Bank of England update: A mixed bag

BoE holds the Bank Rate at 5.25%

As widely expected, the Bank of England (BoE) held the Bank Rate on hold at 5.25% for a sixth consecutive meeting, its highest level since 2008. However, what was key today was the central bank signalled it could be getting closer to easing policy in the summer, possibly as early as June’s meeting (60% chance of a cut currently priced in) or in August, which is fully priced in at the moment. Markets are currently leaning in favour of the latter as a date to cut rates by 25bps, which, incidentally, is quite similar to the European Central Bank (ECB) but quite different to the Fed’s potential rate path, with the Fed funds target rate anticipated to remain restrictive until the end of the year.

Should the BoE step up and cut before the Fed, this will likely weigh on GBP/USD and increase the chances of imported inflation: imported goods and services would be more expensive.

MPC Voted 7-2 in favour of a hold

More movement towards a cut in the Bank Rate was seen at today’s meeting as Deputy Governor Sir David Ramsden switched from a hold vote to a cut, joining external MPC member Swati Dhingra. Albeit somewhat expected, this is a clear dovish signal of a central bank manoeuvring towards easing policy; the question is when. It should not come as much of a surprise that Ramsden made the shift, given comments expressing confidence in the disinflation process and that inflation risks remain ‘skewed to the downside’. Interestingly, history tells us that following a change in voting by Ramsden, the majority of the MPC members tend to follow suit; most recently, in late 2022, when he voted for increased hikes, the majority followed.

Following the rate announcement, BoE Governor Andrew Bailey communicated that a cut as soon as June is not out of the realm of possibility. Bailey added: ‘Inflation has now fallen to just above 3.0%, and we expect it to be close to the target in the coming months; that’s encouraging’. However, the BoE Chief warned that the central bank is not at a point where they can cut rates and will consider forthcoming data; he also addressed the perception that the BoE would not move before the Fed does, commenting: ‘There is no law that says the Fed moves first’.

Ahead of the next BoE meeting, the upcoming inflation (22 May and 19 June) and wage data (14 May and 11 June) will be a key watch.

The March UK CPI revealed a slower-than-expected pace of disinflation across all four key metrics (headline and core for both YoY and MoM). While all four reports released higher-than-expected numbers, the year-on-year reports continued to exhibit a disinflationary trajectory. Headline inflation rose +3.2%, down from 3.4% a month earlier (consensus: +3.1%), and core inflation increased +4.2% from the previous +4.5% print in February (consensus: +4.1%). Month on month, both headline and core reports saw inflation rise by +0.6%, matching February’s data. However, this was higher than forecasts of +0.4% and +0.5%, respectively.

BoE projections

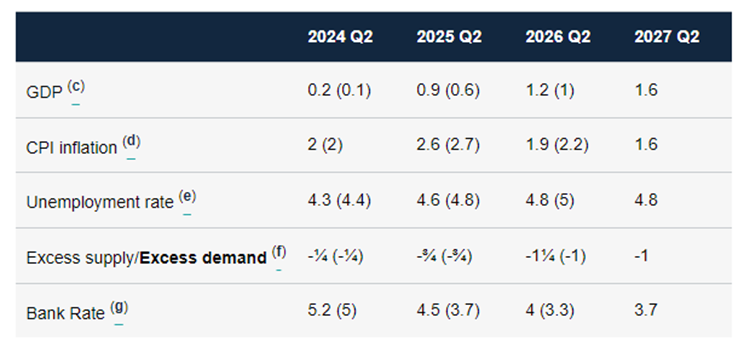

We also had the quarterly release of updated economic projections from the BoE, showing a downgrade in inflation forecasts, which was largely expected. The central bank still projects inflation to reach the 2.0% inflation target in Q2 of this year (unchanged from the previous forecast) and then subsequently increase to approximately 2.6% in the second half of the year (down from 2.7% in the previous forecast). By Q2 2026, inflation is anticipated to be 1.9% (down from 2.2%) and then by 2027, slowing to 1.6%.

Unemployment was also downgraded, with Q2 expected to be 4.3% (from 4.4%), increasing to 4.6% (from 4.8%) in 2025 and remaining at 4.8% for 2026 and 2027.

In terms of GDP growth, economic activity is expected to grow by 0.4% in Q1 of this year, followed by 0.2% in Q2, indicating that the mild technical recession seen in the second half of last year was in the rear-view mirror. As a note, tomorrow welcomes UK growth data at 6:00 am GMT; market consensus heading into the data expects we’ll see another expansion in March. This follows economic expansion in January and February’s reports: +0.3% and +0.1%, respectively. According to Bloomberg’s estimates, the median forecast indicates a +0.1% expansion in March (estimate range between +0.2% and -0.2%), with the QoQ release forecast to print +0.4% for Q1 (estimate range between +0.4% and +0.1%).

Summary and market snapshot

Overall, it was quite a mixed bag at today’s meeting.

Inflation was downgraded (expected/dovish), with growth upgraded (hawkish). The vote split saw a key member switch from hold to cut, but this was not enough to surprise markets given Ramsden’s comments and some desks speculating that this may occur (should Bailey have shifted to a cut as well, then this would have been a different kettle of fish and more dovish and likely triggered a more sizeable move), and the Bank Rate was left unchanged.

The immediate aftermath of the rate announcement saw GBP fall versus its peers, though as of writing, the GBP/USD is trading in positive territory and has reclaimed pre-announcement levels. Gilts popped higher following the release but swiftly pulled back to trade pretty much unchanged, and the FTSE 100 also rallied but similarly pulled back to the pre-announcement level shortly after before turning higher – the market index on the verge of refreshing all-time highs.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,