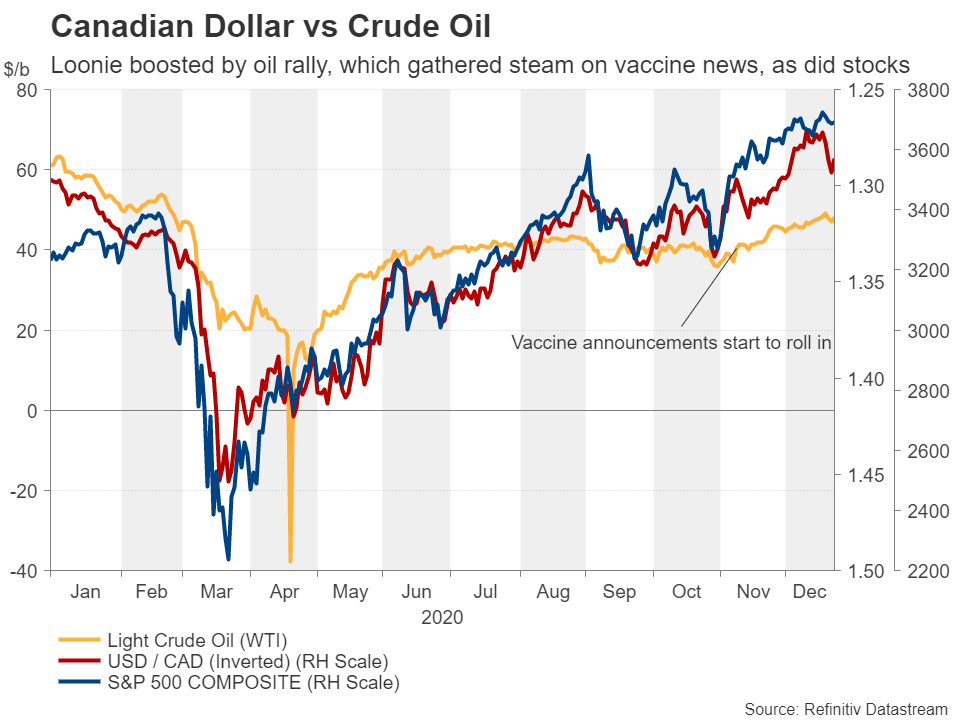

Oil prices back from the brink

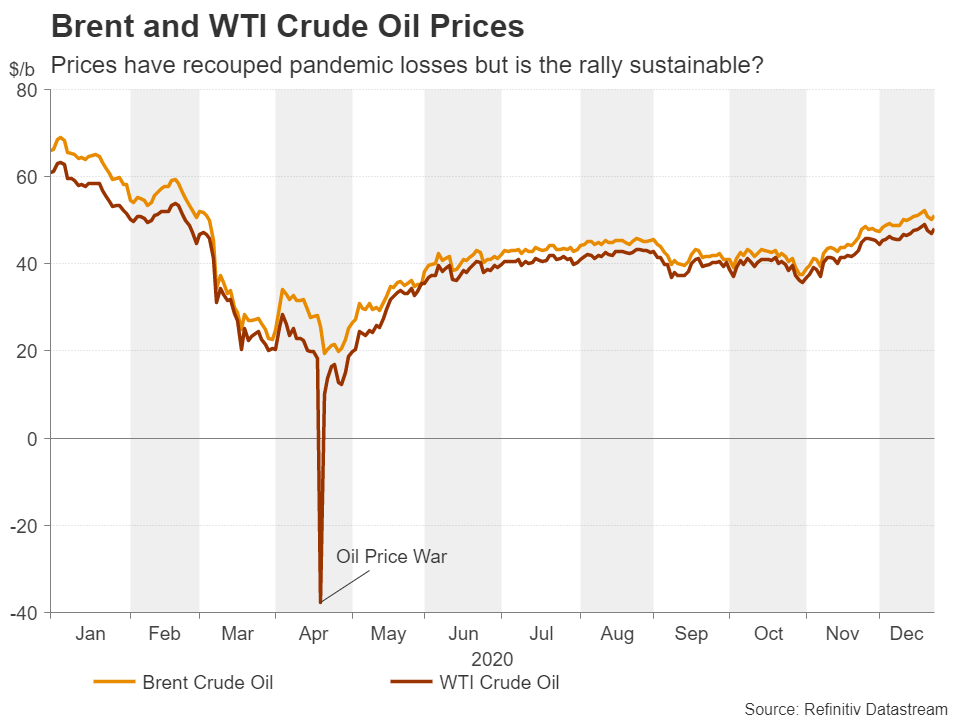

Saudi Arabia and Russia couldn’t have picked a worse time to start a price war as it was their standoff during the height of the first virus wave in April that triggered WTI oil futures to nosedive into negative territory for the first time in the commodity’s history. The swift U-turn by Saudi Arabia and decisive action by OPEC and its allies that soon followed ensured that oil prices not only bounced back to more ‘reasonable’ levels but that the price rebound was durable.

Judging by where prices stand as the year is about to close, it’s safe to say the production cuts have been successful, with Brent crude back above $50 a barrel and WTI not far behind. However, that’s still some distance from the $60 plus levels that both benchmarks were trading at the beginning of the year so there is scope for additional gains in 2021 should the global economy recover as predicted.

New lockdowns bring new headaches

However, the oil industry is not out of the woods yet as analysts have wound back some of their more optimistic forecasts for demand after Europe was plunged into a second lockdown in November. The strict virus curbs could last until next spring, holding back fuel consumption as Europeans are forced to spend more time at home. But restrictions have also recently tightened in other parts of the world, including Australia and the United States, risking a further delay in demand rising to pre-pandemic levels.

The uncertainty about the outlook is not fully reflected in prices, however, as they’ve already more than recovered the losses incurred in March and April. Hopes that the vaccine rollouts will bring about a swift end to the pandemic are propelling the latest upswing in prices. But can the bullish structure last for much longer without some of the clouds hanging over the medium-term horizon clearing?

OPEC+ plan may not save the oil rally

One of the other big clouds is doubts about how OPEC and non-OPEC countries will manage the easing of output cuts in the new year. The plan agreed in December to hold monthly meetings to fix new production levels was seen as a compromise amid growing reluctance among members to commit to tough quotas. The monthly review frequency could lead to greater volatility in oil prices in 2021. But the main worry is the danger that supply increases at a faster pace than demand, which could set oil on a new downward path, particularly if the recent price hikes encourage more US shale production.

But just as the stimulus and vaccine euphoria is drowning out the worries in equity markets, the same applies for oil and other growth commodities. As long as the euphoria holds, oil-linked currencies such as the Canadian dollar should also be able to maintain their bullish posture.

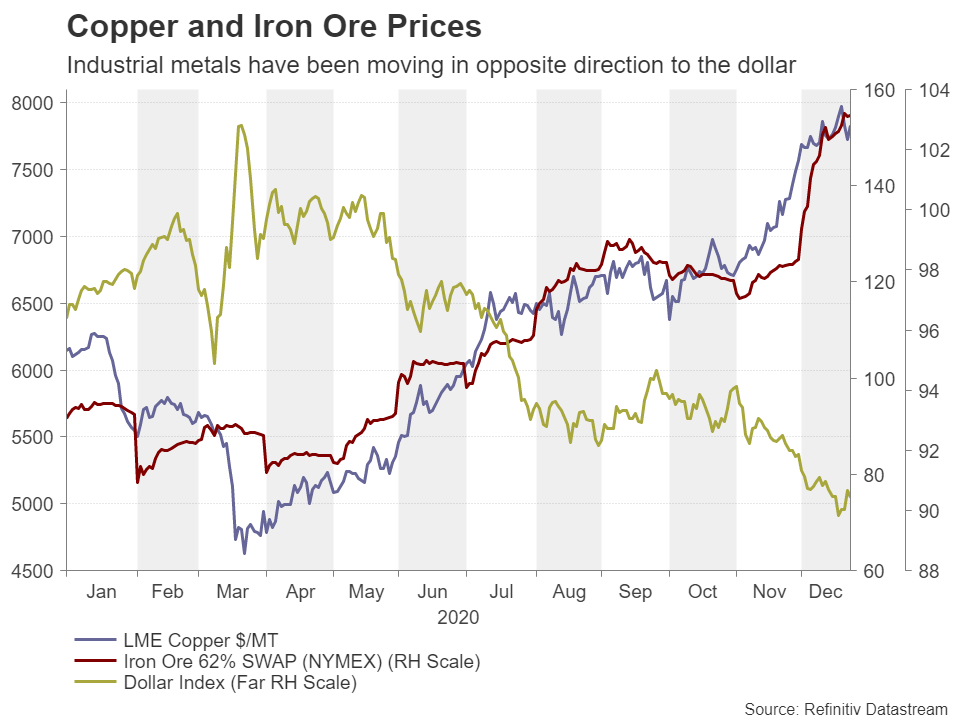

Industrial metals defy the pandemic gloom

Precious metals – led by gold and silver – may have had a strong year but industrial metals also had an outstanding 2020. The two don’t necessarily move in tandem with each other as most precious metals behave like safe havens while industrial metal prices tend to be driven by economic growth prospects. But they do have something in common and that is they are both negatively correlated with the US dollar. Hence, the fate of industrial metals lies as much in the hands of the dollar as it does on the growth outlook.

Given that the dollar is expected to remain bearish in 2021 and major economies are anticipated to maintain their recovery course, there’s not a lot standing in the way of the rally. Additionally reinforcing the positive shift in the economic backdrop is the fact that manufacturing output has been much less severely impacted from the lockdowns of the second wave. So even if 2021 gets off to a shaky start, demand for extensively used metals such as copper should not be significantly dented.

Can metal prices extend their climb much further?

Copper is up more than 25% so far this year, while iron ore has surged by about 65%. The strengthening recovery in China and optimism that vaccines will soon spell the end of virus restrictions have added extra impetus to the stimulus-led rally. But has much of the vaccine jubilation been priced in by now, and if so, how sustainable are these gains going forward?

Another risk for 2021 is a worsening diplomatic and trade row between Australia and China, which may unsettle markets and generate some volatility if China were to broaden its punitive tariffs on Australian agricultural products to metals as well. The Australian dollar would be the worst hit from tariffs being imposed on Australian resources exports, though the direct effect on metal prices might be less obvious.

Ultimately, it’s a dollar story

All in all, many of the trends that began after the stimulus taps were opened in March and once vaccines became a reality will likely endure in 2021, at least in the first half. But while the path of the global recovery will greatly determine the next direction for all three commodity classes, the US dollar’s own outlook and Fed policy may ultimately decide what 2021 holds for the major commodities.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics. Following graduation, he joined PricewaterhouseCoopers in the Business Recoveries team, where he was responsibl