Top 5 semiconductor stocks for 2022: AMD leads high-growth sector

- 34% capex growth in 2021 should lead to continued high demand for new chip technologies in 2022.

- The semiconductor industry is forecast to grow revenue by 10-15% in 2022.

- Fabless chip designers are projected to grow revenue faster than foundries.

In a year that has seen the S&P 500 gain 24% year to date, it is unsurprising that so many passive investors would be happy with the progress of their portfolios. Normally, lacklustre sectors like energy and financials have performed the best, even outperforming usual stalwarts like technology stocks.

Semiconductors were one of the more satisfying industries to hold in 2021. The Philadelphia Semiconductors Index (SOX) has returned 36% so far with just two weeks left in the year.

SOX YTD chart comparison with top semiconductor stocks

Much of the underlying alpha for the industry came from the supply shortage caused by the global logistics logjam, which has boosted unit prices in the industry. Unusually high demand also became a major trend in 2021 due to the reduced 2020 covid-related demand drop that had many consumers and companies move purchases from 2020 to 2021. By some estimates, it has caused foundry orders to move from 14 weeks to 20 weeks, and the automotive industry especially has suffered due to shortfalls in chip shipments.

Regardless of the global supply constraints, research group IC Insights expects revenue to continue soaring in the semiconductor space throughout next year as capex surges.

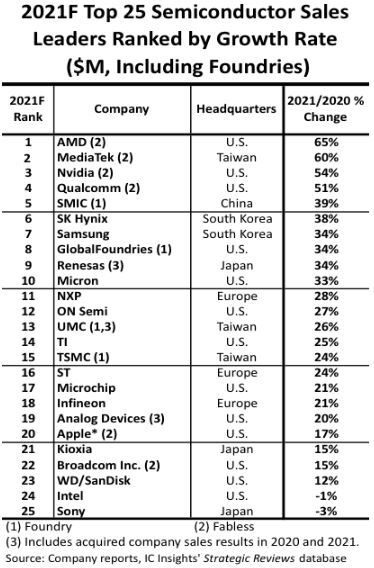

The group of analysts released a report in early November saying it expects Advanced Micro Devices in particular to post a revenue increase of 65% this fiscal year, which runs through the first half of 2022. This places AMD in first place on IC Insights' list of the fastest-growing semiconductor companies, above Nvidia (3rd, 54%) and Qualcomm (4th, 51%).

This is not to say that sales will continue to grow for the industry in the estimated 25% range like this year. Several forecasters see revenue growth averaging between 10% to 15%. IC Insights pegs the average CAGR for 2021 to 2023 at 13%.

Secondly, a 34% growth in semiconductor industry capex in 2021 should lead to demand growth as foundries find the capacity to meet demand for components in the new 3-nanometer segment.

-637752434668763196.jpg)

As you can see from the chart above, semiconductors for personal computers are expected to drop by 5% in 2022, but as a whole this demand shortfall should be made up for by 5% growth in the smartphone market and 9% for light vehicles. Smartphones are a much bigger market than PCs, so there is absolute drop-off.

FXStreet’s top five semiconductor stocks for 2022

Advanced Micro Devices (AMD)

This is the least surprising pick on the list. AMD has seen its prospects grow by leaps and bounds in 2021. As mentioned, with revenue expected to grow by 65% in fiscal 2021, this stock seems unlikely to slow down.

Bank of America said recently that AMD stock is now preferred by hedge funds compared with competitor Intel (INTC). Greater institutional ownership should protect retail investors from any major sell-off.

Wall Street consensus is equally bright. The average of 35 analyst predictions sees AMD earnings per share (EPS) rising 26% to $3.32. This gives the stock a forward P/E ratio of 41.

Revenue already exploded in 2021, but analyst forecasts put the average at $19.1 billion for the full year 2022. This would mean growth of 18% YoY and a forward P/S ratio of just 8.6.

That is key because though AMD stock is up 47% year to date, it continues to trade at a much lower multiple than sector leader Nvidia (forward P/E ratio of 55, forward P/S ratio of 22.5).

Secondly, the (as of yet) unfinalized merger with Xilinx should begin to bear fruit for AMD in 2022. As such, expect AMD to become even more competitive with Intel and forecasts to get upgraded in the second half of the year.

Last, AMD’s announced partnership with Meta Platforms (FB), formerly known as Facebook, requires an extreme ramp up in sales of its processors for the latter’s data center expansion strategy. Meta plans to ramp up capex throughout 2022, a great deal of which will increase AMD’s top line.

Applied Materials (AMAT)

The “picks and shovels” approach is always a popular means of gaining exposure to any industry. Though few prospectors strike it rich during a gold rush, those who sell everyone else the tools necessary to become a miner have a much more certain chance of cashing in.

One of the best ways to approach semiconductors is to invest in one of the primary providers of materials and equipment to the industry – Applied Materials. The company’s Semiconductor Systems unit sells various manufacturing equipment that is used to fabricate semiconductor chips and integrated circuits.

With 2020 and 2021 seeing foundries raise capex to its highest level on record and still remain unable to meet demand, investment in the company’s equipment is expected to be brisk. IC Insights expects capex to grow by 34% YoY in fiscal 2021, most notably in the foundry segment, and some of this spending will assuredly bleed into the second half of the year as well.

It is also a value pick. While AMAT stock has exploded 70% YTD, it remains cheap. The stock is trading at less than five times forward revenue with a forward P/E of 18. This is partly due to management offering lower forecasts for next year, but that is what makes it attractive. The market expects little from AMAT, which means any upward revisions or earnings beats could help this stock fly.

-637752436730927159.jpg)

Broadcom (AVGO)

Broadcom is a leader in wireless, networking and infrastructure software for the semiconductor industry. The San Jose-based company’s WiFi 6E technology is expected to fly off the shelves in 2022 as customers adopt the faster speeds of the 6-GHz spectrum.

AVGO stock gained 45% in 2021 as the company became uber profitable. Now management is becoming more shareholder focused in the new year. Just this month they announced a $10 billion share buyback program for 2022 and raised the dividend by 14%.

As the Federal Reserve begins reducing its bond buying and even possibly raising rates in the second half of next year, expect investors to move to cash cows like Broadcom that have immaculate earnings records and extremely high margins. The company’s adjusted EBITDA in 2021 was an unheard of 60%.

AVGO is the safe choice in this bunch. With a forward P/E ratio under 19 at the moment, it would be understandable if it saw multiple expansion in 2022.

ASML Holding (ASML)

ASML Holding is another pick-and-shovels choice. The company has a near monopoly of the extreme ultraviolet systems used to print circuit designs, as much as 90% of the market.

With capex set to continue pumping away until the chip demand is satisfied, the Dutch company is expected to be in high demand by industry leading foundries like Taiwan Semiconductor (TSMC).

Morgan Stanley named ASML a top pick in Europe for 2022, saying it should greatly benefit from the continued chip shortage and 5G rollout. The investment bank released an enormous upgrade to the equipment manufacturer’s 2022 revenue.

It said it could see $34 billion in full-year turnover, though the average Wall Street consensus expects less than $25 billion. Maybe this expectation is too high, but if Morgan Stanley is proved correct, ASML shares will once again see massive upside.

76% of analysts have buy ratings on the stock, and the average price target provides for consensus share price appreciation of 22%.

Qualcomm (QCOM)

Qualcomm shed much of its boring facade in 2021. As a major supplier of modems to Apple (AAPL) for years, it was priced at a lower multiple than other high-flying semiconductor companies.

The company is now on a new path that will focus it on the automotive and Internet of Things (IoT) sub-sectors. As such, management said in November that its total addressable market would rise from $100 billion to $700 billion by 2030.

"Qualcomm is at the beginning of one of the largest opportunities in its history, enabling a world where everyone and everything is intelligently connected," said CEO Cristiano Amon in mid-November.

QCOM is now priced 13% below fairly conservative price targets, and 68% of analysts give it a buy rating. The stock sports a P/E ratio of 17 and a P/S ratio just above 5. This is a news play. As QCOM makes major investments and announcements in 2022, expect the stock to gain on brighter expectations.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Clay Webster

FXStreet

Clay Webster grew up in the US outside Buffalo, New York and Lancaster, Pennsylvania. He began investing after college following the 2008 financial crisis.