Discover financial services: Uncertainty ahead

Discover Financial Services provides digital banking and payment services, mainly in the United States. Its digital banking segment is quite regular, providing loans and credit cards to individuals. On the other hand, the payment services segment comprises ATMs, funds transfers, and settlement services, among other things. The company suffered a disastrous 2020 but still managed to stay profitable and seems to be recovering well, but is shrouded in uncertainty ahead.

When it rains, it pours

Discover was doing quite well before the pandemic, with revenues rising consistently. In FY17, the company reported revenues of around $9.9 billion, and they had gone up to about $11.4 billion by FY19. However, the company’s performance was primarily driven by the rise in revenues, as the net margin did not increase during the time (it fell slightly). As such, COVID-19 was a particularly devastating time for the company.

The vast majority of the company’s revenues come about due to its credit card business. In fact, 76% of the company’s revenue in FY19 was due to its credit cards. Credit card revenues fell sharply during the pandemic, as not only did people stop traveling (which accounted for a lot of the revenue), but they also stopped being extravagant with their finances. Americans, in general, took on less debt during the pandemic. Companies like Discover suffered the worst as a result.

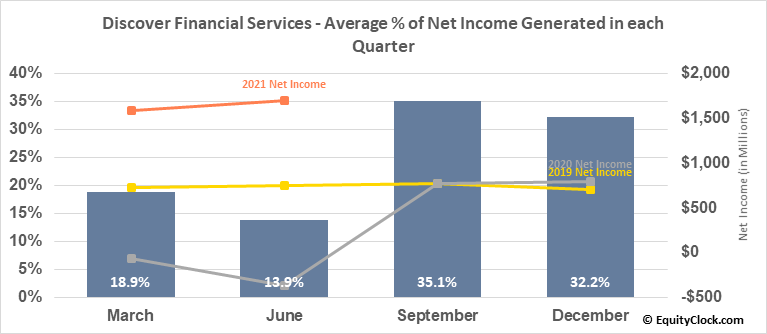

The company tends to generate most of its income in the final two quarters of the year, which means that FY21 could be the most profitable year for the company yet. Source: EquityClock

Fighting back

Q2 FY20 was a particularly devastating quarter for the company, as large credit losses meant that the company reported a $1.2 per share loss. However, the company announced in an earnings call at the end of Q1 that it had plans to cut costs by $400 million in 2020, and it is a strategy that has seemed to work.

Q2 FY20 was the last quarter in which the company reported a loss. While the turnaround can be largely attributed to the recovery of the economy in general, Discover has come through on its promises to reduce costs and streamline its operations.

The company’s net margin was 28.1% in the final quarter of FY20, and business has been booming in FY21 so far. While Americans were initially wary of the financial burden caused by COVID-19, the sentiment has now swung in the opposite direction. Over 40% of Americans have more credit card debt now than they did at the beginning of the pandemic.

While many of these debts are due to financial decisions during the pandemic, a lot of this is simply consumer debt, with people wanting to buy new things in the wake of rising asset prices.

Discovering value

Trying to value Discover is quite difficult right now. The company has performed exceptionally well in FY21, and the earnings per share have crossed $10 by the end of the second quarter. Just to put this into perspective, the company’s EPS for the entirety of FY19 was $9.08.

However, we are unsure if the company can sustain such a performance. For one, the outlook for the economy is not as great as it was at the beginning of FY21. With inflation on the rise, it is possible that the FED could cut interest rates. While it may not happen in 2021, it is inevitable at some point if inflation rates continue to stay high. That would mean people taking on less credit card debt and may even lead to higher defaults.

Still, while the long-term outlook for Discover is uncertain, we cannot argue that the company seems very enticing in the short term. Consensus estimates place the company’s earnings at $16.8 for FY21. The P/E ratio, currently at 8.15, is expected to fall to 7.70 by the end of the year. For FY22, the earnings are expected to fall to $12.5 per share, with the P/E ratio at 10.3.

This makes it challenging to recommend Discover as a long-term investment right now. Although it may be possible for you to time your entry and exit perfectly, we strongly advise against it. Many an investor has thought themselves to be smarter than the market and realized how wrong they were. Although the company has cut costs significantly during the pandemic, it is still massively exposed to its credit card business. As such, considerable deviations in the company’s performance are to be expected in the years ahead.

Author

Baruch Silvermann

The Smart Investor

Baruch Silvermann is a personal finance expert, investor for more than 15 years, digital marketer and founder of The Smart Investor.