2016/17 Cotton Production: Weather in India, Pakistan and La Nina’s impact on Major Cotton Producing Countries

The August 12th USDA-FAS World Market Report, continues the trend in falling cotton production estimates for 2016/17, lowering their estimates from last month by ~1% to 101.582 million bales (22.117 million metric tons). The reduction in production predictions driven by a combined decrease of 1 million bales in India (-1.82%) and China (-2.33%) were more than enough to overcome the positive outlooks in countries such as Brazil (+3.9%). Despite USDA estimates increasing from July-August for the United States (+0.005%), the third leading cotton producer, they were rather disappointing when compared to the June-July estimate increase of 1 million bales (6.75%). So what is driving the estimated production decreases? Two dominating factors, drought and reduction in planted area, have influenced the downtrend in predicted production.

The cotton production superpowers of China and India, combined account for over 50% of the world's cotton with the United States a distant third. As shown in figure 1 the top 7 cotton producing nations account for ~84% of global production. In last week’s article, regarding sugar production in India; I discussed the severe drought that has plagued India. In addition to India the impacts of this multi-year drought have been felt in Pakistan, especially in the eastern regions along the border with India. I have read several articles stating that this year's summer monsoon has alleviated the drought; while these articles are not necessarily wrong special considerations need to be taken for those looking into cotton production for 2016/17. The primary consideration, especially this year, is the “phenology” of cotton, which can be defined as the interaction between the weather and cotton specifically as it relates to individual “growing stages”. This article, divided into two sections, will first discuss the potential abiotic stress (drought) will have on this year’s crop production in India and Pakistan while also looking forward at what to expect regarding future weather and cotton production in India and Pakistan. The second section, covering global cotton production, places special emphasis on the reduction in China’s planted area and production along with an around the world synopsis of the impact of La Nina conditions on major cotton growing nations.

2016/17 Cotton and Weather in India and Pakistan

Along the border region of Pakistan and India lies a core of global cotton production; containing the provinces of Punjab and Sindh in Pakistan and the states of Gujarat, Rajasthan, Haryana, and Punjab in India. This relatively small area of states and provinces has a substantial influence on global cotton production, accounting for a staggering ~17-19% of the world's cotton production or approximately the same amount as Brazil and the United States combined. In addition to Indo-Pakistani border core a secondary core encompasses central and southern Indian states, including the second and third leading cotton producing states in India of Maharashtra and Andhra Pradesh, which account for ~13-16% of global cotton production. Data acquired from the United States Department of Agriculture (USDA) demonstrates the importance of India and Pakistan in global cotton production with a four year average of global cotton production percentage at 33.06%. To better account for the influence of weather on cotton production separate examinations of the Indo-Pakistani region and central/southern India. Each of these cores has distinctive traits related to weather and cotton production that when delineated give an increased understanding of the variability of cotton production and the influence it has on global cotton production specifically in 2016/17.

As is present in most agricultural region there exists significant differences in cultivation practices between regions in India, with the Indo-Pakistani border region having the earliest planting dates and relying heavily on irrigation. There is little water where it is needed most. The Gujarat Plains, supplying 25-30% of India's cotton over the past 4 years, has been hit the hardest with little hope for recovery. Monsoon rains, which have been plentiful in other states, didn't arrive with much intensity until recently, still Ahmedabad at the center of the Gujarat plains has reported average precipitation totals for the monsoon season however when looked at more closely it can be seen that the precipitation arrived late with nearly 3/4 of their precipitation being received in the past 10 days. Precipitation arriving late resulted in cotton planting area along the Indo-Pakistani border drastically decreasing, with some districts reporting upwards of 60% less planted area, as farmers shifted to alternative crops. The presence of whiteflies, poor germination rates, and severe water deficit stress during the squaring-flowering period will greatly reduce the yields of any cotton that was planted in the Indo-Pakistani border core, especially the early crop from the northern parts of India.

In comparison to the Indo-Pakistani border region the central and southern regions of India have had excellent summer monsoon conditions. Regions of Maharashtra and even parts of Gujarat that delayed planting until the arrival of the monsoon will see yields significantly higher than last year. Planting in the central region of India received ample moisture prior to planting allowing for high germination rates and alleviating concerns regarding soil moisture. Despite this has still been some concern expressed regarding the full recovery of lakes, rivers, and reservoirs, used for irrigation, which were at or near record lows during the drought. After looking at both monsoon conditions and long range models I believe that concerns will be alleviated as significant rains continue to fall across the west and portions of central India with the rain likely stretching as far west as the Pakistani border. Currently, monsoon rain is tapering off over the past week across a region extending from Kerala and Karnataka in the south northward into the central states of Maharashtra and Madhya Pradesh and the northern Indian state of Uttar Pradesh. While the weekly deviations from normal are down 25-50%, this should cause few issues in central and northern India due to significant rainfall earlier in the summer monsoon season resulting in average to above average rainfall, since June 1st. Concerns, do exist for the far southern state of Kerala which is down 30% from average for the monsoon. This concern extends into southern Karnataka where deficits of 18-20% have been reported. As a whole Karnataka is reporting deficits of ~13% with the lowest deficits reported from central into northern portions of the state. This is important when considering the aforementioned reservoir levels. Major reservoirs used for irrigation, such as the Tungabhadra Reservoir in central Karateka and the Almatti dam which holds back the largest reservoir in the Upper Krishna Irrigation Project. Assuagement for drought stricken reservoirs is further supported by correspondence with those on the ground and releases from the Indian government. According to India’s Central Water Commission the nation’s reservoirs, as of August 24th, are at 65% of live storage capacity and 102% of average availability with respect to the last ten years; with reports from those on the ground across the agricultural region reporting increases to 70-75% of capacity. This is a substantial recovery from even earlier this year when a government release in early August reported India’s main reservoirs to be 45% of capacity. This is positive news for future agricultural endeavors, however as previously mentioned delayed rainfall will severely impact cotton production in the western parts of India and Pakistan, specifically in the southern into central portions of Sindh, the second leading cotton producing state in Pakistan. Issues with irrigation water from the Rohri canal resulted in delayed planting and likely reduction in germination rates in the districts of Tando Muhammad Khan, Tharparkar, Badin, Hyderabad, Matiari, Tando Allahyar, Umerkot, and Sanghar. In contrast the largest cotton producing state of Punjab, with 2016-2017 production targets of ~9.5 million bales, did not experience issues with water supply during the sowing period. While on the topic of germination rates and biotic stressors such as the pink bollworm and whitefly and with the conflicts between Monsanto and the Indian government, regarding cotton seed, in the news. I feel it is important to discuss some of these issues and how they affect buyers, farmers, and traders.

When considering potential yield, quality, and other features of soft commodities many variables are considered, however there are few that are commonly overlooked and with good reason. Typically those involved in cotton or any soft commodity trading are aware of agricultural practices and features of the commodity and region they specialize in. Yet there are traits specific to the varieties of every soft commodity grown within each region that are habitually under considered or inadvertently disregarded. In my experience the most common of these is the status and prevalence of selectively bred and/or genetically modified (GMO) varieties within each region. This leads us back to the issues with Monsanto and the Indian government. Monsanto, the world’s leader in seed production, has introduced GMO varieties of cotton to India over the past several years leading to India surpassing China in 2015/16 to become the largest cotton producing nation. Of particular importance is GMO varieties containing the bacillus thuringiensis gene, more commonly known as the Bt gene, which works to limit the biotic stress specifically damage done by pests such as the pink bollworm. While strains containing the Bt gene are quite prevalent in all areas of India, barring parts of north and northwest India, there are issues with their effectiveness. In contrast to the cotton grown in the United States where extensive research is conducted resulting in the most technologically advanced seed being planted; conflicts between Monsanto and New Delhi over genetically modified cotton has led to Monsanto substantially lowering their interest in the region and pulling GMO seeds from the Indian market. This has resulted in issues with the effectiveness of the available seed which is often older and the result of multiple backcrosses between parent lines and less than ideal selection methods. As a result these hybrids have a weaker Bt gene expression or in simple terms a “weaker” variety that can be left susceptible to bollworm. Personally, I am deeply concerned with the future of the cotton industry in India if seed companies are not allowed to introduce hybrids that are developed to optimize yield for the region. Continued conflicts will likely result in a decrease in research aimed at the Indian cotton market and at worst a complete pullout by major agricultural companies from India. In addition to issues with varieties in India, Pakistan may have even more prevalent issues due to the widespread use of uncertified seed leading to poor germination rates and lower cotton quality.

This brings us back to the topic of potential issues regarding yield losses from pests and the effect that weather has on them. The pink bollworm, which the Bt gene is successful at limiting, thrive under wet and cloudy conditions during the pre-harvest period with issues surrounding the effectiveness of the GMO varieties in India farmers, buyers and traders should ensure they look closely at reports of infestations. While, currently not of a great concern one should carefully follow both the rainfall trends in Eastern Pakistan and Western India as we progress into October and November along with reports of pink. Reports are currently positive with the few reports of pink bollworm limited to replantings due to the drought in Gujarat, however after discussions with an agronomist on the ground in India I am closely watching another pest, the whitefly, in Northern India. At the moment the whitefly is well contained in isolated pockets across the north, but if an outbreak were to occur the lack of effective pesticides makes the potential for damage to the cotton crop a constant concern. The damage to last year’s cotton crop in the Indian states of Punjab and Haryana was exceptional and the effects are still being felt into the current year with planting of cotton in Punjab reaching a 61 year low. Meteorologically, whiteflies thrive under hot and humid conditions with limited rainfall. The good news is as of recent excessive humidity and heat has not been particularly prevalent with respect to normal, however over the past week diminished rainfall has occurred. As of present the threat appears fairly low, but with past outbreaks, such as last year, causing severe issues traders and those involved in the cotton industry should monitor this region for any sign of increased whitefly activity.

Global Cotton Production: Reduction of planted area in China and Synopsis of Weather in Major Cotton Producing Countries

Of special concern is China, the second leading producer of cotton, continues to see production and area planted slashed. The latest USDA report estimates production down by 2.33% (~0.5 million bales) from last month’s estimate and 4.55% (~1 million bales) from 2015/16 while planted area is down 0.05 M ha (1.72%) from last month’s prediction and 0.2 M ha (6.56%) from last year. The policies implemented in 2014/15, regarding the cotton industry, by the Chinese government are blamed by many including myself for the drastic reduction in Chinese cotton production over the past couple of years. Since 2014/15 to the current USDA predictions production has dropped by 30% (1.55 M ha) with total area planted falling by 35.23% (9 million bales). To put that into a perspective; since 2014/15 China’s claim to the global market has dropped 3.5% from 25.2% 21.7% of global cotton production (Figure 1).

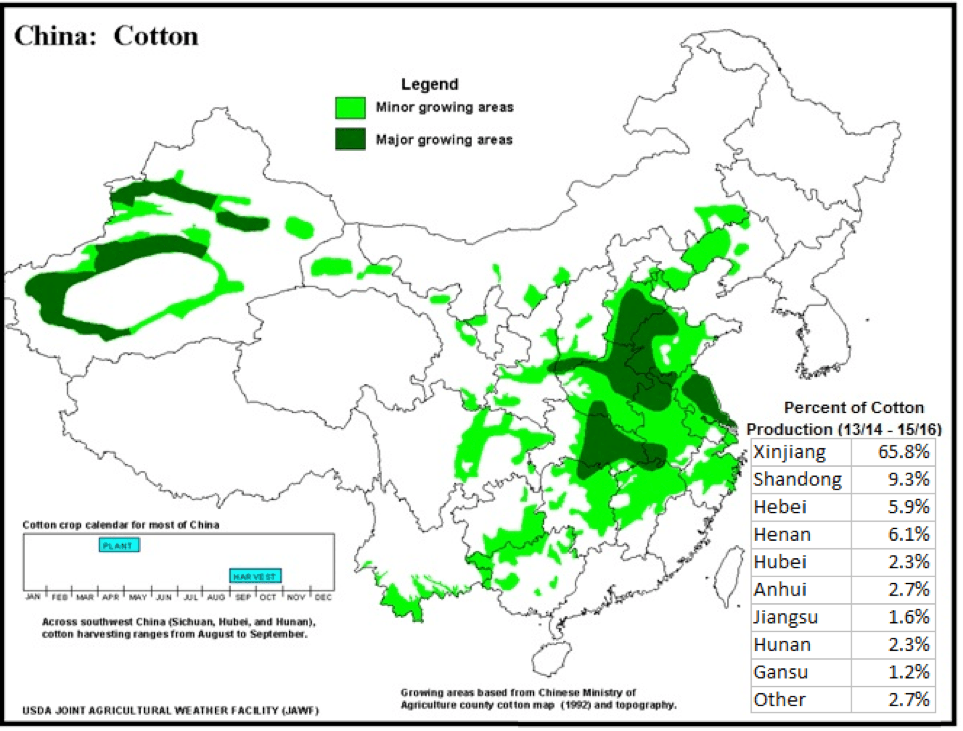

As can be seen in figure 2, which is compiled from USDA-FAS stats and modified from a previous USDA-JAWF table, China’s cotton industry is dominated by the northwestern province of Xinjiang. As producers look for cheaper labor much of the production has been shifted into the rural province. In contrast to other cotton growing regions of China; Xinjiang is known for its excellent conditions and is considered one of the premier regions for upland and sea-island cotton. Xinjiang’s location in an arid region, providing substantial sunshine, and with severe winters issues with pests are limited, however the region also requires intensive irrigation, the majority of which is fed by melting snow from the surrounding mountains. During average or El Nino years there is sufficient mountain runoff for the needed irrigation, however with a transition towards La Nina conditions, concerns do arise regarding sufficient winter precipitation in the mountains. The concerns, for the mountainous region surrounding the region, are a result of late winter and spring extreme precipitation anomalies during La Nina years, where, extreme precipitation events are reduced by 85%. As a meteorologist that does make me look more closely at the region and consider the potential implications it may have on yield. The USDA GAIN report on China from this past spring predicts a decrease in yield from the 4 year average for Xinjiang of 2.2% while increasing the national average by 10.5%. From correspondence with those in the cotton industry this report did not fully consider the possible impact of La Nina which leads me to feel leery of Xinjiang reaching its expected production. The one saving factor could be the presence of glaciers and year round snow cover on some of the mountains which could supply sufficient irrigation water even if there is limited snowfall. In addition to the potential implications of La Nina there are concerns with the rapid mechanization of agriculture in China. Both the USDA and private agricultural company scientists have mentioned not only the rapid mechanization, but also reports of yield losses and reduction of fiber quality, as was stated in the April 1st, 2016 GAIN report. Taking both the potential for yield losses from La Nina and the increase in acres under mechanized harvest, I am looking at below average yields in Xinjiang and with such a large percent of China’s cotton production occurring in Xinjiang I would not be surprised to see this reflected in China’s total production in upcoming USDA global cotton reports.

Continuing the discussion on La Nina, which is projected by many to intensify this winter and continue into the spring and summer of 2017 by some members of the meteorology community including myself, I will present a brief synopsis of conditions that La Nina can induce in major cotton producing nations. With an overview of China completed in the previous paragraph our attention can be turned to nations, of Brazil and the United States, where there exists the possibility for La Nina to affect cotton production.

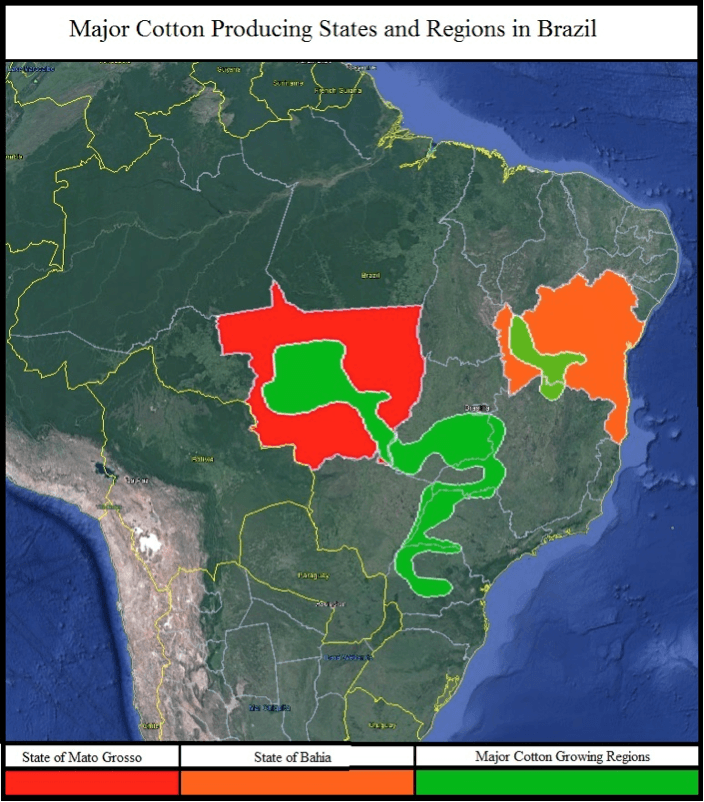

Brazil, predicted to be the 5th largest producer of cotton in 2016/17, is the only major cotton producer located in the southern hemisphere. As a result the cotton growing season is reversed from other major producers with planting occurring primarily in November and December, which we are quickly approaching, and in many cases as an intermediary between soybean plantings. As shown in figure 3 the two significant cotton growing states are Mato Grosso and Bahia, the first and second leading production states respectively. The graphic shows the majority of cotton grown occurs from central to southern Brazil near the major cities of Rio de Janeiro, Sao Paulo, Cuiaba, and Salvador this is important when it comes to determining the impact of La Nina on the cotton crop. Typical La Nina conditions during the Brazilian cotton growing season are below average temperatures across southern Brazil with increased precipitation across northern Brazil. This leads to an interesting predicament for the cotton growing region which is sandwiched between these two anomalies. Currently I am predicting average to above average precipitation occurring with the highest probability in northcentral regions of Mato Grosso, which one could arguably designate the most important cotton growing region of Brazil. In Bahia it appears currently that precipitation will be greater than the past couple years, during which the worst drought in 60-80 years occurred, and it is possible that above average precipitation will occur. For those who watched the Olympics earlier this year you may have noticed the presence of rain on multiple occasions despite this being the dry season for Rio de Janeiro and Sao Paulo. This in my opinion is a positive sign for the upcoming cotton planting season, which stretches from January to February in Bahia, and is further support to my current predictions. However there are still some issues that may arise, both of political and meteorological nature, resulting in several questions that need to be answered. First the issue of the political turmoil that is ongoing in Brazil. The political turmoil has resulted in a weakening of the Brazilian real which in turn has increased production prices, but also higher domestic prices and with strong demand farmers are in a position to have a strong ROI. Then there arises a problem that interlinks politics and the weather. The Sao Francisco River is a major supplier of irrigation for the entire region yet the Sobradinho Reservoir, the largest reservoir in the region, was reported to be at only at 10-15% of capacity in early August. I do not see it recovering this year after such a horrible drought over the past years and then there lies the issue of politics. With the volatile nature of current Brazilian politics, the big question is what decisions the government will make in regard to releasing water for irrigation and drinking. This is a question best left for a more qualified person, but it is an important issue that could quickly become an issue for the Bahia state’s cotton industry. Finally, there is the concern, while very limited, of the influx of cooler than average air into southern Brazil which often occurs during La Nina. While influxes of cooler temperatures from the south will alleviate concerns about moisture lost to evapotranspiration there always exists the possibility of issues with limits on growth if cool temperatures persist for an extended period. Cotton has a lower growing degree day (GDD) threshold of 60o F (~15.5o C) and if cooler temperatures make their way into Central Brazil the accumulation of GDDs would be limited, slowing growth and potentially impacting final yields and quality. On average daily low temperatures in Brasilia, located between Mato Grosso and Bahia, are 60-65F (15-18C) during the growing season which is near the lower threshold of the GDD; with highs near 80F (26C). With these average temperatures lying within an ideal range for GDD accumulation I do not see there being an issue even with a few periods of cooler than average temperatures. While it currently appears that there is no reason to be overly concerned I will continue to monitor both the precipitation and temperature conditions throughout the growing season.

In contrast to Brazil the United States, whose cotton industry is scattered across the southern United States with west Texas and the southern Mississippi River valley being the premiere regions of cotton growth, often encounters brutal drought and hot temperatures during the summer when La Nina conditions are present. For 2016/17 dry and warm conditions in west Texas will be prevalent during the winter. Depending upon the endurance of the La Nina event these conditions will continue across most of the cotton belt along with the Midwest and Great Plains region which could cause significant issues especially in west Texas. Cotton planting typically peaks in late April into early June depending on locality and field conditions, with harvest occurring from as early as late September to as late as early December. With such a long interval between now and the cotton season it is difficult to pin down exactly the intensity or even duration of this La Nina event, however based on current trends and correlation analysis with past events I feel confident it will persist into summer which will negatively impact the United States grain and cotton crops. My confidence is great enough that I am working to determine the ideal price and month for which corn futures would have the greatest return. In such a short synopsis I cannot not cover the entirety of the world nor get into every topic, such as the negative precipitation anomalies that are occurring in northern Brazil, but will gladly answer questions from those interested.

Author

Paul Carlone

Bargueton Ltd

Paul Carlone, the founder of Marketable Meteorology, is a meteorologist specializing in the financial, energy, and agricultural sectors.