S&P 500 Forecast (SPY) (SPX): Four reasons why the S&P 500 can power to 5,500 in 2022

- Demand to remain strong, but supply side to improve in H2.

- Inflation growth to slow in H2.

- P/E growth to remain strong but slow down.

- Fed policy to remain market friendly and slower than anticipated.

Forecasting, like economics, is a dismal science, but occasionally one can reap the rewards of a carefully constructed argument. 2021 follows 2020 as a tumultuous year with some momentous events in the stock market. With less than a month to go, we can safely consign 2021 to one of the strongest years on record for stock market performance, and now we endeavour to forecast for 2022. Will it be another year of strong equity performance? Will inflation batter returns? Will Bitcoin blow up or takeover?

We live in interesting times, as the Chinese might say, and they certainly kept us guessing in 2021. We had the DIDI IPO that is now no more. Increased regulation and worries over Evergrande Group surfaced, as did fears over climate change and raw materials. China certainly kept itself at the forefront of investors' concerns for 2021 and will do so again in 2022.

For 2022, we forecast the major themes that investors will battle to comprehend are inflation, inflation and inflation. Everything else is merely an ingredient into that. Inflation dictates credit, which dictates asset allocation. Inflation dictates perception of price, which dictates asset allocation. Inflation dictates central bank policy, which dictates asset allocation. See where we are going yet?

For 2022 we expect inflation to moderate but not enough to totally assuage investors’ fears.

- We expect the supply side to pick up in the second half of the year, which will help inflation.

- However, we expect the demand side to remain elevated and even pick up further if covid is consigned to history. Pent up demand is still an issue and orders are still working through the system.

- Wage growth and demands will pick up in 2022.

- We expect the Fed to taper and raise rates less than expected in 2022.

- We expect corporate earnings to remain strong, but corporate earnings growth will slow.

- With interest rates remaining low and the Fed remaining a friend to markets, the TINA trade (There Is No Alternative) will get another year.

- We, therefore, forecast another strong year for US equities with a gain of 10% pencilled into the S&P 500 for 2022.

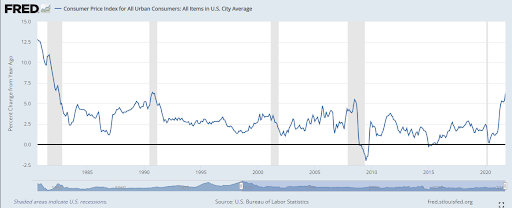

Inflation to peak in summer 2022

“Transitory” was the word of 2021, but Powell put that one to the sword in his remarks at the start of December as inflation gauges spiked in all major economic blocs. The key question remains on how we gauge inflation going forward. Currently, we base our view that massive stimulus by global central banks has had a disproportionate effect on global savings rates and now spending ratios of consumers. The Fed and others have effectively juiced consumer spending. Money supply has exploded and credit is everywhere you look. Cars, consumer electronics, jewelry – whatever you want, credit is available. Buy now, pay later.

That did not end well the last time with the US housing collapse, and it may not end well this time around, but 2022 is not likely to see the bubble burst just yet. Demand is just too strong and central bank pumping remains elevated. No, this bubble has more inflating yet to do.

The onset of covid saw global lockdowns and a consequent slump in consumer spending and demand. We saw strong v-shaped recoveries in all major global economic blocs as economies reopened. Pent-up demand led to supply issues. Demand soared for consumer products, notably big ticket items, electronics and automobiles, etc.

With supply chains struggling to resume, the knock-on effect on pricing had only one outcome – inflation. Shortages in everything from raw materials, copper, lumber, oil and notably semiconductors put upward price pressure on all sectors. Demand can quickly return to pre-covid levels, but it is more difficult for the supply side to speed things up. We are assuming Omicron is no worse than Delta (hoping, as well as assuming) and so expect the supply side to continue to recover while demand remains strong. Based on this we see inflation peaking around mid to late summer of 2022 before the supply side finally starts to bring it under control.

Since 1990 previous spikes in inflation above 5% have proven transitory, due largely to technological advancements, cheap labor and globalisation. The speed of technological development is increasing not decreasing. Labour costs in the developing world remain low, and inflation is not a concern in Asia, where most labor intensive manufacturing originates.

Fed to taper but hike slower than expected

The Fed will begin 2022 in a cautious mood as it waits for more data on Omicron and the likely economic effects. Already we are seeing some further restrictions in Europe, and UK Winter 2022 is not the time to be raising rates in our view. Come summer we expect the supply side to have picked up. We assume the pandemic will begin to ease and normality to finally return.

Much is made of the Fed balance sheet and its correlation to the S&P 500, the dreaded taper tantrum. But as we can see from the chart below, The Fed balance sheet peaked after the Great Financial Crisis in mid-2014 and remained flat before reducing in 2018 until the 2020 pandemic. The S&P 500 however rallied just over 70% during that taper period.

-637764728990959245.png)

The combination of covid winter and supply-side improvements will allow the Fed to delay its hiking cycle in our view, while the Fed watches the effects of the taper closely. The Fed has been a friend to markets for over two decades now, rarely straying off course and scaring investors too much. The message is that they have got your back. Expect more of the same in 2022. Any rate hiking cycle will be carefully and clearly signaled in advance, the first signal likely around March in our view. Markets will be allowed to prepare in advance.

Corporate earnings growth to slow from high levels

The real driver of the stock market has been strong earnings growth since the Great Financial Crisis. This has been down to unlimited availability of cheap credit, allowing unlimited funds for investment and expansion.

This time last year an argument could have been made, and was by many, that a DotCom-like crash was imminent as the price/earnings for the S&P hit nearly 40. However, taken against the exuberance of the pre-Great Financial Crisis era, this looks positively pedestrian. In any event the price/earnings ratio for the S&P has steadily declined to sit under 30 by December 2021.

-637764729955047364.png)

Price/earnings ratio for the S&P 500. Source: Macrotrends.net

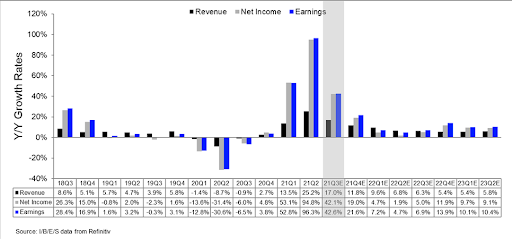

The latest data from IBES Refinitive (the industry benchmark) forecasts earnings growth to remain strong for 2022. Earnings growth peaked in H2 2021 and will slow. However, earnings will continue to grow at about 8% for the year. Earnings growth without stock price growth is highly unlikely.

Risks and unknowns

Geopolitical risks come from China and Russia. President Biden met virtually with President Putin in December and was apparently forceful in the strong defence of Ukraine. However, Putin may gamble that sanctions are not as unpalatable as a military defence by the West. After Afghanistan, the US appetite for another foreign mission may be severely diminished. Europe does not have a force of its own, leaving Ukraine extremely vulnerable. This could develop as 2022 progresses, leaving energy markets set for more gains if tensions rise. However, US midterm elections in November 2022 could leave President Biden as a lame duck president with no domestic agenda if he loses control of Congress. This is likely in our estimation and most others. With no domestic agenda possible, expect a stronger foreign policy rhetoric for the remainder of the Biden presidency. Russia may gamble on Ukraine, but all bets are off after midterms in our view. Biden will need positive spin and nothing like a new Cold War to achieve reelection.

China is China, and the regulatory crackdown on its tech sector is now a known fact for investors to decide on for their risk appetite. The Evergrande and broader real estate concerns are by now well-publicized. China’s recent move to reduce reserve requirements for its banks is the first step in policy easing, which is likely to continue for 2022. While the rest of the developed world will be tightening, China is likely to be going the opposite way. This should help contain the situation in our view, leaving the banking sector in a weakened but survivable state and the overall property sector to stumble on.

In conclusion, we see inflation peaking by Summer 2022 as the supply side improves. Demand will remain strong, meaning strong economic growth. The Fed will not raise rates until the third quarter of the year and slowly in well signaled moves. Earnings growth will slow but should still be sufficient to underpin a strong growth in stock prices. We expect the S&P 500 to gain in the region of 10 to 15% for the year, with the majority of the performance coming in the second half. Given we are likely to test 5,000 before December is out, that could leave a target of 5,500 for year-end 2022.

Technical levels to watch

Using the SPY (SPDR S&P 500 ETF) as our proxy, we identify some key levels should things get a little shaky. Obviously with all-time highs just in sight, there is no real resistance to speak of beyond the psychologically-important round number of 5,000 and then 5,500 for the SPX. The start of the year may prove tricky though, especially if covid sticks around and clogs up healthcare systems.

For the SPY, $428 is the last significant low and any retracement will just have to hold. Otherwise, the short-term bullish trend is broken. That will lead us down the next double bottom at $405. We also note the 100-day moving average at $449 and the 200-day at $430. These are important supports for the longer-term outlook, which is what we are after.

-637764730503099067.png)

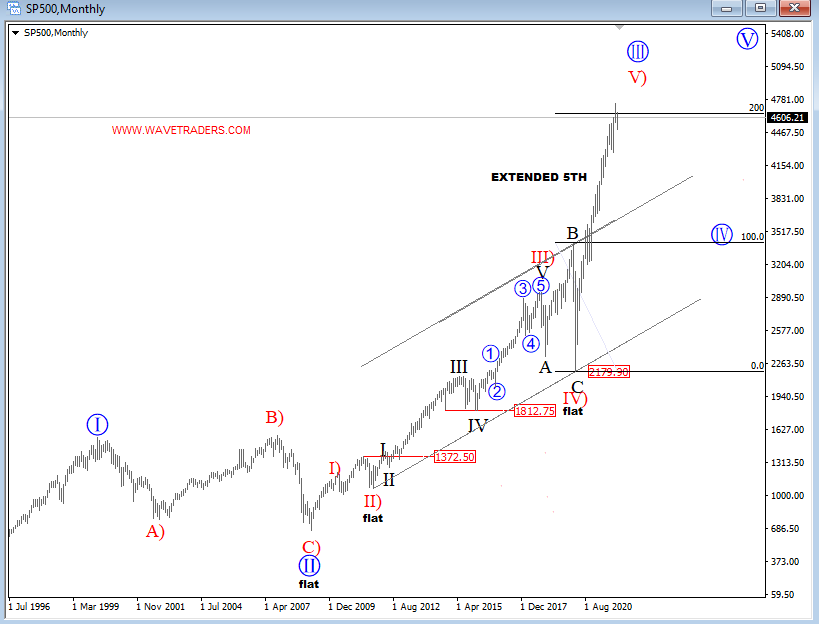

Gregor Horvat projects an ending of the upward S&P 500 pattern on his 2022 Elliott Wave analysis:

S&P 500 Elliott Wave Analysis

SP500 is coming sharply higher, out of an upward channel meaning that market is accellerating, making an extended move which can be sign of “mania cycle”. This may not continue forever, so we are aware of a fourth wave set-back. 5k is a big level.

Forecast Poll 2022

| Forecast | Q1 - Mar 31st | Q2 - Jun 30th | Q4 - Dec 31st |

|---|---|---|---|

| Bullish | 100% | 100% | 90% |

| Bearish | 0% | 0% | 0% |

| Sideways | 0% | 0% | 10% |

| Average Forecast Price | 4802.7 | 4869.9 | 5027.5 |

| EXPERTS | Q1 - Mar 31st | Q2 - Jun 30th | Q4 - Dec 31st |

|---|---|---|---|

| Alberto Muñoz | 4300 Bullish | 4750 Bullish | 5000 Bullish |

| Andrew Lockwood | 4900 Bullish | 5025 Bullish | 5100 Bullish |

| Andrew Pancholi | 5747 Bullish | 5083 Bullish | 4225 Bullish |

| Brad Alexander | 5000 Bullish | 5250 Bullish | 5500 Bullish |

| Gil Ben Hur | 4300 Bullish | 3991 Bullish | 4350 Bullish |

| Ivan Cummins | 5200 Bullish | 4900 |