![]() Carl R. Tannenbaum

Carl R. Tannenbaum

Northern Trust

Economists are often accused of looking at social problems through a clinical, data-driven lens. But we do have feelings.

Upon arriving in Stockholm for client visits two weeks ago, I ventured out for a walk to acclimatize. Outside the main train station was a large tent. Inside the tent were dozens of refugees; I presumed that many were Syrians. They were being fed and receiving support to find lodging. The faces reflected both the ordeal of traveling 3,000 miles across numerous countries and a faint hope that their new surroundings would become home.

I was especially moved by the presence of children, the innocents in all of this. It was difficult, at that moment, to consider Europe’s migration crisis in the abstract. My heart certainly hoped that those young people would find a brighter future.

Since then, my head has fallen into line with my heart. The fortunes of Europe’s new arrivals may become very closely aligned with the fortunes of Europe itself. Viewed from an economic standpoint, these accidental tourists may become the answer to the Continent’s prayers.

Nearly 1 million people have arrived at Europe’s borders this year after fleeing their homes in the Middle East. It’s the largest mass migration in decades and has tested the processing capacity of host countries. The situation has cast a dark cloud over relations among eurozone members, who have struggled to craft a comprehensive solution to the crisis. But there may be a silver lining to the situation.

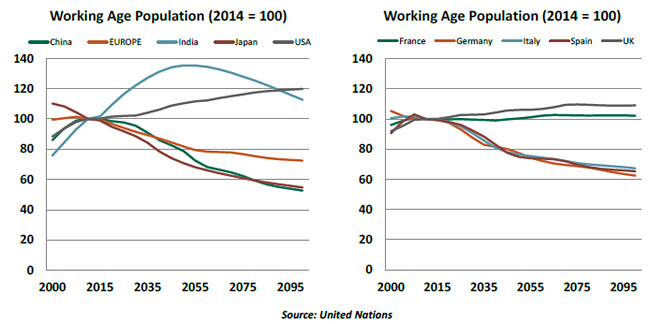

The aging of Europe’s postwar generation has placed the working-age population on a downward trajectory.

Trends in the labor force are critical to potential economic growth. Stasis or decline in a population raises the risk of stagnation, which in turn raises the risk that investors may look on the market less favorably. At the extreme, limited economic growth can challenge the ability of a country to service its debt.

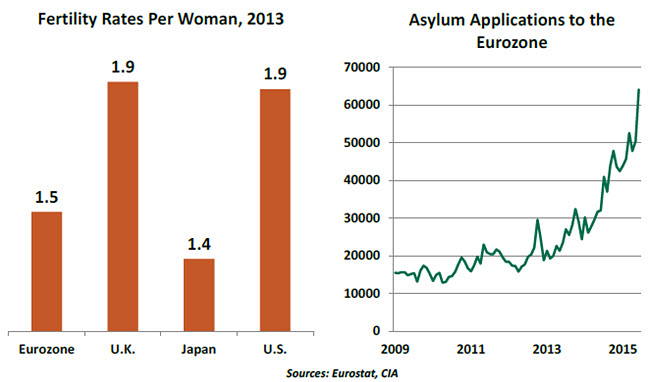

According to Eurostat, 54% of asylum seekers entering the European Union (EU) in 2014 were between the ages of 18 and 34 (prime working ages). A further 20% were between 35 and 64, and less than 1% were aged 65 and over. Under-17-year-olds made up the remainder of the dataset (25%), which will provide a boost to future working-age populations as they mature.  Of those coming to the EU from outside the bloc, many have a decent education. In fact, the level of first- and second-stage tertiary educational attainment among this group is not far off that of EU-born nationals (30.6% versus 35.7%, respectively). Therefore, on average, non-EU migrants can be seen as highly employable once language barriers are overcome.

Of those coming to the EU from outside the bloc, many have a decent education. In fact, the level of first- and second-stage tertiary educational attainment among this group is not far off that of EU-born nationals (30.6% versus 35.7%, respectively). Therefore, on average, non-EU migrants can be seen as highly employable once language barriers are overcome.

Those arriving on Europe’s doorstep therefore have the potential to slow the Continent’s demographic deterioration. There are only two ways to sustain population, and immigration is clearly the more fast-acting of the two.

Of course, immigration is more than just a numbers game. Assimilation is never perfectly smooth and sometimes takes a couple of generations. But there are many myths about immigration that data simply do not support. Among them:

- Immigrants take jobs from natives and depress their wages. There is no systematic evidence of this; often, new arrivals do work that natives would avoid. And if new entrants assume jobs from retirees over time, this should not be a concern.

In some skilled professions, European countries are already facing shortages that migrants can help with. Sweden, for example, needs more dentists; among the new arrivals are a number who are trained in dentistry. To ply their trades, however, they’ll need to satisfy licensing requirements in their new countries, which can act as a frustrating restraint. - Immigrants are a drain on social services. Aid will certainly be needed initially, but providing some financial support may be beneficial to economic growth.

Germany has allocated $6.7 billion to provide support to the refugees in their country, and France has pledged $4.5 billion. While these are not insignificant nominal amounts, they are certainly manageable.

In fact, it may be just the sort of growth-promoting fiscal policy that Europe sorely needs. A lack of demand is one of the root causes of sub-par growth in the eurozone, and there have been calls for the Germans, in particular, to open their coffers a bit. Money spent to integrate immigrants doesn’t go down a big drain; it rebounds through the economy as it is spent. - Immigrants don’t pay taxes. Anyone who purchases things pays sales taxes, and anyone who rents pays property taxes indirectly. At some point, the new arrivals will begin paying into national retirement schemes, where their contributions will be very much welcomed as a means to pay pension obligations.

The economic perspective does have its limitations. History suggests that incorporating significant new populations takes time, and success depends heavily on program design and popular support. Neither is firmly in place at the moment, as the waves have arrived much more rapidly than anticipated. But cultures that find a way to make immigration work remain vital, literally and economically.

Emerging Markets Face Headwinds from Capital Outflows

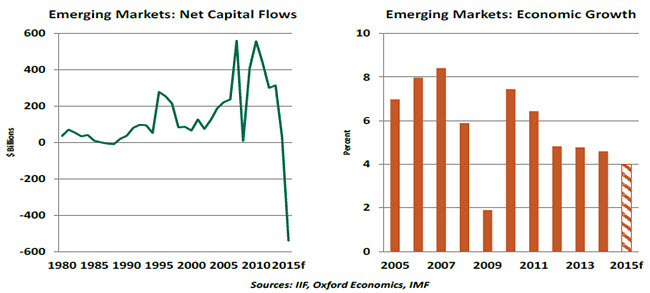

People haven’t been the only resource flowing out of emerging markets (EMs) in recent months. Capital has been making its way out as well.

Capital flowed freely to EMs as the Federal Reserve and other central banks in advanced economies implemented unconventional monetary policies after the Global Financial Crisis. The surge in capital inflows helped to lift growth in the developing world.

But the tide has turned. The Institute of International Finance (IIF) estimates that, on net, more money will leave EMs than enter them in 2015, a first since 1988.

The outlook for growth in EMs is not upbeat. Recently, the International Monetary Fund (IMF) trimmed growth projections of EMs to 4.0% in 2015, down from 4.6% in 2014. This would be the fifth straight year of slower growth.

Weaker growth in EMs in the past five years has left their asset markets less attractive. Uncertainty about the Chinese economy has extended to nations that sell to China. Worries about possible Federal Reserve tightening have added to the anxiety; even if the exit is well- managed, some further outflows of capital from EMs is likely.

The reversal of EM capital flows has the potential to develop into a negative loop. Faltering growth kindles investor retreat, which further hinders growth, etc. But well-managed economies can sustain themselves during periods like this with the application of some key strategies.  First, is it essential that central banks in EMs maintain adequate reserves to protect their currencies in the face of rising capital outflows. China has used some of its vast reserves this year to contain its markets, and oil-exporting EMs have sold foreign-exchange reserves as lower oil prices led to wider current account deficits. Brazil, China and India do not face a shortage of foreign-exchange reserves, but Indonesia, South Africa and Turkey are in a tight spot.

First, is it essential that central banks in EMs maintain adequate reserves to protect their currencies in the face of rising capital outflows. China has used some of its vast reserves this year to contain its markets, and oil-exporting EMs have sold foreign-exchange reserves as lower oil prices led to wider current account deficits. Brazil, China and India do not face a shortage of foreign-exchange reserves, but Indonesia, South Africa and Turkey are in a tight spot.

Second, EMs should strictly limit the borrowing they do in currencies which are not their own. Non-financial corporate debt in EMs is estimated to have risen from $4 trillion in 2004 to more than $18 trillion in 2014. The weakening of EM currencies renders the cost of servicing this debt higher. If growth is not robust, corporate defaults could rise and affect the banking system adversely. This chain of events could threaten economic growth.

Third, EM central banks need to stick to their mandates. While it is tempting to ease credit when times get tough, containing inflation is central to sustaining the confidence of the international investor community. China, India, Mexico, South Korea, Singapore and Taiwan are examples of EMs with low inflation, but Brazil is an outlier. The independence of a central bank from its government can help it make tough choices, when needed.

Fourth, keeping debt and deficits under control limits the need to tap international credit markets. India and Brazil are at the vulnerable end of the fiscal-health spectrum; Mexico, Malaysia and South Africa are in challenging but less-severe positions. The budgetary situations of China and Indonesia are more-favorable.

And finally, international investors are hesitant to engage with countries that are corrupt. Transparency and the rule of law are qualities that are elemental to market function. Several EMs have compounded their cyclical challenges with scandals that paint them in a decidedly unfavorable light. Brazil and Malaysia, in particular, have made headlines with political misbehavior that reaches to the highest levels of government.

On all of these fronts, it is far easier to establish discipline when times are good. Some EMs have operated with this perspective, but others used foreign capital a little bit more aggressively when it was flowing in freely. Those latter markets will have to work harder to adjust now that the money is no longer as easy.

The Fed Votes No Confidence

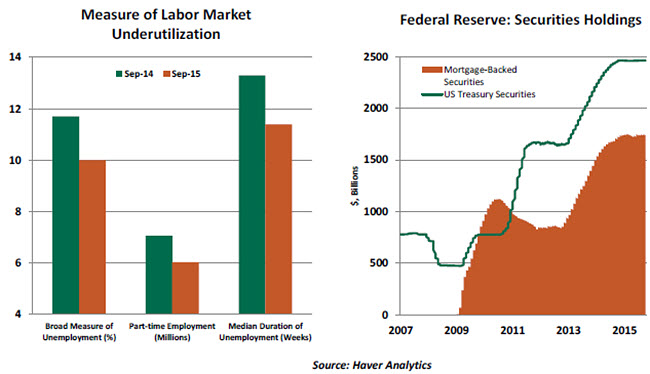

The September meeting of the Federal Open Market Committee (FOMC) disappointed and confused many observers, so there was keen interest in the minutes of that meeting. Released yesterday, those minutes reveal a group struggling to gain confidence and clarity around the economic outlook. Without these ingredients, a change of monetary policy is unlikely.

The minutes noted that “because of the risks to the outlook for economic activity and inflation (arising from international developments), the Committee decided that it was prudent to wait for additional information confirming that the economic outlook had not deteriorated and that inflation would gradually move up toward 2 percent over the medium term.”  There was a difference of opinion about labor market conditions. A few noted that underutilization in labor markets has been eliminated, while others held that additional progress was necessary. The relatively disappointing September employment report will likely not lead the latter camp to feel more comfortable with the situation.

There was a difference of opinion about labor market conditions. A few noted that underutilization in labor markets has been eliminated, while others held that additional progress was necessary. The relatively disappointing September employment report will likely not lead the latter camp to feel more comfortable with the situation.

The meeting included a staff presentation on options to eventually normalize the Fed’s balance sheet. The staff explored two options – (1) reinvestment ends “soon after initial policy firming” and (2) reinvestment stops after the federal funds rate reaches 1% or 2%. The staff concluded that if economic conditions were consistent with the Fed’s baseline forecast, the macroeconomic outcome of the two options would be nearly similar. But they pointed out that postponing balance sheet normalization has the advantage of allowing room for a larger adjustment of the federal funds rate if economic conditions weakened. This suggests that a cautious Fed will opt for a later date to stop reinvestment.

Overall, the tone of the minutes reflects a level of uncertainty that may take some time to clear. The conviction among the group that inflation will eventually converge toward the Fed’s 2% target has ebbed in the face of persistent disinflationary trends, which may be exacerbated by slower growth in emerging markets. The outlook could certainly brighten in time for a rate hike in December, but the odds are declining.

The information herein is based on sources which The Northern Trust Company believes to be reliable, but we cannot warrant its accuracy or completeness. Such information is subject to change and is not intended to influence your investment decisions.

Recommended Content

Editors’ Picks

EUR/USD edges lower toward 1.0700 post-US PCE

EUR/USD stays under modest bearish pressure but manages to hold above 1.0700 in the American session on Friday. The US Dollar (USD) gathers strength against its rivals after the stronger-than-forecast PCE inflation data, not allowing the pair to gain traction.

GBP/USD retreats to 1.2500 on renewed USD strength

GBP/USD lost its traction and turned negative on the day near 1.2500. Following the stronger-than-expected PCE inflation readings from the US, the USD stays resilient and makes it difficult for the pair to gather recovery momentum.

Gold struggles to hold above $2,350 following US inflation

Gold turned south and declined toward $2,340, erasing a large portion of its daily gains, as the USD benefited from PCE inflation data. The benchmark 10-year US yield, however, stays in negative territory and helps XAU/USD limit its losses.

Bitcoin Weekly Forecast: BTC’s next breakout could propel it to $80,000 Premium

Bitcoin’s recent price consolidation could be nearing its end as technical indicators and on-chain metrics suggest a potential upward breakout. However, this move would not be straightforward and could punish impatient investors.

Week ahead – Hawkish risk as Fed and NFP on tap, Eurozone data eyed too

Fed meets on Wednesday as US inflation stays elevated. Will Friday’s jobs report bring relief or more angst for the markets? Eurozone flash GDP and CPI numbers in focus for the Euro.