USDA cattle report clickbait?

This week, I joined guest host Tommy Grisafi on RFD-TV’s Cow Guy Close to discuss the current situation for cattle ranchers and beef consumers. Going into the hit, I had quite a few things I wanted to say but failed to articulate; live TV is harder than it looks! Accordingly, I was compelled to organize my thoughts in a written piece.

Cattle supplies are tight, but demand is not guaranteed

As of the latest USDA report, it was official. US ranchers have fewer heads of cattle now than they have had since the early 1950s. This astonishing statistic is getting a lot of attention, as it should. However, it feels like clickbait material rather than a reason to be bullish cattle.

There is a lot of focus on supply due to the recent USDA report, but Demand is not guaranteed. In fact, it might take a few years for ranchers to normalize their inventory, but Demand for beef can shift on a dime. Main Street America is making more than they ever have, but they are paying more for everything. The post-COVID euphoria spending does have an expiration date; in our opinion, the consumer will start feeling vulnerable sooner rather than later.

Consumers have been resilient thus far, yet we cannot forget that price will eventually matter, and there are substitutes for beef. They might not be as tasty, but chicken and pork are sufficient for most dinner tables. According to the USDA, supplies are slightly tighter now than in 2014, but what we witnessed in 2014 wasn’t “higher for longer” beef prices, as some suggest the most recent inventory report will lead to. On the contrary, we saw cattle prices weaken substantially in 2014 on the heels of what appeared to be, at the time, the most bullish news possible. Lastly, mainstream media has finally jumped on the low inventory story, which has historically been a relatively decent contrarian indicator.

Like other commodity industries, science and technology are working in favor of consumers. It should also be noted that the USDA report getting all of the attention is based on the head of cattle, but the weight of the animals today is higher than what we’ve seen historically. Thus, producing the same amount of beef takes fewer heads of cattle. With this in mind, the shock and awe of the USDA headline “lowest cattle and calves inventory since 1951” should be diluted.

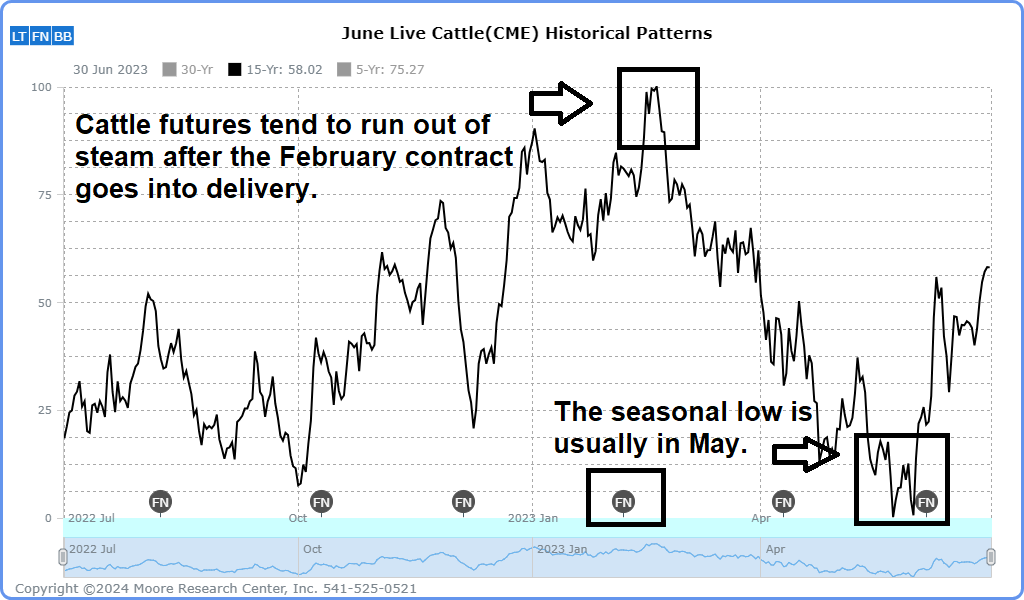

From a seasonal standpoint, the cattle market generally finds a top in early or mid-February and often doesn’t find a bottom until July. Thus, despite the overwhelming bullish narrative, annual price patterns are working against the rally.

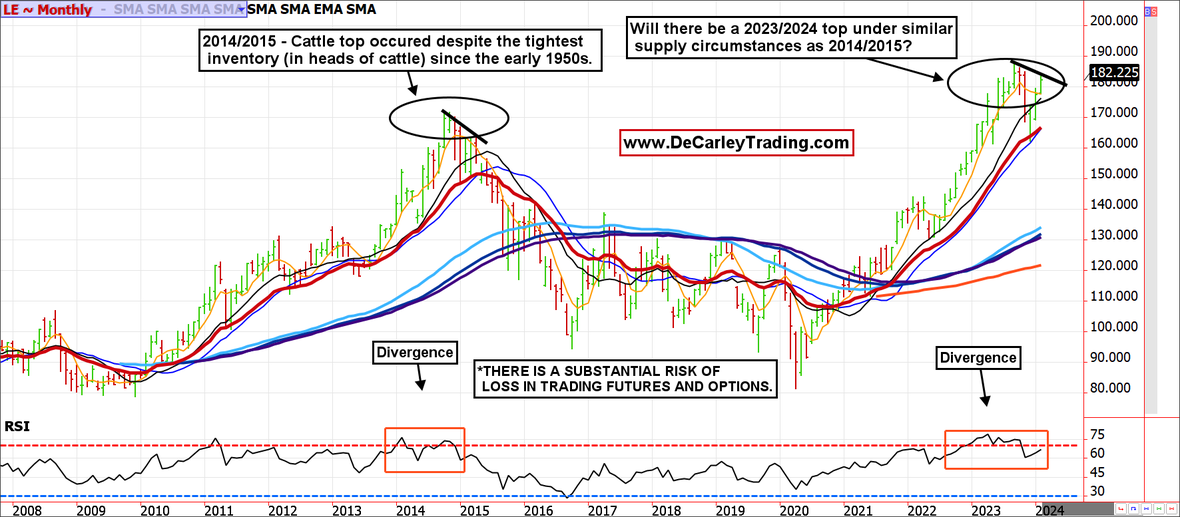

Monthly chart

A monthly chart of Live Cattle futures shows eerie similarities in current price action relative to the 2014/2015 top. We prefer to be wrong for the sake of ranchers, but there is a good chance we will repeat the sell-off. Commodity rallies rarely survive time; we doubt this will be an exception.

One of the tell-tale signs that a prolonged trend is running out of steam is oscillator divergence. This occurs when the futures price is making new highs, but indicators are not. The monthly chart above shows that price outperformed the oscillator as the 2014/2015 top was forming (in this chart, we are using the RSI, or Relative Strength Index). Many reading this might shrug it off as arbitrary or witchcraft, but this phenomenon works more for unknown reasons than it doesn’t. We also see similarities in the price action and timing of that price action. For instance, the 2014/2015 rally spiked to fresh all-time highs in the late fall but struggled the next few months as market participants shifted from a “buy the dips” mindset to a “sell rallies mindset.” This process involved significant dips and wild snapback rallies, but the ultimate result was a multi-year bear market.

Conclusion

The cattle supply per head is tight, but by weight, the shortage is less catastrophic. Furthermore, Demand is not guaranteed. The jury is still out, but we should be prepared for a repeat and act accordingly.

Author

Carley Garner

DeCarley Trading

Carley Garner is an experienced commodity broker with DeCarley Trading, a division of Zaner, in Las Vegas, Nevada. She is also the author of multiple books including, “Higher Probability Commodity Trading” and “A Trader's First Book on Commodities”.