For many Americans, preparing for retirement is a delicate balance between investment performance, tax benefits and anticipating future needs.

Retirement accounts such as Individual Retirement Accounts (IRAs) play a central role in this equation.

But for high-income taxpayers, direct access to certain tax advantages, such as those offered by Roth IRAs, is restricted. This is where a little-known but powerful strategy comes into play: the Backdoor IRA.

What is a Backdoor Roth IRA?

The Backdoor Roth IRA is not a special account, but a tax strategy. It allows people whose income exceeds the IRS thresholds to indirectly access a Roth IRA.

It involves contributing after-tax money to a Traditional IRA (a non-deductible contribution), then converting these funds into a Roth IRA.

This allows you to benefit from the advantages of the Roth, in particular growth and tax-free withdrawals at retirement, while bypassing income limits.

Why is this retirement strategy useful?

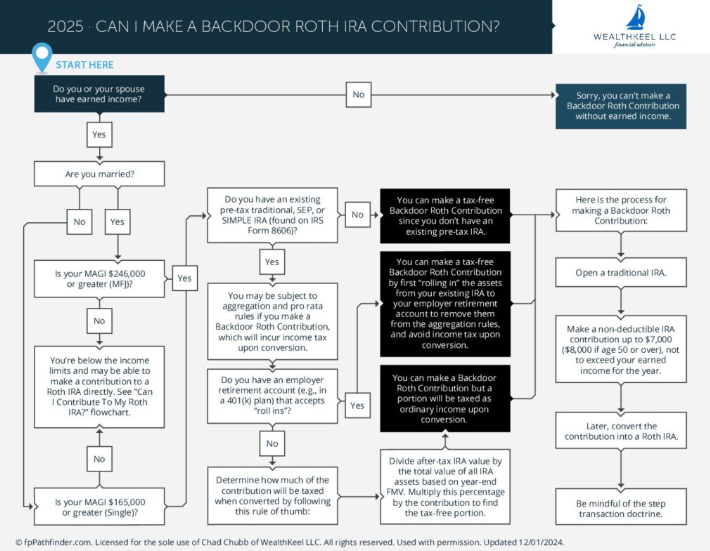

In 2025, single taxpayers can no longer contribute directly to a Roth IRA if their Modified Adjusted Gross Income (MAGI) exceeds $165,000. For married couples filing jointly, the limit is $246,000, according to the IRS requirements. These thresholds effectively exclude many executives, entrepreneurs and professionals.

Through the "back door", these taxpayers can still invest up to $7,000 a year ($8,000 if age 50 or over) in a Roth IRA. And there are no income restrictions. A rare opportunity to optimize your retirement planning strategy over the long term.

How to set up a Backdoor Roth IRA?

There are four key steps to implementing this strategy:

- Open a Traditional IRA with a broker or bank.

- Make a non-deductible (after-tax) contribution.

- Convert these funds to a Roth IRA, ideally quickly, to avoid taxable gains.

- Complete IRS Form 8606 to report the non-taxable nature of this conversion.

It is essential not to invest the funds prior to conversion, and to comply with all tax formalities, otherwise the tax authorities may wrongly consider the entire conversion to be taxable.

Beware the pro-rata rule

One of the main pitfalls of the Backdoor IRA is the famous "pro-rata rule". This rule requires that all of a taxpayer's Traditional IRAs (including SEP and SIMPLE IRAs) be taken into account when determining the taxable portion of the conversion.

For example, if you already have $90,000 in pre-taxed Traditional IRAs, and you add $10,000 in non-deductible contributions, any conversion will be considered to contain 90% taxable funds. This can result in an unexpected tax bill.

Fortunately, there are ways around this rule, including transferring old IRAs to a company 401(k), which doesn't enter into the pro-rata calculation.

What are the advantages of a Roth IRA via Backdoor?

The Roth IRA offers unique retirement benefits:

- Tax-free growth.

- Tax-free withdrawals after 59 and a half (and 5 years of ownership).

- No Required Minimum Distribution (RMD) at age 73, unlike Traditional IRAs,

- And an indirect advantage on the taxation of Social Security benefits, since withdrawals from a Roth IRA do not increase the taxable income used to calculate taxes on these benefits.

In other words, this strategy allows you to optimize your tax situation at retirement, protect your future income and even organize your succession with a Roth IRA.

For whom is the Backdoor IRA suitable?

This strategy is particularly relevant if:

- Your income exceeds direct Roth IRA contribution limits

- You've already maximized your 401(k) or don't have access to a Roth 401(k)

- You have no pre-existing traditional IRAs (or have moved them into a 401(k))

- You're in a high tax bracket today, but anticipate even higher rates in retirement

But beware, this is not a one-size-fits-all solution. If you need the funds in the short term, or if you don't want to deal with the tax complexities associated with the pro-rata rule, it's best to consult a tax advisor before taking the plunge.

A strategy to consider when preparing for retirement

Against a backdrop of increasing tax pressure and uncertainty about the future of Social Security, every opportunity to optimize your retirement tax situation counts.

The Backdoor IRA is one such powerful strategy that, although technical, can offer lasting benefits to high-income households concerned about their future financial independence.

However, it's important to master the rules, and not to overlook the importance of professional guidance, as one misstep can be costly. But if properly executed, this strategy can make the difference between a tax-free retirement... and a taxed retirement.

IRAs FAQs

An IRA (Individual Retirement Account) allows you to make tax-deferred investments to save money and provide financial security when you retire. There are different types of IRAs, the most common being a traditional one – in which contributions may be tax-deductible – and a Roth IRA, a personal savings plan where contributions are not tax deductible but earnings and withdrawals may be tax-free. When you add money to your IRA, this can be invested in a wide range of financial products, usually a portfolio based on bonds, stocks and mutual funds.

Yes. For conventional IRAs, one can get exposure to Gold by investing in Gold-focused securities, such as ETFs. In the case of a self-directed IRA (SDIRA), which offers the possibility of investing in alternative assets, Gold and precious metals are available. In such cases, the investment is based on holding physical Gold (or any other precious metals like Silver, Platinum or Palladium). When investing in a Gold IRA, you don’t keep the physical metal, but a custodian entity does.

They are different products, both designed to help individuals save for retirement. The 401(k) is sponsored by employers and is built by deducting contributions directly from the paycheck, which are usually matched by the employer. Decisions on investment are very limited. An IRA, meanwhile, is a plan that an individual opens with a financial institution and offers more investment options. Both systems are quite similar in terms of taxation as contributions are either made pre-tax or are tax-deductible. You don’t have to choose one or the other: even if you have a 401(k) plan, you may be able to put extra money aside in an IRA

The US Internal Revenue Service (IRS) doesn’t specifically give any requirements regarding minimum contributions to start and deposit in an IRA (it does, however, for conversions and withdrawals). Still, some brokers may require a minimum amount depending on the funds you would like to invest in. On the other hand, the IRS establishes a maximum amount that an individual can contribute to their IRA each year.

Investment volatility is an inherent risk to any portfolio, including an IRA. The more traditional IRAs – based on a portfolio made of stocks, bonds, or mutual funds – is subject to market fluctuations and can lead to potential losses over time. Having said that, IRAs are long-term investments (even over decades), and markets tend to rise beyond short-term corrections. Still, every investor should consider their risk tolerance and choose a portfolio that suits it. Stocks tend to be more volatile than bonds, and assets available in certain self-directed IRAs, such as precious metals or cryptocurrencies, can face extremely high volatility. Diversifying your IRA investments across asset classes, sectors and geographic regions is one way to protect it against market fluctuations that could threaten its health.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended content

Editors’ Picks

EUR/USD: Winds of change blowing into the Federal Reserve Premium

The EUR/USD pair fell towards 1.1417, its lowest since last March, as the US Dollar (USD) soared following the first Federal Reserve (Fed) monetary policy meeting chaired by Kevin Warsh. EUR/USD got to recover some ground on Friday, finishing the week, however, well below the 1.1500 mark.

Gold: Hawkish Fed leads to third consecutive weekly loss Premium

Gold (XAU/USD) opened with a bullish gap and registered strong gains in the first half of the week, but a hawkish Federal Reserve (Fed) spoiled the party. Mid-tier macroeconomic data releases from the United States (US) and changes in crude Oil prices could impact XAU/USD’s action in the near term, while the technical outlook suggests that the bearish bias remains intact.

British Pound rebounds as holiday-thinned trade slows USD bulls

The Pound Sterling recovers some ground after reaching a three-month low on Friday at 1.3163, sponsored by the Fed’s hawkish tilt, but edges up 0.18% amid thin trading conditions due to a holiday in the US. The GBP/USD trades at 1.3226, yet it is poised to end with weekly losses of 1.25%. Market sentiment remains fragile despite the recovery from the US-Iran deal.

US Dollar: The last mile just got longer Premium

A very auspicious week saw the US Dollar (USD) trade with robust gains, rapidly leaving behind the prior pullback and sending the US Dollar Index (DXY) to levels last traded in mid-May 2025, past the 101.00 barrier on Friday.

Bitcoin: Recovery hopes fade after the Fed spoils the party

Bitcoin (BTC) is set to end the week in the red, trading near the 200-Week Simple Moving Average (SMA) at around $62,300 on Friday. Institutional selling persists, capping BTC’s recovery as spot Exchange Traded Funds (ETFs) point to a sixth consecutive week of outflows.

Tesla (TSLA): Why Elliott Wave supports higher prices toward $774

Tesla (NASDAQ: TSLA) remains one of the most closely followed companies in global markets. While many investors focus on electric vehicle deliveries and short-term earnings, Tesla’s long-term growth story extends far beyond the automotive sector.