Gold Price Forecast: XAU/USD rebounds from $1,810 amid cautious optimism

- Markets consolidate and weigh the convergence of sentiment between the ECB and Fed.

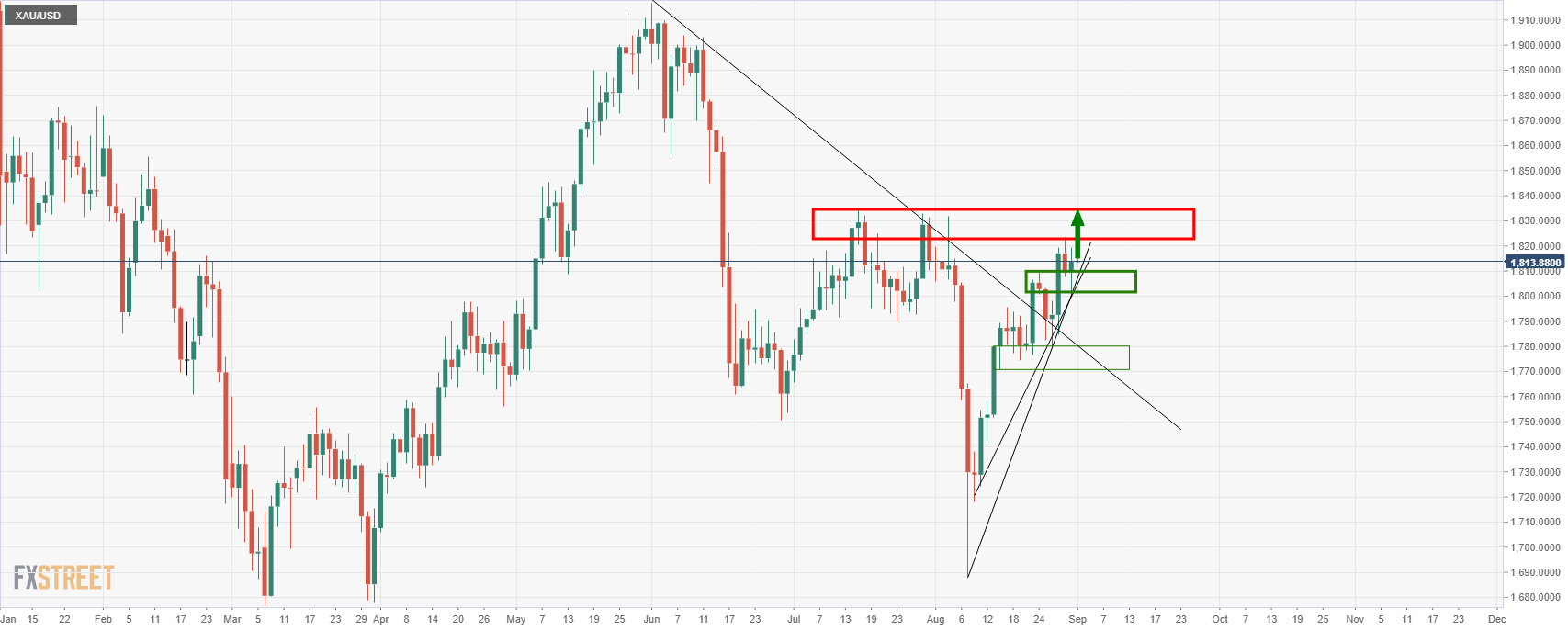

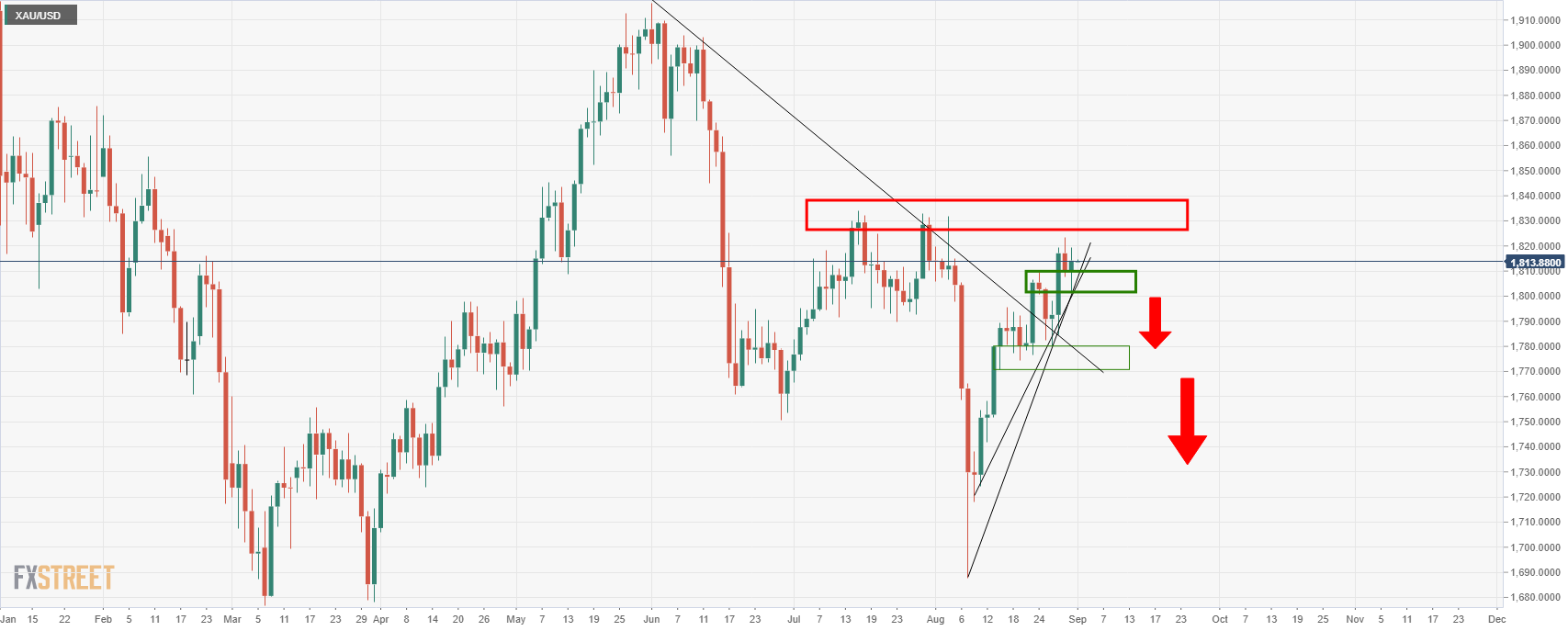

- A break of $1,800 will see the price below the dynamic trendline support. Bulls look to test $1.830s.

Update: Gold (XAU/USD) tracks mildly positive market sentiment, soft USD to portray a U-turn from the intraday low near $1,810 during early Wednesday.

In doing so, the yellow metal struggles for a clear direction after the previous day’s defense of the $1,800 threshold.

Behind the moves could be the mixed concerns over the coronavirus conditions and the central bank moves.

While the latest figures from Australia and New Zealand seem grim, China and the UK offer receding COVID-19 numbers to keep the buyers hopeful. It should be noted that the political jitters in Japan, concerning fresh elections, join the Sino–US tussles to challenge the bulls. Additionally, chatters over the European Central Bank’s (ECB) bond purchase cut, due to strong inflation data from the bloc and indecision over the Fed’s next moves amid mixed data also weigh on the market sentiment.

Amid these plays, S&P 500 Futures rise 0.20% by the press time whereas the US 10-year Treasury yields stretch the previous day’s upside to 1.326%, up 2.4 bps.

Although the risk catalysts will be more important for gold traders, the US ADP data and ISM Manufacturing PMI for August can provide the near-term market direction ahead of Friday’s jobs report.

The markets are consolidated in early Asia and gold prices are stuck near $1,815. The price of gold was ending the day higher on Tuesday, adding 0.25% by the close of play on Wall Street.

XAU/USD was near $1,815 at the close and had travelled between a low of $1,801.72 and $1,819.24 the high.

The US dollar was volatile due to month-end flows and the prospects of a less dovish European Central Bank, converging with the Federal Reserve.

EUR was strong following inflationary pressures and data reported in the Euro Area.

Flash CPI estimate for August coming out hotter than expected, (3% vs 2.5% exp and 2.2% prior).

Core inflation increased to 1.6% YoY, up from 0.7% in July. Energy costs lifted 15.4% YoY. Service inflation increased to 1.1% YoY while non-energy industrial goods lifted to 2.7%.

However, Unemployment in Germany fell to 5.5% in August following a downward revision of the previous month’s data to 5.6%.

This was sinking the DXY with the ECB’s Philip Lane as a key takeaway from the Jackson Hole, basically, promising to calibrate the QE program to financial conditions BOTH in an upwards and in a downwards direction.

Traders are seeing the shift in rhetoric as a hawkish development at a time when the Fed is dialling down its own hawkish tone.

''The markets are increasingly focusing on the possibility of the European Central Bank (ECB) commencing tapering back its stimulus measures,'' analysts at ANZ bank explained.

''And this topic may be up for discussion when it meets next week. The recent improvement in economic data means the central bank may consider scaling back the magnitude of Pandemic Emergency Purchase Programme (PEPP) under which the bank is currently purchasing ~EUR20bn of bonds each week.''

''The programme is due to expire in March and given the improvement in economic data, particularly increased inflation, it may be very difficult for the ECB to justify continuing the programme beyond March,'' the analysts explained further.

''It is also becoming increasingly likely that the rate of purchases may ease later this year if the ECB considers the economy strong enough to manage with a little less support.''

US data was also a burden for the greenback.

The August Conference Board measure of consumer confidence fell to 113.8 (from 125.1) with a decrease seen in both the current situations (147.3 vs 157.2) and expectations (91.4 vs 103.8) indices.

''Confidence was dented by the spread of the Delta variant, high inflation and the looming expiration of benefit payments on 6 September,'' analysts at ANZ Bank said.

The focus now shifts back to the US calendar this week and the US jobs market particularly.

Wednesday's Manufacturing PMIs as well as the ADP jobs report and then Jobless Claims also have the potential to stir up volatility before Friday's Nonfarm Payrolls showdown.

In terms of what to expect, Deutsche Bank US economists think that ''the pace of hiring will slow somewhat after the strong report in July, but the +700k increase in nonfarm payrolls that they’re forecasting should be more than sufficient to keep the Fed on track to announce tapering at the November FOMC meeting.

In turn, that jobs growth should see the unemployment rate fall to a fresh post-pandemic low of 5.2%.''

''If the outlook changes and the US economy slows significantly, then it would be a likely game-changer for the dollar,'' analysts at Brown Brothers Harriman warned.

Gold & DXY technical analysis

Bulls failed to close above 93.50 for month-end.

There is scope to the downside and the counter-trendline will be exposed on disappointing US data this week.

At this juncture, DXY could be looking into the abyss from a longer-term perspective:

Meanwhile, the price of gold remains in bullish territory and eyes a run to test the 1,834s.

On the upside, a break of the 1,840s opens risk to 1,870.

However, if September’s August jobs report comes in hotter than expected then the greenback could bounce back aggressively on hawkish Fed expectations.

A break of 1,800 will see the price below the dynamic trendline support.

In this regard, gold bears would be in the clear below 1,769.

Author

Ross J Burland

FXStreet

Ross J Burland, born in England, UK, is a sportsman at heart. He played Rugby and Judo for his county, Kent and the South East of England Rugby team.