Premium Value of an Option

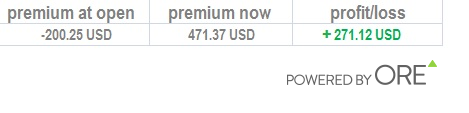

Buying an option

In the example below, the option holder has paid 200.25 USD to buy an option and now it is worth 471.37 USD, hence the profit is 271.12 USD.

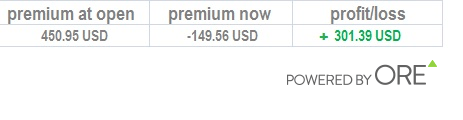

Selling an option

In the example below, the option writer (seller) received 450.95 USD when he sold an option and now it is worth 149.56 USD, therefore he can buy it back for less and his profit is 301.39 USD.

Premium value is comprised of two parts: Intrinsic value and time value. These values change as the underlying market changes.

Premium = Intrinsic Value + Time Value.

Intrinsic Value

Example

Let’s say you buy a EUR/USD Call with a strike of 1.1200 and an amount of 100,000 EUR, as per the option trade details in this image:

If the underlying market is trading at 1.1300, your strike rate (to buy) is 100 pips better than the market, hence your trade is in-the-money (ITM). We calculated this by subtracting the market rate (1.1300) from the strike rate (1.1300) giving us 0.0100 or 100 pips. In fact, on expiry the spot is trading above 1.1200 (the Call with the strike 1.1200), the Call option has intrinsic value.

Intrinsic value = Amount x Difference between market rate and strike rate

= 100,000 x (1.1300 – 1.1200)

= 100,000 x 0.0100

= $1,000.

Therefore, the Call option’s premium = $1000 + Time Value.

Time value

Time value, also known as extrinsic value, is the portion of the premium left after deducting the intrinsic value and is determined by external factors: Time Value = Premium – Intrinsic Value.

Premium can increase or decrease depending on time value and the two main external factors are time until expiry and implied volatility.

Options with a longer expiry are more expensive since you are buying more time for the market to move in your favour. The opposite is also true, options with a closer expiry cost less. When holding an option, the expiry date moves closer for each day passing. The time value portion of the premium declines reflecting this. The process of time value declining each day is known as time decay. Values at expiry have no time value, hence they are intrinsic value only.

Net Present Value (NPV)

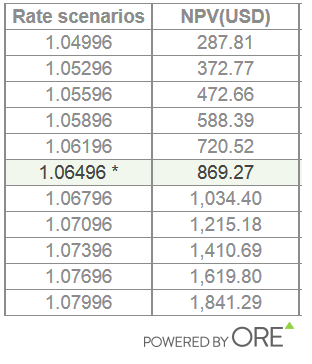

If you are long (by buying) an option, then the NPV value will be positive and this is the amount you will receive when you sell your option back. The example below is a snap-shot of the optionsReasy sensitivity table for a long Call option. The NPV column indicates how the option’s value increases as the underlying market rises.

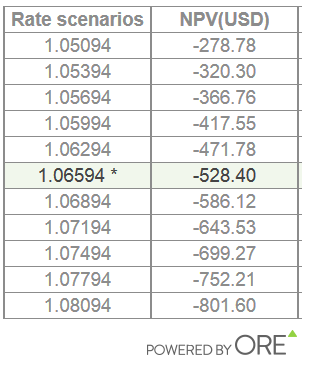

If you are short (by selling) an option, then the NPV value will be negative and this is the amount you will pay to buy back the option. The example below is a snap-shot of the optionsReasy sensitivity table for a short Call position. The NPV column indicates that the cost to the seller increases as the underlying market rises.

Volatility

The marketplace’s consensus on future volatility affects an option’s premium (time value portion). This is known as implied volatility (IV). If the market is expecting more volatility, you will pay more for the option. If there is increasing volatility, it is more likely the market will move in your favour.

Tips:

- If the implied volatility increases after an option trade has been purchased, this is good for the buyer and bad for a seller. Buyers like increasing volatility!

- At any time, your option’s premium will be at least the intrinsic value. At expiry, time value = 0 and the premium = intrinsic value.

Author

Davina Becker is a Product Specialist at ORE with over 10 years of experience in the financial markets.