The US dollar is alive and well

Since the middle of March, the US Dollar Index (DXY) has been on a steady decline. I wrote about some of the forces behind its weakness in mid-November, which you can find here. Since then, the dollar has declined even further against many of its peers, particularly against the currencies of developed nations. Talks of the dollar’s demise have only intensified the lower the dollar index has fallen. I want to dissect many of the arguments against the dollar and present some flaws within them. I also want to discuss the various aspects of the dollar that many overlook. I strongly believe that the calls for the death of the dollar are unwarranted and due to a lack of understanding of the dollar and its role in the global monetary system. Before we dive into that though, I want to first take a quick look at where the dollar currently stands.

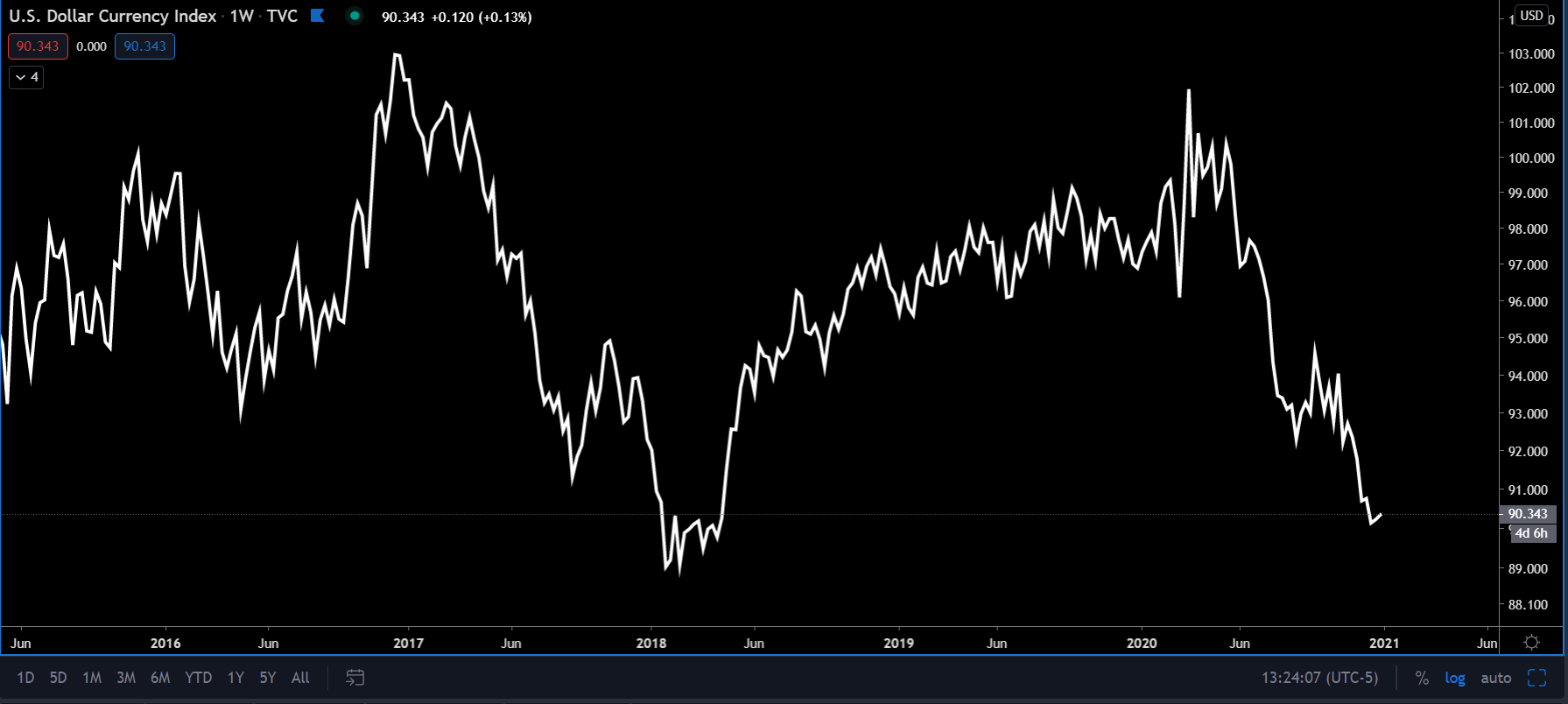

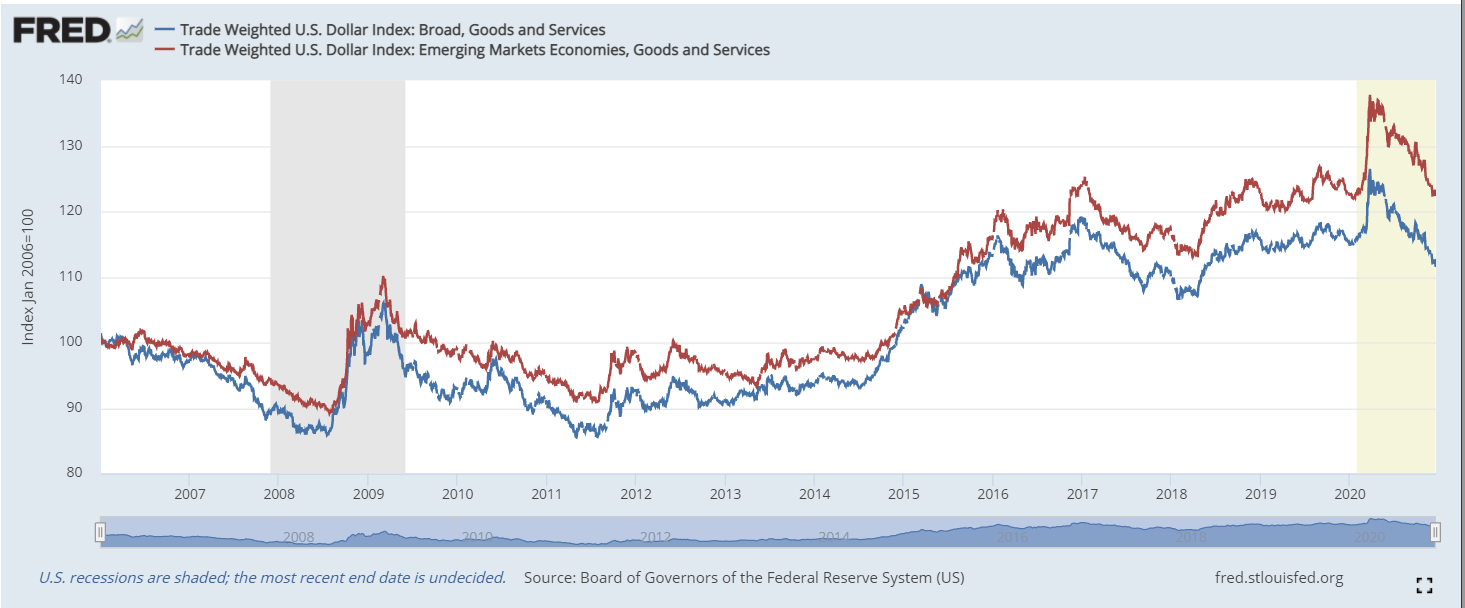

The chart below shows the current state of the DXY. The DXY is heavily weighted in the euro which has performed very well since the March selloff. If you look (2nd chart) at the trade weighted dollar index and the trade weighted dollar index against emerging markets, the dollar has held up much better in those indices than the DXY. I don’t want to get too deep into the different dollar indices since I already did that in my first article on the dollar. Just be aware that the popular DXY can be very misleading because of its over-weighting in the euro. Nevertheless, the dollar’s weakness over the last several months is well-noted regardless of your preferred dollar index.

The dollar continues to plunge as the reflation theme and stimulus talks intensify. Most believe the dollar will not recover from this downward spiral. After-all, the Fed continues to “print” money. Without getting into the argument of whether QE is or isn’t money printing (it’s not), I want to run with QE for a moment. Anytime QE is brought up, the mainstream talks about how the Fed is going to print the dollar to zero. One thing that isn’t being considered though is that every other central bank is also printing. So, let’s say for example the Fed prints a trillion dollars and the European Central Bank (ECB) prints the equivalent amount in euros, assuming all else is equal, in theory the EURUSD exchange rate would be unaffected. Both sides are increasing their money supply an equivalent amount, so neither the USD nor the Euro would see a negative impact relative to one another. Now, the Fed’s balance sheet has expanded at a faster rate than every other central bank the last couple of years. This certainly should be considered when measuring the USD printing that has taken place, which I will do in just a moment. However, first I want to look at a central bank that has in total printed more than any other central bank by far. No, not the Fed, it’s the Bank of Japan (BOJ).

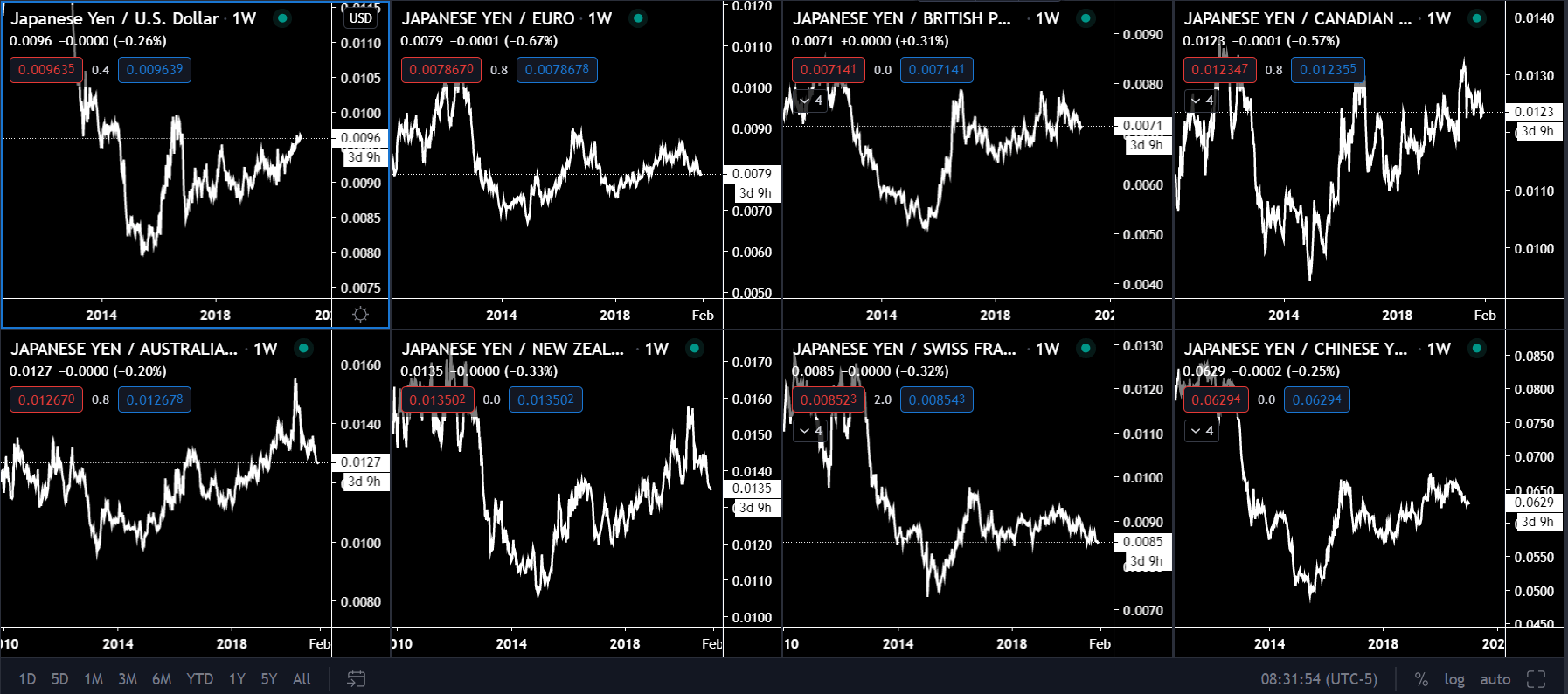

The BOJ has printed close to three quarters of a quadrillion Japanese Yen (roughly 7.5T USD). Yes, you read that correctly, quadrillion. Surely, with that amount of currency printing the Yen should have already hit zero, right? Well, if you look (below), I have a chart of the Yen versus the other seven major currencies and the yuan. The chart shows that the yen is up against all of its counterparts since 2008, except the Swiss franc, which it is slightly down against, and the Chinese yuan which it is flat against. If you consider the more recent lows back in 2015, the yen is up against every major currency, as well as the yuan. The BOJ is years ahead of every central bank in the printing department, and yet, their currency is alive and well. It is still in demand. Everyone loves to overlook Japan when it comes to money printing, which is mind-boggling considering they have significantly more experience with it. The point is, it is clearly possible for a central bank to print inconceivable amounts of currency and still not destroy the demand for its currency.

Currency demand is the biggest element to this puzzle that is being missed. The US dollar (eurodollar) is the Global Reserve Currency (GRC). The US dollar is the largest source of global funding. A reserve currency is the mechanism by which financial entities and different nations with varying systems can communicate with one another, allowing for trade and investment to take place without owning that nation’s local currency. It is the single most vital aspect of the global economy and has been since post-WWII. In other words, there is more demand for the US dollar than there is for any other currency on the planet, bar none! Therefore, the Fed can afford to print more of its dollars than any other central bank in the world. If the BOJ (which doesn’t hold the GRC status) can print more than the US, without destroying their currency, surely the Fed has a long way to go before the dollar is threatened as a reserve currency and its value is compromised relative to other currencies. That is what’s key – relative to other currencies. Most agree that the fiat currency system is coming to an end, but until then, currencies trade relative to one another. Because the dollar has more demand for its currency than any other, it will inevitably rise versus its counterparts overtime.

Dollar bears are screaming right now, “but the world is de-dollarizing! Everyone is moving away from the dollar! It’s dead!” Yes, it is true that there has been more and more global trade taking place in local currencies outside of the dollar. This speaks to the global dollar shortage from which we are suffering. You cannot operate globally without US dollars. So, when nations do not have enough dollars, what do they do? That’s right, they will try to trade in their local currency (or commodities). This has been happening more frequently as of late. However, it is not efficient for nations to start engaging in trade with many different currencies. Let’s say you’re an oil producer in Russia and you reluctantly accept Brazilian real from a buyer in Brazil as a form of payment for your oil. Now you have Brazilian real— but what if no one else is willing to accept Brazilian real as a form of payment? You just sold oil for a currency that no one will accept. You will now have to sell those reals on the open market for another currency (probably dollars). This can get exorbitant. It is not efficient and can be quite costly to start dealing in various currencies. That’s what makes the GRC so important— it allows for smooth operations without worrying if a trading partner will accept your form of payment. Think of it like this: who wants Russian rubles outside of Russia? No one. Who wants Brazilian real outside of Brazil? No one. Who wants Chinese yuan outside of China? No one. Who wants euros outside of the eurozone? No one. Who wants dollars outside of the US? Everyone. The reason being, is that there needs to be depth and liquidity for a currency to have global appeal. No other currency has that to the extent that the dollar does.

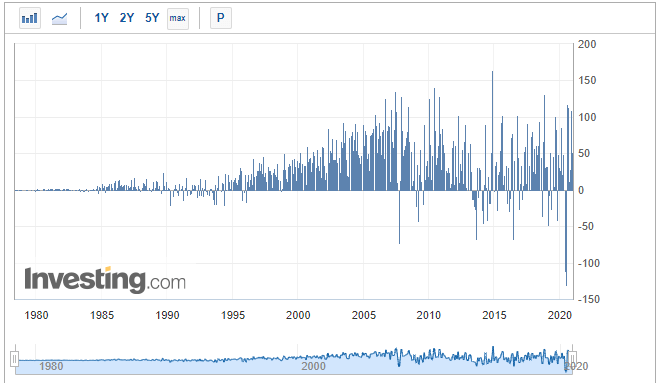

So, the question becomes: are nations using their local currency for trade by choice? The answer is no. They are forced to engage in global trade with local currencies because there are not enough dollars to go around. The mainstream loves to highlight that foreigners have been selling US Treasuries over the last few years. If you look at TIC Data (below), that is indeed that case. TIC is the Treasury International Capital which shows the net foreign buying and selling of US securities. Above zero shows net buying of US securities by foreigners and below zero shows a net selling of US securities by foreigners. You can see from the 1980s to about 2007-08 there was a steady increase in purchases with a few moments of selling in between. When central banks have excess dollars, they purchase US Treasuries and keep them in their reserves. They tend to do this more in periods of dollar weakness. Since 2007-08, you can see that the purchasing of US Treasuries has occurred with less volume over time and the periods of net selling have become more frequent and with heavier volume. This data speaks to the global dollar shortage. Foreigners are essentially forced to sell their Treasuries for dollars, which has become more prevalent over the last 13 years— with the biggest such event happening this past March where foreigners sold 250 billion Treasuries in just a couple of weeks, disrupting the Treasury market. So, not only has the selling of US Treasuries picked up over the past 13 years, the buying has subsided. Recently, the buying has picked up slightly, but not as much as you’d expect considering the DXY is down about 13% since March. The buying spike in July, August, and now November is well short of the high last seen in October 2018 and the DXY was 6% higher during that time than it is now. In such a period of dollar weakness, you would expect more buying of US Treasuries by foreign central banks, but it is not happening because they do not have the dollars to do so. In fact, they have been forced to continually drain their reserves by selling their Treasuries because they need dollars but aren’t getting them through global business operations like they had many years ago.

I always hear the mainstream media mention that China is moving away from the dollar and they present data that China has been net sellers of US Treasures since 2014 as evidence. While this is true, it’s easy to assume that this means China is “de-dollarizing”. However, once you understand the global monetary system is a dollar (eurodollar) one, you can clearly see that China is in fact being “de-dollared” and not “de-dollarizing”. In other words, China has a dollar problem— they don’t have enough dollars to operate and they’re being forced into conducting business in other forms of payment. Let’s not forget, China became a global superpower in a DOLLAR (eurodollar) SYSTEM! China loved dollars until they became scarce, which caused both the GFC and March 2020. If there was a legitimate alternative to the dollar system that China could move onto, then I would be singing a different tune, but there’s not. I will get into that later. For now, I want to talk more about the eurodollar, which I have mentioned a few times already.

The eurodollar market is a cashless, virtual dollar market that is the funding mechanism for the global banking system, and it governs our global monetary system. Eurodollars simply refer to any US dollar that is outside of the US. Prior to the euro currency, euro just meant a currency outside of the domestic economy. For instance, a euroyen are Japanese yen outside of Japan, euroyuan are Chinese yuan outside of China, etc. This is important because neither the Fed nor any other US governing body has any influence or authority over the eurodollar market, despite the fact that these eurodollars are technically dollars. It is an unregulated market that the banking system completely controls. The banks make the rules and create the dollars in whichever manner they see fit. These eurodollars are created through various and often complex balance sheet constructions, which never show up on a transaction sheet or accounting balance sheet, and because of this, it is very difficult (near impossible) to keep track of them (hence the reason it is called “shadow banking”). The BIS (bank for international settlements) estimated that eurdollar debt stood over 12 trillion USD at the end of 2019. It has likely grown since then, but again this is just an estimate. Many of those that are familiar with the eurodollar market believe eurodollar debt is 20-30 trillion or even greater. In other words, there is a massive amount of USD-denominated debt OUTSIDE of the US. Debt creates demand for the currency in which that debt is denominated. So, not including domestic debt, there is potentially tens of trillions in dollar debt (and thus, dollar demand), that exists outside of the United States. When that debt comes due, dollars must be obtained in order to service the debt, which again creates demand for the dollar and drives its value even higher.

The eurodollar system was created around the mid-1950s. It really took off in the 60s and 70s and was firing on all cylinders up until 2007-08. Since the dollar earned its reserve status in 1944 (could be argued prior to that) the US supplied the world with dollars by running a trade deficit with other countries. After WWII, the US comprised about 40% of global GDP, so supplying the world with the dollars that were needed was not an issue. Over the years, the US as a percentage of global GDP has continually declined, with the US now making up less than 20% of global GDP. The US has not been able to supply the dollars needed to the rest of the world for quite some time, and that’s when the bank-centered, eurodollar system took over. As mentioned before, global banks exchange financial liabilities and assets, creating eurodollars. Collateral is the key component to this— actually quality collateral is key. Collateral is used by banks to secure funding in eurodollars from other banks. At some point in the early 2000s, banks lost control and began using risky collateral to secure funding. The growing amount of risky collateral on banks’ balance sheets was eventually recognized, which caused lenders to seize funding to other banks if they did not present quality collateral (typically on-the-run Treasury Bills, as they are the most risk free and liquid). So, banks whose balance sheets were filled with risky, illiquid collateral such as low grade mortgage back securities were unable to obtain funding. This is what led to the collapse of Lehman and Bear Sterns (yes, it had little to nothing to do with subprime mortgages). Risky collateral is no longer accepted by funding banks the way it used to be and nothing has replaced that collateral since, which is why there has been a shortage of eurodollars. Since 2007-08, there has been a lack of QUALITY collateral in the system (I can hear Raoul Pal’s voice referencing bitcoin, “pristine collateral”). Combine the lack of quality collateral with poor financial conditions, you have banks hoarding any T-bills and cash they can get their hands on, refusing to lend. You cannot blame them, no one wants to end up like Lehman. The point here is that since the US is no longer large enough to supply the world with dollars via trade and the eurodollar system is not operating at the appropriate capacity to support global growth, we are left with a global dollar shortage. So, what can be done to obtain dollars when there’s a shortage?

It has been argued that foreigners who need dollars can just sell their USD-denominated assets (which often means US Treasuries because they’re the most liquid) to obtain the dollars they need. We saw this play out in March, as risk assets, even gold, bitcoin, and treasuries were sold in order to obtain dollars, which caused the DXY to rally about 9% in less than two weeks. But, there are a few problems with this route. First, many EM (emerging markets) nations own little to no USD-denominated assets. That’s a problem because EM nations often borrow in dollars but own assets denominated in their local currency. They would then be forced to sell their assets for their local currency, then use that currency to buy dollars in the open market. This is a very inefficient and costly route. During a crisis like the one in March, when the dollar is spiking higher, other currencies are falling against it, which would make it even more difficult for EM’s to convert their currency into dollars as a cost-efficient price. The result would likely be a default on their USD-denominated debt.

Second, since we’re in a global dollar shortage, selling your USD-denominated assets for dollars is just a temporary fix, it does not solve the problem. So, what would happen if a nation had to sell all their USD assets to get the dollars that they needed in order to service their debt and operate globally? Once all those dollars are used, what would they do? They would be out of dollars and in a worse position than they were in prior to selling their USD assets. Now, this might sound extreme, but as we head closer to the end game of the fiat currency system, I expect extreme events to take place.

Third, as Brent Johnson has pointed out, there are likely political ramifications for selling your USD assets to obtain dollars. Let’s say Japan is in a serious bind and needs to sell $1T worth of US Treasuries. That type of selling in a short time span would certainly disrupt the US Treasury market. In March, the Treasury market became illiquid for a short time period as foreigners sold 250B worth of US Treasuries for dollars. It only took a few hundred billion to disrupt the Treasury market. I can’t imagine the disruption it would cause if a nation had to sell more than a few hundred billion. The US would be very unlikely to sit on the sideline and allow this to happen. Japan could lose one of its largest trading partners and/or even be kicked out of the global dollar payment system. Each USD transaction that takes place globally goes through the dollar payment system, even if the US is not involved in the actual transaction. Not having dollars and/or not being able to trade in dollars would crash Japan’s (or another nation’s) economy. This would in turn have negative consequences on the global economy.

For foreigners who cannot obtain dollars to pay off their debts, defaulting is their alternative. What if the entire world decided to default on their USD-denominated debt? Well, one person’s liability is another person’s asset. So, when you default, you are destroying someone else’s asset. You are destroying credit. In a situation of a large-scale default of USD-denominated debt, supply is destroyed faster than demand. This creates a scenario that is very bullish for the dollar. So, even if the entire world all agreed to drop the dollar as the reserve currency today, there are still tens of trillions of USD-denominated debt that must be serviced. So, whether that debt is paid or defaulted on, both scenarios create a very bullish environment for the dollar to have at least one last super spike before its demise. I am not denying the end of the dollar is coming, I’m simply saying that the other currencies will fall first due to their lack of global demand.

There is another alternative when foreigners need dollars: central bank swap lines. A swap line is an agreement between two central banks to swap each other’s currency. The currencies are often exchanged overnight or for a very short-time frame (less than a year), and then they are swapped back at the predetermined date. It is like a collateralized loan. A foreign central bank uses its currency as collateral to obtain dollars which they have to pay back to the Fed with interest. For example, let’s say the ECB needs 1 Trillion USD. The Fed would print 1T USD and give it to the ECB in exchange for 1T euros. Now, assuming all else is equal, the dollar would not depreciate against the euro, despite the Fed printing 1T USD. Where do you think the ECB is getting 1T euro’s from? They also must print them. Now, many believe the Fed can just print as many trillions of dollars as necessary to bail out the entire world. There are a couple of issues with this though. First, as Jeff Snider pointed out, these overseas swap lines are not as overseas as we think. In other words, the purpose of the swap lines is to get dollars outside of the US for those who need them. But often times what happens is these dollars find their way into the hands of offshore US banks – US banks located outside of the US. They then take those dollars and send them back to their domestic (US) locations. So, these dollars never find those offshore non-US banks like originally intended. Second, and more importantly, swap lines do not fix the dollar shortage problem; they are just another temporary fix which eventually causes bigger issues. When a central bank swaps their currency for dollars, they don’t then turn around and hand those dollars to their local banks, corporations, and other entities that need them. What they do is they loan out these dollars to their local banks, corporations, and other entities that need them. By doing this, they are creating more USD-denominated debt and making the problem greater. Each time this happens, it reinforces the eurodollar market as the global monetary system, because it further indebts the world in dollars.

The problem with a debt-based monetary system (which we have) is that debt needs to continue to grow in order for the system to grow, but by doing so you further indebt the world and in this case, in dollars since we live in a dollar system. The more USD-denominated debt is issued, the more demand for dollars there becomes. But, even if no more USD-denominated debt is issued, a bullish environment for the dollar can still occur. To reiterate, there is currently tens of trillions in USD-denominated debt out there. If dollar debt is no longer being extended, that means there are less dollars in circulation to service the current debt, which means demand for dollars is now chasing less supply and the result would be a higher dollar. But, it wasn't that long ago that USD-denominated debt was extended by the Fed via swap lines, we just have to go back to the post March selloff.

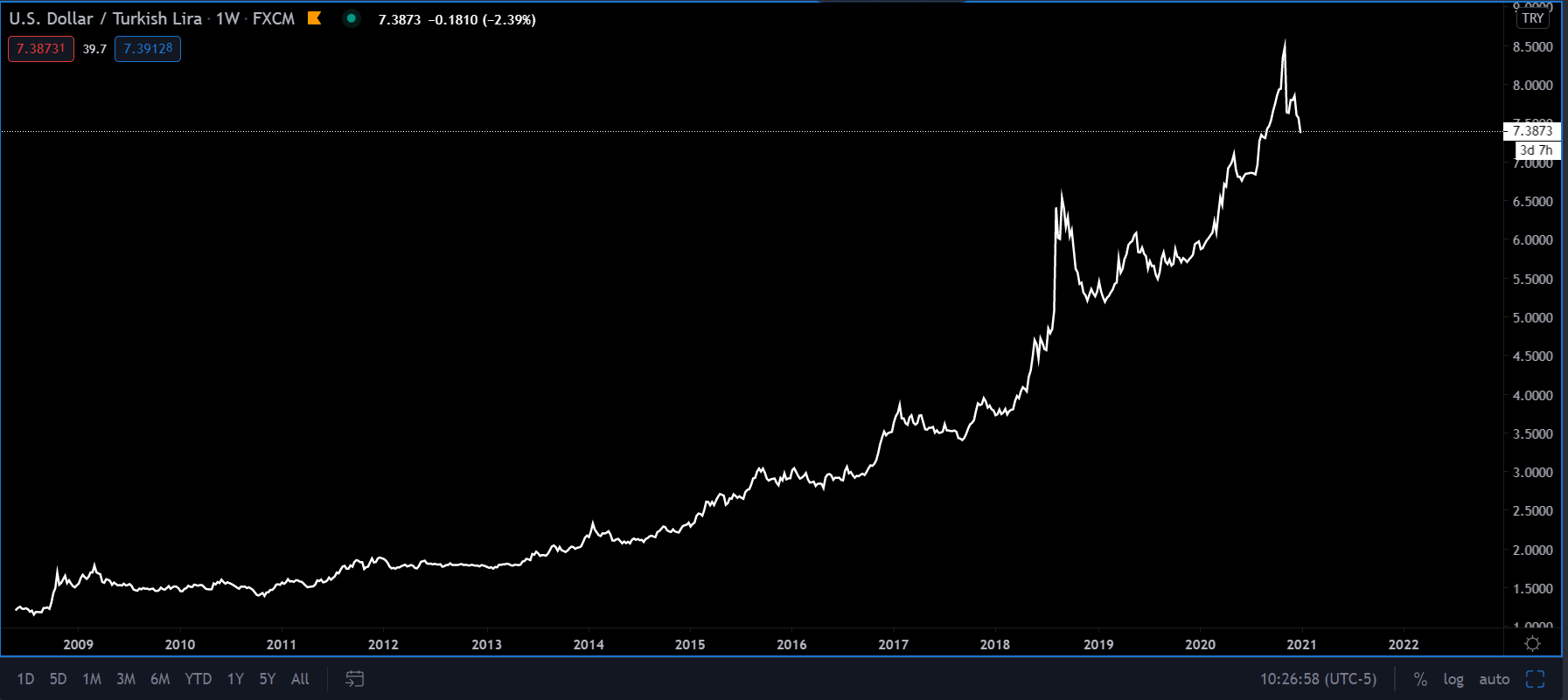

Swap lines are an advantage for the US as the GRC. These swap lines can be politicized as a weapon. Let’s take March for example: as the dollar funding squeeze was playing out, the Fed opened their swap lines to foreign central banks who needed them. However, they did not open their swap lines to everyone. Those who are not allies of the US, like China, Russia, and Turkey did not receive a swap line; therefore, they did not receive much-needed dollars from the Fed. Turkey was already in a tough spot and short on dollars prior to March. Once the dollar funding squeeze ensued, they were desperate for dollars, but the Fed never opened their swap lines to them, despite negotiations that took place for Turkey to try and secure USD funding. It is speculated that Turkey’s relations with Russia as well as their unwillingness to meet certain political concessions played a role in them not receiving a swap line. If we look (below) at a chart of the dollar versus the Turkish lira, we can see that since March the dollar rallied over 40% against the lira. It has recently come down, but it is still up over 20% against the lira. This is despite all the dollar weakness that we have witnessed since then. This is a clear example of what can happen to a foreign nation’s currency that is experiencing a dollar shortage and cannot obtain the dollars they need.

Over the years, the US has been the preferred nation for investment by foreigners as they have had the highest interest rates among the developed nations. Now that interest rates are near, at, or below zero across the developed world, the interest rate spreads aren’t creating as many opportunities. I recently heard that this would result in currencies once again being traded based on balance of trade measure The thought is that this will be a negative for the US because the US has been running deep trade deficits for many decades. It makes sense, because a nation that runs a trade surplus will be more stable and fit for investment than one that consistently runs deficits. However, the mistake here is not taking the dollar’s GRC status into consideration. Going back to the demand for currency concept, no one has confidence in any other currency the way they do the dollar, period. Is that confidnece fading? Sure, but so is the confidence of all fiat currencies. The dollar is the best looking in a group of ugly people. The euro has been around for 20 years, so you could argue it’s still an experiment, an experiment which many believe will fail. The yuan is not a free-floating currency, nor is China transparent about any of the activity that goes on within their borders. Do you think people will suddenly start using an experimental currency or a shady, manipulated one over the dollar which has been king for about 75 years and is accepted everywhere? I don’t even need to answer this one.

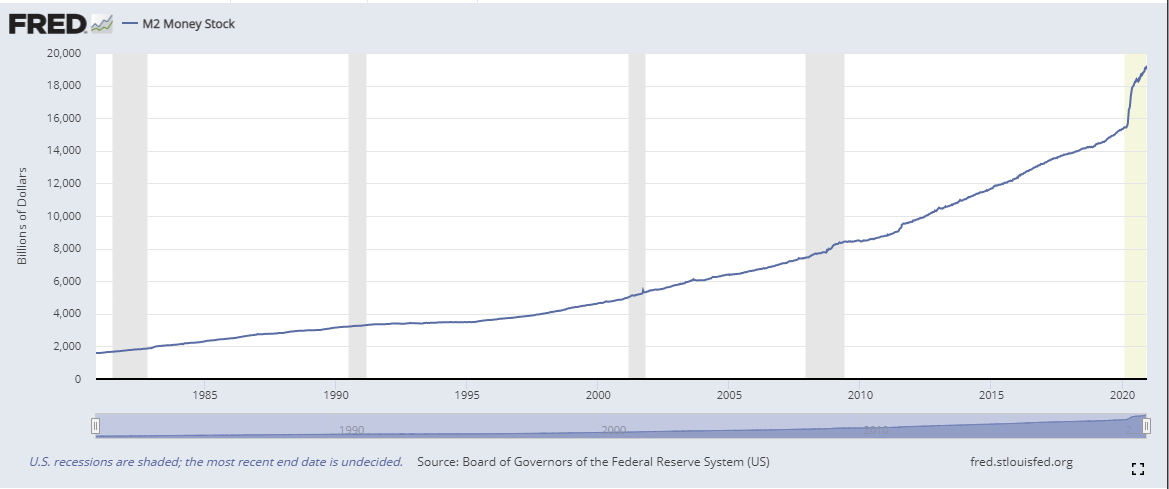

I want to come back one last time to how much money the Fed has printed because I have also talked about the eurodollar system since the last time it was mentioned. According to the M2 money supply which you can see below, the amount of new dollars that have been created in 2020 is unprecedented. The M2 has absolutely taken off since March. This amount of money supply growth with more on the horizon will surely dismantle the dollar. At least that’s what many believe. The expansion of the money supply is a very common argument that is frequently used to support the narrative that the dollar is dead. But there is a massive problem with the M2 money supply. First, let’s define what the money supply is: “M1, is restricted to the most liquid forms of money; it consists of currency in the hands of the public; travelers checks; demand deposits, and other deposits against which checks can be written. M2 includes M1, plus savings accounts, time deposits of under $100,000, and balances in retail money market mutual funds.” This definition comes directly from the Fed. Now, the problem with this is that there are many other forms of money that are not included in the money supply, for example, the eurodollars created by global banks. So, money created in the eurodollar system which is not included in the money supply could find its way into, say, a demand deposit at a bank, expanding the money supply. Do you see the issue? This money was already in circulation and should have been accounted for, but it was not. Now, it finds its way into one of the measures of the money supply, expanding its supply, making it look as if brand new money was created when it was not. This makes the M2 money supply metric extremely misleading.

As we’ve already discussed, the eurodollar market is enormous. There are more dollars in the eurodollar market than in the US domestic economy, yet they are not included in the money supply. Jeff Snider pointed out how monetary authorities do not know how to define money. I mean, Alan Greenspan (former chair of the Fed), admitted this much back in 2000, stating: “the problem is that we cannot extract from our statistical database what is true money conceptually, either in the transactions mode or the store-of-value mode. One of the reasons, obviously, is that the proliferation of products has been so extraordinary that the true underlying mix of money in our money and near money data is continuously changing. As a consequence, while of necessity it must be the case at the end of the day that inflation has to be a monetary phenomenon, a decision to base policy on measures of money presupposes that we can locate money. And that has become an increasingly dubious proposition.” In other words, the Fed has no idea how to define money because the eurodollar system has created so many products (different ways to create eurodollars) that they have no way of tracking or even knowing what “money” is anymore. Nothing has changed since then, meaning monetary authorities still have not figured out how to define money because they do not have a clue how to track the largest dollar market in the world: the eurodollar market. Yet, we are supposed to rely on their measure of the money supply? That is comical. It essentially makes the money supply and thus money velocity (which is based on this outdated money supply metric) completely useless. So, when you argue the dollar is dead because the large expansion of the “money” supply, just know you are using a flawed, outdated metric.

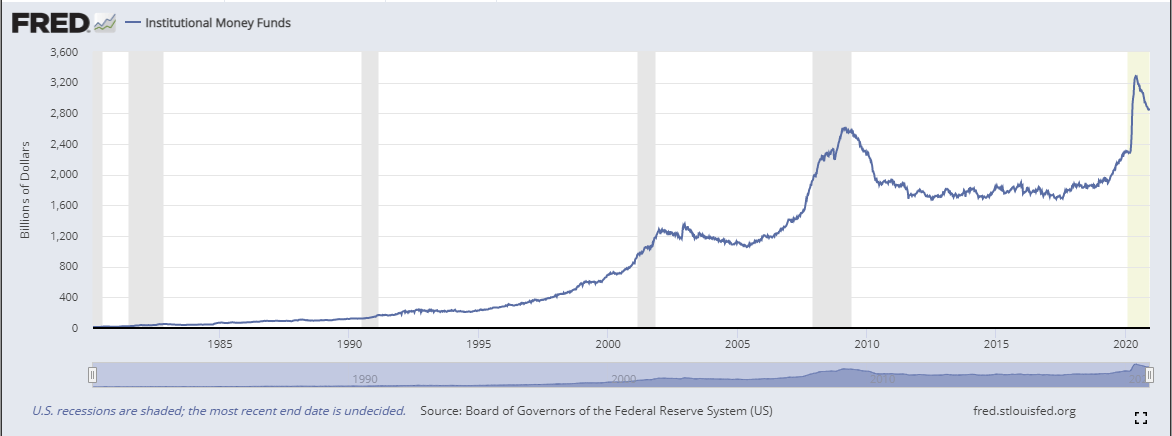

At this point, you may be asking yourself, if all of this is true, why has the dollar been falling? We can speculate many reasons as to why, but I will keep it simple. Cash is not in demand at this current moment. Numerous payments since March have been deferred, from rent, mortgages, loans, inventory purchases, etc. If you have less payments to make, well, then you have less of a need for cash. Also, since March, many loans that were lent have turned into grants, decreasing the need for cash as people no longer have the responsibility to service that debt. If you look (below) at the chart for Institutional Money Funds, you can see that since May it has been on the decline. This means institutional investors are holding less cash and cash equivalent securities. This is significant because investors are getting out of cash and getting into equities. That is why equities continue to rally and the dollar continues to fall: investors are selling dollars and buying equities. Eventually, there will not be enough dollars to continue to push equities higher and that’s when we will see the stock market rollover.

Yes, the fiat currency system is coming to an end, but it won’t happen overnight. Until that day comes, the dollar remains king among the fiat currencies and king among various forms of payment. Yes, there are other forms of payment like gold and bitcoin (among others) that many have been shifting their attention towards. But, the dollar is still the reserve currency, it still makes up almost 50% of all global trade, 80% of global transactions occur in USD, and 40% of all global debt is denominated in USD. A new global monetary system is likely on its way in the coming years and is expected to be in some form of a digital asset, but until that day comes there is NO alternative system. Because of this, the dollar will never die until the system dies. When that day of reckoning comes, which currency do you think will be the last standing? The ones with little to no global demand, or the one with the most global demand? So, continue to expect frequent dollar spikes when USD funding runs short, similar to what we saw in March. As the system starts to collapse, these dollar spikes could become bigger and sharper (yes, the dollar milkshake theory).

I used to be a dollar bear, which I will become again once the dollar spikes higher and the system starts to really breakdown because a strong dollar is detrimental to the global economy. Everyone thinks because the dollar is moving lower that means the dollar and the US are unraveling, but a lower dollar is good for the global economy, and thus good for the largest economy in the world: the US. A cheaper dollar allows for cheaper global trade to occur and it allows dollar debt to be serviced at a much lower cost. A strong dollar makes trade more costly and servicing debt more difficult. Thus, problems occur when the dollar is strong, not weak. When the dollar starts pushing sharply higher as it did in March, that’s when you will know there are systemic issues. That’s when I will turn into a dollar bear because the system cannot handle a strong dollar. A strong dollar will force action by monetary and fiscal authorities to weaken it. I used to be a dollar bear because I used to focus my analysis on the supply side of the dollar. Once I took a deep dive into the demand side, I realized that the demand for the dollar heavily outweighs the supply. From the eurodollar market, to swap lines, to the dollar as the GRC, to global demand, to USD-denominated debt— the demand for the dollar is unmeasurable because of its vastness. Of course, time will tell, but considering the many systemic and structural issues with the global monetary system, the potential for a crisis is high, and each time there is a crisis, the dollar moves higher.

Author

Ryan Miller

Ryan Miller Trading Economics

Ryan Miller received a Bachelors Degree in History from William Paterson University. Through his studies of U.S. history, he developed an interest in the implications the financial markets have on the economy.