GBP/USD Price Annual Forecast: Will 2026 be another bullish year for Pound Sterling?

- GBP/USD has witnessed an eventful journey in 2025, from almost 15-month lows to nearly a four-year high, to finish the year roughly 6.5% higher.

- Divergent Fed-BoE monetary policy expectations, grim UK economic outlook, and political volatility are set to impact the pair’s 2026 price action.

- GBP/USD’s technical setup on the monthly timeframe paints a bullish picture.

Having wrapped up 2025 on a positive note, the Pound Sterling (GBP) eyes another meaningful and upbeat year against the US Dollar (USD) at the start of 2026. The GBP/USD pair is expected to battle a gloomy UK economic outlook and geopolitical risks, while prospects of monetary policy divergence between the Federal Reserve (Fed) and the Bank of England (BoE) could act as a tailwind.

In hindsight, the currency pair’s journey in 2025 was nothing but a dreamy run in the first half of the year, after the initial rough patch. The Pound Sterling bottomed at nearly 15-month lows of 1.2100 against the USD in January, and since then, there has been no looking back, with buyers clinching an almost four-year high at 1.3789 on July 1.

However, the Greenback managed to find its feet in the third quarter, stalling Cable’s advance before losing ground once again in the final three months of 2025. This allowed GBP/USD to regain traction to trade around the 1.3400 round figure by mid-December, adding about 6.5% annually.

GBP/USD Weekly chart for 2025. Source: FXStreet

2025: A fundamental backstory

The latest rebound in the US Dollar in 2024, fuelled by the ‘Trump trade’ optimism after Donald Trump’s victory in the US general elections, extended into the beginning of January 2025, maintaining the bearish pressures on the Pound Sterling.

Increased concerns over the potential impact of US President-elect Trump’s immigration and trade policies revived the haven demand for the Greenback. The USD also started off the year on a strong footing amid expectations of fewer interest rate cuts by the Fed. Subsequently, GBP/USD hit a rock bottom at 1.2100 around mid-January, with its pain exacerbated by the bond market turmoil in Great Britain as investors remained worried about UK assets and the economic outlook.

Over the next few months, the Pound Sterling capitalized on intense bearish sentiment around the USD, as markets sold off US assets amidst Trump’s threats to impose ‘reciprocal tariffs’ globally. At the same time, the US labor market began showing early signs of slack, bringing back the odds of aggressive Fed rate cuts to the table, and weighing negatively on the buck.

On April 2, the so-called ‘Liberation Day’, “US President Donald Trump unveiled a 10% baseline tariff on most goods imported to the US, with much higher duties on products from dozens of countries. Chinese imports to be hit with a 34% tariff, on top of the 20% Trump previously imposed, bringing the total new levy to 54%,” per Reuters. The EU faced a 20% tariff, and Japan was targeted for a 24% rate.

Worries about potential retaliation from the US's major trading partners, including China and the EU, which could ultimately escalate into a severe global trade war, further fuelled the ‘Sell America’ scenario, while the Pound Sterling stood resilient despite reduced appetite for riskier assets.

Mounting economic concerns prompted markets to lift their expectations for Fed rate cuts in 2025. Interest rate futures then priced in about four cuts over the year, compared with the Fed's median forecast of two cuts in the March monetary policy meeting.

Keeping the GBP afloat, markets predicted a limited impact on the UK economy from Trump’s 10% reciprocal tariffs, waiting for the Bank of England (BoE) to stick to fewer rate cuts in the year. The growing expectations of the Fed-BoE monetary policy divergence lent additional support to the pair.

The tide turned against the major in the three months to September as the USD witnessed a buying resurgence amid easing trade tensions. The US reached trade deals with some of its major Asian trading partners and the European Union (EU). This came after the US and China confirmed that they have agreed on a trade framework in the London talks.

However, the downside remained cushioned as the USD continued to face headwinds from renewed US-China tensions, concerns over the Fed’s autonomy and increased calls for rate cuts by the central bank in the balance of the year.

During this time, markets began to expect the Fed to cut rates by a total of 100 basis points (bps), starting later in 2025 and ending early 2026, amid renewed economic and trade worries.

Concerns over the UK fiscal and economic health, combined with the Fed’s shift to a more cautious stance on rates, emerged as a double whammy for the pair. UK Chancellor of the Exchequer Rachel Reeves had plans to raise income tax rates in her November 2025 budget, which was later dropped just days before the Autumn Budget report.

Meanwhile, uncertainty over the impact of Trump’s tariffs on inflation led a majority of Fed policymakers to adopt caution on further rate cuts.

In the final quarter of the year, GBP/USD found strong support at the 1.3000 psychological level as the USD was thrown under the bus once again. The longest-ever US government shutdown, which lasted 43 days, delayed economic data releases, and mounting bets for Fed rate cuts – to alleviate the labor market slowdown – refuelled the USD downside.

That being said, the Artificial Intelligence (AI)-driven rally in global stocks, alongside optimism over a US-China trade deal and dovish Fed outlook, kept risk sentiment in a sweeter spot and the GBP/USD pair above the 1.3300 mark. Broadly, the US-China trade deal included a reduction of fentanyl-related tariffs on imports from China, renewed agricultural purchases, and a pause in Chinese export controls.

GBP/USD: Key catalysts to watch in 2026

Fed and BoE interest rate outlooks

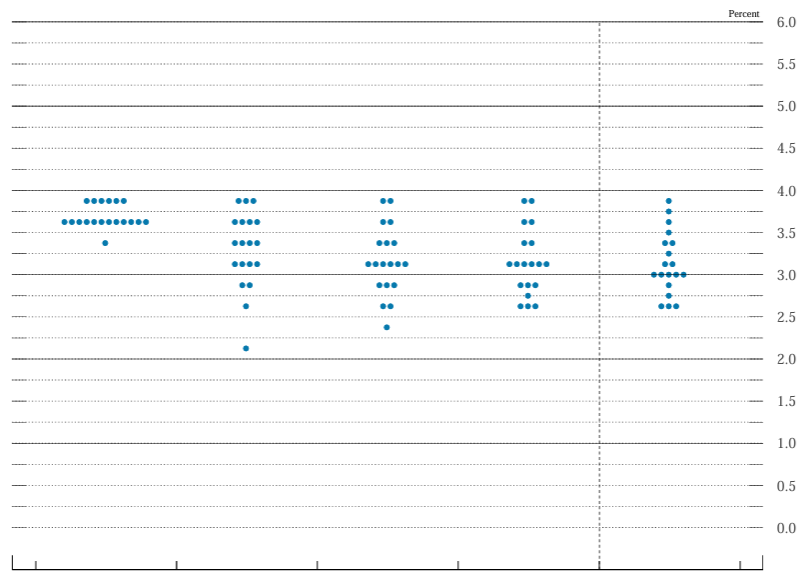

The Fed lowered the fed funds rate by 25 bps for the third consecutive meeting to a target range of 3.5% to 3.75% in December, bringing its key rates to the lowest in nearly three years. Before September, the US central bank extended the pause for five meetings in a row.

Notably, three Federal Open Market Committee (FOMC) members dissented against the latest cut, marking the first such split since 2019. The Fed’s median forecast now anticipates a single quarter-percentage point cut in 2026, with inflation not expected to reach its 2% target until 2028.

Source: Federal Reserve

Fed Chairman Jerome Powell stuck to his cautious tone at the press conference following the December monetary policy meeting, disappointing those positioned for a more hawkish stance.

Markets continued to price in two more rate cuts in 2026, despite the central bank’s cautious cut decision going into the turn of the year.

Traders expect 63 bps of rate cuts by the Fed next year, according to data compiled by LSEG FedWatch.

This could be in part due to their understanding that a potentially more dovish Fed may be seen in a handful of months, with Jerome Powell’s term as the Fed Chairman expiring in May 2026. Further, US President Donald Trump’s picks for the Fed’s top position, including Governor Christopher Waller and White House Economic Adviser Kevin Hassett, continue to endorse lower rates.

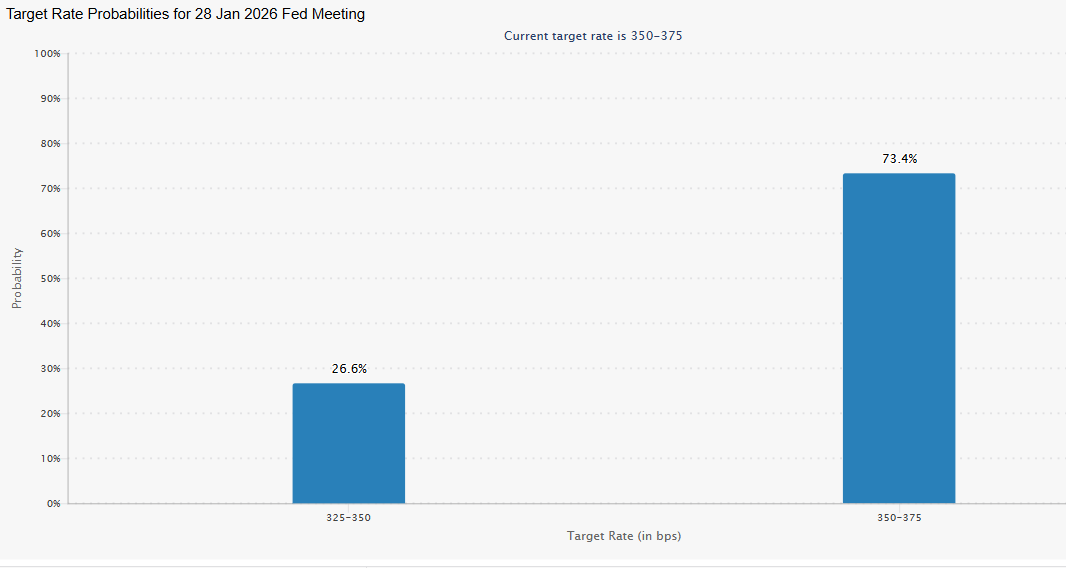

Meanwhile, the odds of a Fed rate cut at the January monetary policy meeting stand at about 25%, according to the CME Group’s FedWatch Tool.

Source: CMEGroup

Across the Atlantic, the BoE cut the benchmark Bank Rate by another 25 bps from 4% to 3.75% after its December monetary policy meeting, dragging borrowing costs to their lowest level since January 2023. The central bank delivered a total of 100 bps of cuts this year after the easing cycle began in August 2024.

BoE Governor Bailey switched to the rate cut camp as a 5-4 vote split came as no surprise. However, his comments that as rates approach this neutral level (estimated between 2-4%), further easing will be a "closer call" leave the money markets now pricing in about one-and-a-half cuts next year.

Bailey further noted that “we still think rates are on a gradual downward path.”

Goldman Sachs revised its call, now expecting the BOE to deliver a 25 bps rate cut each in March, June, and September 2026, versus the prior forecast of cuts in February, April and July.

Meanwhile, Deutsche Bank predicts two BoE rate cuts in 2026, noting, “we stick to our call for two further rate cuts in 2026 - one in March, and another in June, taking Bank Rate to a terminal rate of 3.25% - broadly consistent with our current estimates of neutral.”

US and UK macroeconomic picture

Markets remain sceptical about the US economic prospects, in the face of the data distortions caused by the longest-ever government shutdown.

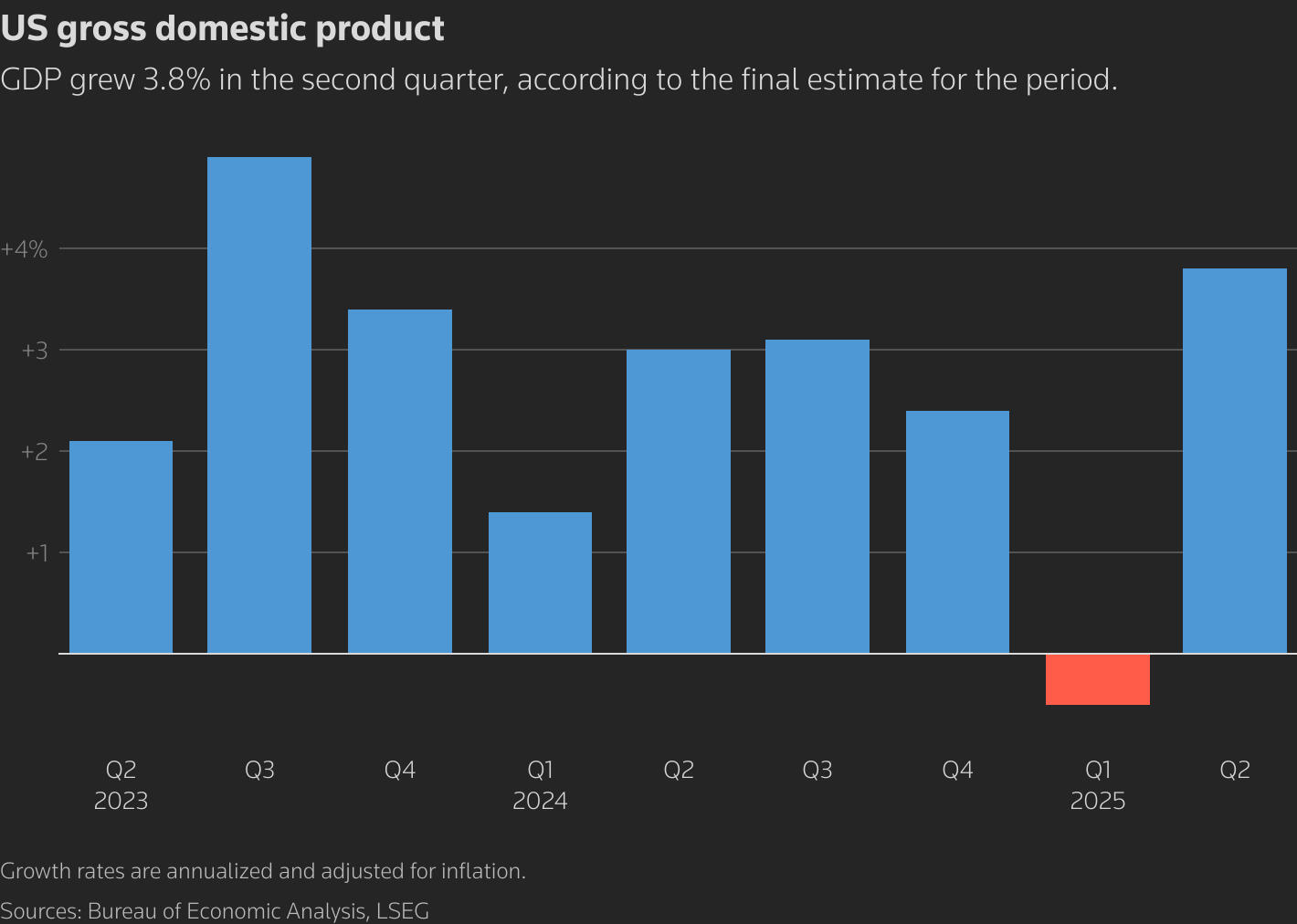

The second-quarter US Gross Domestic Product (GDP) increased at an upwardly revised 3.8% annualized rate, the fastest pace since the third quarter of 2023, according to the Commerce Department's Bureau of Economic Analysis (BEA).

However, the US labor market is worsening. Nonfarm Payrolls rebounded by 64,000 jobs in November after the economy shed a whopping 105,000 jobs in October. The Unemployment Rate rose to more than a four-year high of 4.6% in the same period.

Meanwhile, the US core Consumer Price Index (CPI) rose 2.6% year-on-year (YoY) in November, falling short of the 3% increase forecast by economists.

Despite the unexpected numbers, underlying inflation remains higher. Nonetheless, the potential deepening labor market slack could help it move closer to the Fed’s target of 2%. In such a scenario, calls for more than one rate cut in 2026 by the American central bank could be justified.

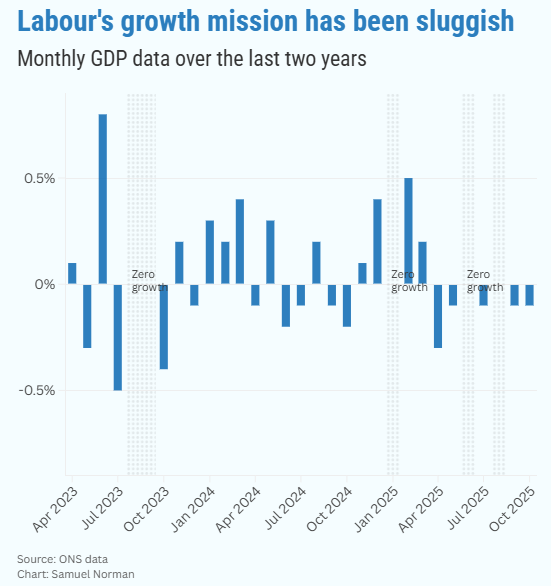

On the UK side of the equation, recent economic data were nothing but disappointing, which kept expectations of further BoE rate cuts alive heading into 2026. To begin with, the UK GDP contracted or flatlined every month from August through October, and the total Trade Deficit widened by £4bn to £6.7bn in the three months to October.

Annual CPI inflation fell to 3.2% in November from 3.6% in October, reporting a bigger drop than markets expected and below the central bank’s forecast of 3.4%. Meanwhile, the ILO Unemployment Rate rose to 5.1% in the three months to October.

While the bank welcomed the drop in inflation, it might note that expectations are still well above its 2% target.

The BoE’s updated staff forecast showed zero growth in Q4 GDP on a quarterly basis, against the previous forecast of +0.3%. Inflation is now expected to revert toward the 2% target more quickly in the near term.

The British central bank estimated that Reeves’ budget, announced in November, could reduce inflation by between 0.4 and 0.5 percentage points for a year from April, mainly due to the axing of green levies from energy bills and the freeze.

Markets believe the Chancellor's increase to her financial buffer in the budget would help reduce uncertainty over the coming year, but it was unclear whether that would strengthen economic activity.

But KPMG UK's Chief Economist Yael Selfin said investment from the private sector and government "could help foster growth over the coming year".

British inflation has been higher than in other major advanced economies, and this could persuade the BoE to reduce rates at least a couple of times in 2026. Lower BoE rates should then pave the way for a rebound in growth over the course of 2026.

UK political volatility

Simmering political unease in the UK could weigh on sentiment surrounding the Pound Sterling. Prime Minister Keir Starmer’s stance looks anything but secure amid increased concerns over immigration and economic growth.

The positions of both Reeves and Starmer have been regularly questioned, and with pressure building, despite the limited optimism following the budget release, volatility in the political scene and gilt markets will likely act as a headwind.

Reports that Labour Together – an influential Labour think tank – has been canvassing members on alternative leadership options prompted renewed speculation about Prime Minister Keir Starmer’s long-term position, per Reuters.

The survey is said to include assessments of Starmer and eight senior Labour figures, stoking speculation that a challenge could emerge in May 2026 if Labour underperforms in the local elections.

GBP/USD 2026 technical outlook: Bullish trend to continue

Source: FXStreet

As we can see on the monthly time frame, GBP/USD’s price action in 2025 has carved out an ascending triangle formation, with the path of least resistance appearing to the upside at the beginning of 2026.

Additionally, the ascending triangle is a bullish chart pattern. The Relative Strength Index (RSI) holds comfortably above the 50 level, suggesting that the price remains exposed to upside risks.

In this scenario, Pound Sterling bulls must clear the horizontal trendline resistance at around 1.3785 to validate the triangle breakout. Acceptance above that hurdle would propel bulls toward the 200-month SMA at 1.4142.

However, the 1.4000 round level could act as a tough nut to crack for bulls at first.

On the flip side, strong support aligns at the rising trendline near 1.3100. A downside break to the ascending triangle pattern will be confirmed if the pair yields a monthly candlestick closing below that level.

The immediate support in the 1.3030-1.2960 confluence zone, if challenged, could trigger a tactical pullback on any retracements. That area is where the 21- and 100-month Simple Moving Averages (SMA) close in.

The next critical cushion is located at 1.2721, the 50-month SMA. A sustained break of this support will pave the way for a fresh downtrend toward the 1.2500 psychological mark. The extension of this bearish trend will likely expose the January 2025 low at 1.2100.

To conclude

Expectations regarding the Fed-BoE monetary policy divergence could overshadow the prospect of political turbulence in the United Kingdom (UK) and a softening trend in the domestic economic outlook, keeping the GBP/USD afloat in the year ahead.

The Fed appears more likely to opt for more than a single rate cut in 2026 than the BoE, as the latter has to battle elevated inflation.

Additionally, the pair will likely draw support from a constructive technical outlook, unless the US labor market conditions improve materially.

Pound Sterling Price This Year

The table below shows the percentage change of British Pound (GBP) against listed major currencies this year. British Pound was the strongest against the Japanese Yen.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -11.63% | -6.45% | -0.08% | -4.16% | -6.35% | -2.71% | -12.40% | |

| EUR | 11.63% | 5.82% | 13.07% | 8.43% | 5.91% | 10.09% | -0.87% | |

| GBP | 6.45% | -5.82% | 6.82% | 2.48% | 0.09% | 4.04% | -6.33% | |

| JPY | 0.08% | -13.07% | -6.82% | -4.06% | -6.25% | -2.58% | -12.27% | |

| CAD | 4.16% | -8.43% | -2.48% | 4.06% | -2.38% | 1.51% | -8.60% | |

| AUD | 6.35% | -5.91% | -0.09% | 6.25% | 2.38% | 3.96% | -6.40% | |

| NZD | 2.71% | -10.09% | -4.04% | 2.58% | -1.51% | -3.96% | -9.96% | |

| CHF | 12.40% | 0.87% | 6.33% | 12.27% | 8.60% | 6.40% | 9.96% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the British Pound from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent GBP (base)/USD (quote).

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data. Its key trading pairs are GBP/USD, also known as ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates. When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP. A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.