ProPetro Q2 earnings and revenues miss estimates, expenses down

ProPetro Holding Corp. reported a second-quarter 2025 adjusted loss per share of 7 cents in contrast to the Zacks Consensus Estimate of a profit of 3 cents. This underperformance could be primarily attributed to weak pricing and reduced activity in the reported quarter. The bottom line was also wider than the prior-year quarter’s reported loss of 3 cents.

Revenues of $326.2 million marginally missed the consensus mark of $327 million. This underperformance is attributed to lower-than-expected service revenues in the Cementing segment, which totaled $32.4 million, down 3% from the consensus estimate. Moreover, the top line decreased 8.6% from the year-ago quarter’s level of $357 million. This was due to a year-over-year decline in service revenues from Hydraulic Fracturing, Wireline and All Other.

Adjusted EBITDA amounted to $49.6 million, down 31.8% from $72.7 million reported in the previous quarter. The figure also missed our model estimate of $61.1 million.

During the quarter, the company signed its first 10-year agreement to deliver around 80 megawatts of long-term PROPWR service to a major oil and gas operator in the Permian Basin. More than half of ProPetro’s operating hydraulic horsepower is now covered by long-term contracts, which include two Tier IV DGB dual-fuel fleets and four FORCE electric-powered fracturing fleets.

Since launching its $200 million share repurchase program in May 2023, the company has repurchased 13 million shares, representing 11% of its outstanding stock. In May 2025, the program was extended through December 2026. No shares were repurchased this quarter, as the company directed its efforts toward expanding the PROPWR business.

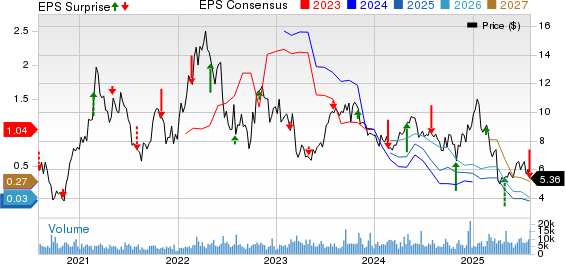

ProPetro Holding Corp. price, consensus and EPS surprise

ProPetro Holding Corp. price-consensus-eps-surprise-chart | ProPetro Holding Corp. Quote

PUMP’s pressure pumping segment

ProPetro provides hydraulic fracturing, cementing and acidizing functions through its Pressure Pumping segment. The business contributed 100% to PUMP's total revenues in the quarter under review.

Service revenues from this unit decreased 8.6% to $326.2 million from the prior-year quarter’s level. However, the figure was slightly up from our estimate of $325.4 million.

Costs and financial position of PUMP

Total costs and expenses were $329.3 million for the second quarter, which was down 7.9% from the prior-year quarter’s level. However, the amount surpassed our prediction of $322.2 million. The cost of services (exclusive of depreciation and amortization) was $253.2 million compared with $265.8 million in the prior-year quarter. On the other hand, general and administrative expenses (inclusive of stock-based compensation) were $28.5 million compared with $30.9 million in the prior-year quarter. Depreciation and amortization were reduced 28.3% to $43.3 million from the prior-year quarter's level.

As of June 30, 2025, PUMP had $74.8 million in cash and cash equivalents and $45 million in borrowings under its ABL Credit Facility. Total liquidity was $178 million, including $103 million in available credit at June-end. Long-term debt amounted to $45 million. The total debt-to-total capital was 6.5%.

In the second quarter of 2025, the company spent $73 million on capital projects but paid $37 million during the period. Of this, $30 million went to maintaining the completions business and $43 million was used for developing PROPWR equipment. The difference between what was spent and paid is mainly because some PROPWR costs were covered by a financing partner and some bills are still unpaid.

During the second quarter, the company reported $54 million in net cash provided by operating activities, $36 million in net cash used in investing activities and $26 million in free cash flow from the Completions Business.

PUMP’s guidance

The company expects full-year 2025 capital expenditures to be between $270 million and $310 million, which is about 9% lower at the midpoint compared with the previous guidance. PUMP anticipates the completions business will spend $100 million to $140 million, indicating a reduction due to expected lower activity in the second half of the year. Additionally, the company plans to allocate $170 million in 2025 and $60 million in 2026 for PROPWR equipment orders, with approximately $104 million of these expenditures expected to be financed.

During the second quarter, the company had 13 to 14 hydraulic fracturing fleets active. Due to the recent drop in oil prices, affected by tariffs and increased OPEC+ production, and a disciplined approach to asset use, the company anticipates operating around 10 to 11 active hydraulic fracturing fleets on average in the third quarter of 2025.

The Zacks Rank #4 (Sell) company anticipates securing long-term agreements for all currently ordered PROPWR equipment (220 megawatts) by the end of 2025 and plans to continue scaling the PROPWR business.

Important earnings at a glance

While we have discussed PUMP’s second-quarter results in detail, let us take a look at three other key reports in this space.

San Antonio, TX-based oil and gas refining and marketing service provider, Valero Energy Corporation, reported second-quarter 2025 adjusted earnings of $2.28 per share, which beat the Zacks Consensus Estimate of $1.73. However, the bottom line declined from the year-ago quarter’s level of $2.71. The better-than-expected quarterly results can be attributed to an increase in refining margins per barrel of throughput and lower total cost of sales. The positives were partially offset by a decline in refining throughput volumes and renewable diesel sales volumes.

The company had cash and cash equivalents of $4.5 billion at the end of the second quarter. As of June 30, 2025, it had a total debt of $8.4 billion and finance-lease obligations of $2.3 billion.

Houston, TX-based oil and gas equipment and services provider, Halliburton Company, reported second-quarter 2025 adjusted net income of 55 cents per share, which was in line with the Zacks Consensus Estimate but below the year-ago quarter’s profit of 80 cents (adjusted). The numbers reflect softer activity in the North American region, partly offset by international growth.

As of June 30, 2025, the company had approximately $2 billion in cash/cash equivalents and $7.2 billion in long-term debt, representing a debt-to-capitalization ratio of 40.4. Halliburton reported second-quarter capital expenditure of $354 million, up from our projection of $338.2 million.

Norway-based integrated oil and gas operator, Equinor ASA, reported second-quarter 2025 adjusted earnings per share of 64 cents, which missed the Zacks Consensus Estimate of 66 cents. The bottom line declined 25% from the year-ago quarter’s level of 84 cents. Weak quarterly results can be attributed to lower liquids production across major segments and reduced liquids prices. Natural declines and portfolio divestments in Nigeria and Azerbaijan also contributed to the decrease in overall production.

As of June 30, 2025, the company reported $9,472 million in cash and cash equivalents. Its long-term debt was $24,505 million. During the same time, Equinor generated a negative net cash flow of $2,579 million compared with $4,022 million in the year-ago period. Equinor’s capital expenditures amounted to $3.4 billion in the second quarter.

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Author

Zacks

Zacks Investment Research

Zacks Investment Research provides unbiased investment research and tools to help individuals and institutional investors make confident investing decisions.