A China fuelled rally runs out of steam as caution sets in once more [Video]

![A China fuelled rally runs out of steam as caution sets in once more [Video]](https://editorial.fxstreet.com/images/Macroeconomics/Countries/Asia/China/great-wall-and-chinese-flag-7816729_XtraLarge.jpg)

Market Overview

It would appear that yesterday’s rally was drive just on the notion that China’s state run media encouraged its people to buy stocks to foster a “healthy bull run”. So perhaps it is of little surprise that a rally fuelled by hot air looks set for a retracement today. China may have managed to pull further equity gains, but other Asian markets are more cautious, also futures elsewhere are turning back. The focus in recent weeks has been far more on the concern that COVID-19 infection rates are rising alarmingly in the US and hampering the re-opening of the economy. There are also pockets of lockdowns being reinstated across other countries such as Germany, Spain and Australia. A bull rally seemingly priced for a perfect global economic recovery may need to prepare for disappointment. It is our view that disappointment could become a theme for Q3. The headline of the ISM Non-Manufacturing data, beating expectations at over 57 sounds great. However, this only notes expansion versus the month of May, which could simply be negligible but broad based. Also the employment component remains at 43 and in contraction. As many US states are hit by rising infection rates, July and through Q3 it could be a difficult period for a sustainable economic recovery. Sentiment across major markets has a negative bias today. Yields are falling back, the dollar is looking to reclaim some ground lost from yesterday’s risk rally. Oil is lower and equities are lower as higher risk assets are hit. The Aussie is also in the firing line today as the Reserve Bank of Australia held rates at +0.25% and did little to change its recent message of forward guidance (will not increase rates until there is progress towards employment and inflation goals). With the city of Melbourne re-imposing a lockdown, this is hitting the Aussie today.

Wall Street closed strongly higher last night with the S&P 500 +1.6% at 3180, but futures have dropped back today (E-mini S&Ps -0.4%). Asian markets are split with the Shanghai Composite +1.3% but Nikkei -0.4%. European indices are faltering early today with FTSE futures -0.6% and DAX futures -0.6%. In forex, the dollar is performing strongly across the major pairs, with AUD and NZD being the main underperformers. In commodities, gold is flat as it consolidates yesterday’s gains, whilst oil is around -1% lower.

The second week of the month is usually fairly quiet on the economic calendar, and this week is fairly typical of that. The US JOLTS jobs openings for May are expected to be 4.85m. This is down from 5.05m in April, with it having been over 7.00m in February. It is important to say that this data is quite old now, with June’s economy re-opening and data rebound expected to show up in next month’s JOLTS.

Aside from the data, it will also be worth keeping an eye out for FOMC board member Randall Quarles who speaks at 1800BST.

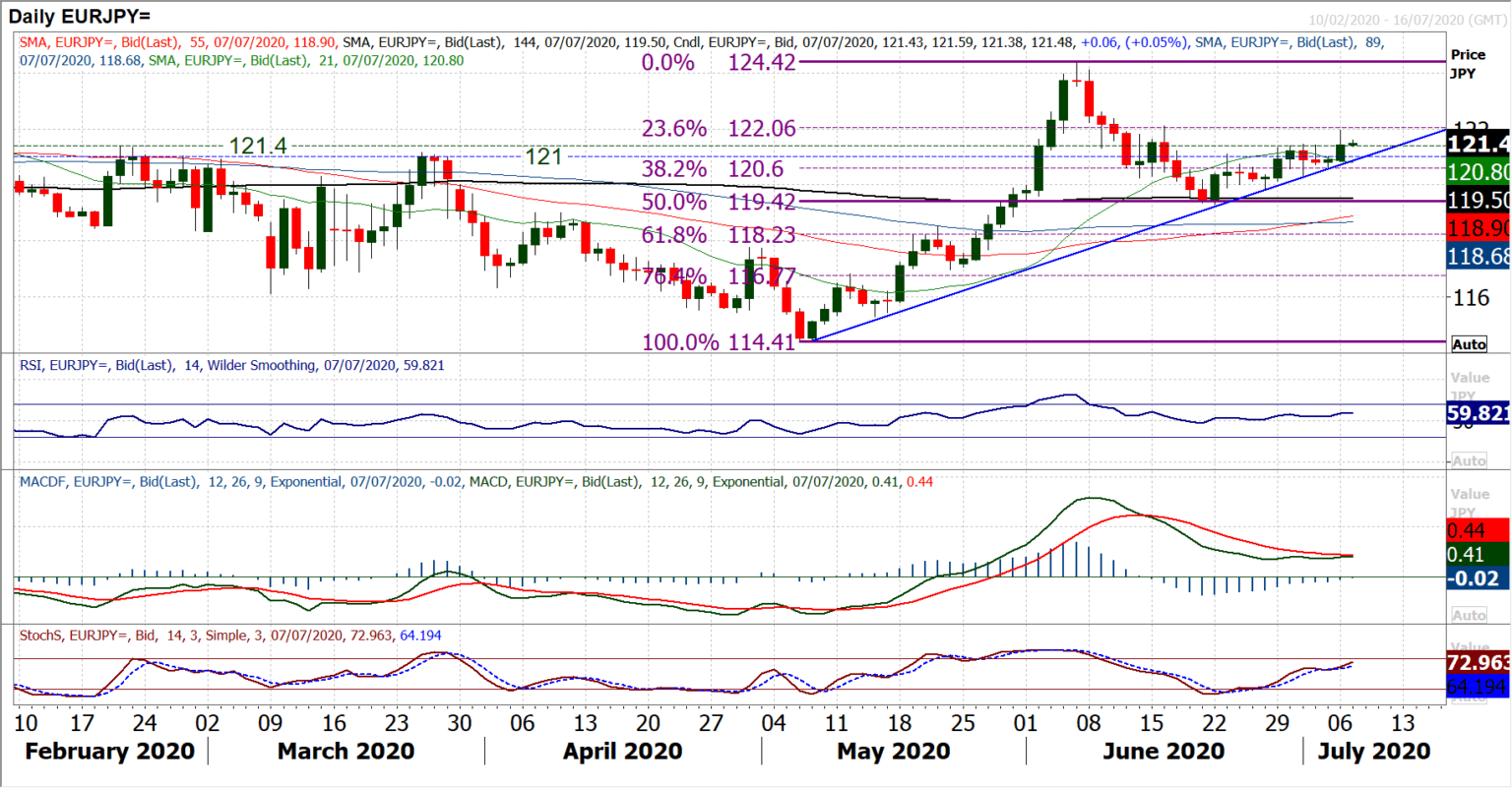

Chart of the Day – EUR/JPY

With the EUR/JPY bulls starting to find their feet in the past week, the technicals are taking on a far more encouraging configuration for long positions again. A retreat to what is now an eight week uptrend is again starting to post a succession of higher lows and higher highs. The past couple of weeks have been characterised by the market testing the old resistance band 121.00/121.40 which has been capping the highs. However, a strong bull candlestick yesterday with a close (just) above the 121.40 resistance is steadily pulling the market higher once more. Momentum indicators are now making progress higher, with RSI close to the 60s again, a bull kiss on Stochastics and MACD lines on the brink of a bull cross. The next step forward will be for a close above the 23.6% Fibonacci retracement (of 114.40/124.40) around 122.05 which would open for a full retracement to 124.40. The consistent near term retreats to find support at the uptrend, suggest that weakness is a chance to buy. The trend line comes in at 120.85 today, with any supported weakness into 121.00/121.40 being a good opportunity for renewed long positions. The 38.2% Fib at 120.60 is added support, whilst a failure below 120.25 would abort the immediate bullish outlook.

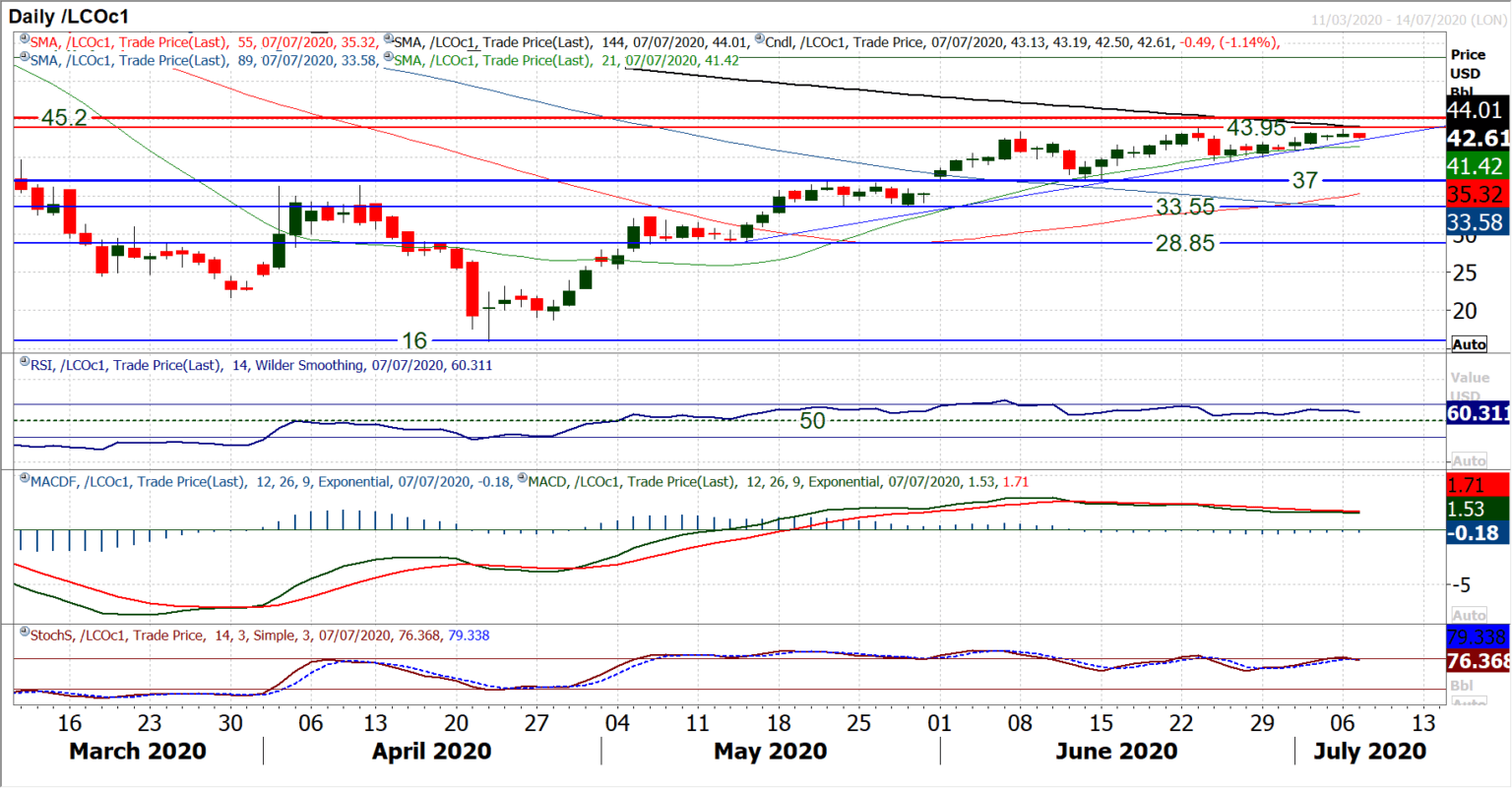

Brent Crude Oil

The trend higher continues as Brent Crude posted another a positive close along the run up towards a test of $43.95, the June high. However, the magnitude of the positive candles is notably reduced from the strength of bull candles that were being posted throughout May and into June. Although these are still positive sessions, there is a threat that this could be a sign of fatigue ahead of the key $43.95 resistance. The appetite to buy into intraday weakness on oil is set to be tested today, with an early slip back. With a seven week uptrend underpinning the run higher at $41.90, this is a basis of support that the bulls will be keen to defend. Momentum remains positively configured, but once more not as decisively strong as it has been during recent weeks. It is interesting to see that if the market does close lower today, the Stochastics will be bear crossing. A bear cross has been the precursor to a consolidation or corrective slip in the past two months. There is initial support at $42.30 and then more considerable between $41/$42. Key resistance at $43.95 is a barrier to the big March gap down from $45.20.

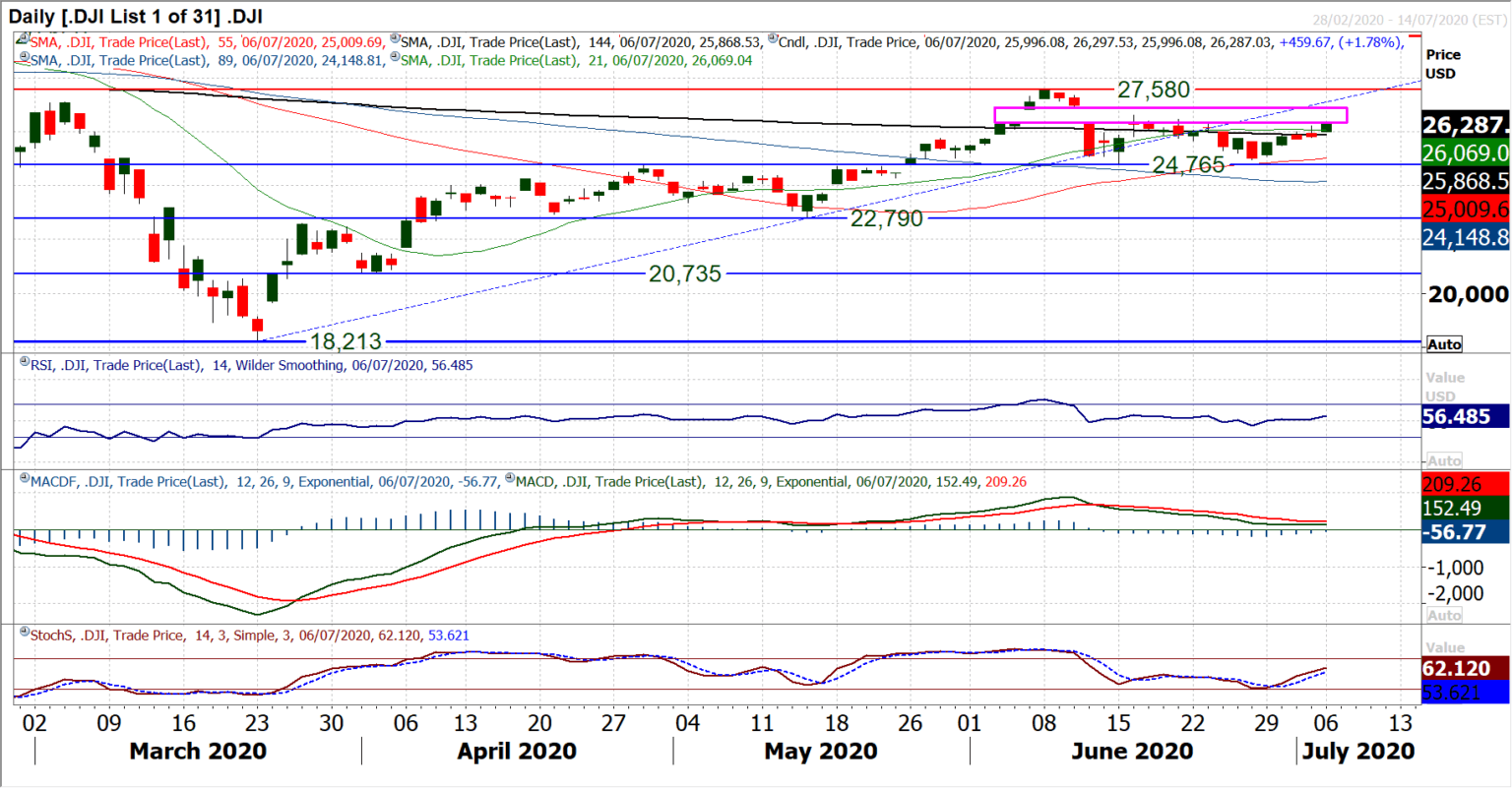

Dow Jones Industrial Average

After a day of strong gains on Wall Street, the Dow is once more up around a test of the near term resistance of the range 24,845/26,610. This comes as the Dow is still yet to close the big June gap 26,385/26,940. This is subsequently a key moment for the near to medium term outlook. Another failure to close the gap left by the island reversal will once more ask further questions of the longevity of this rally. The daily momentum indicators suggest that there is some encouragement, with Stochastics rising at three week highs above 50, MACD lines looking on the brink of turning higher and RSI into the high 50s. However, given the importance of resistance from the latter June highs between 26,315/26,610 and Dow futures ticking lower by around -80 ticks early today, how the bulls respond in this session could be really important. A negative candle with a close under initial support 25,780 would really hit the rally prospects. If the bulls can respond to buy into weakness, as they have done in the past week, to ramp up the pressure on the overhead resistance, then closing this gap can be a real possibility.

Author

Richard Perry

Independent Analyst