US yield curve continues to flatten on falling inflation expectations

Outlook:

We get durables today and it could be a negative—Bloomberg forecasts a drop of 0.6%. Tomorrow we get consumer confidence and the Dallas and Chicago Fed surveys. Friday, it's the University of Michigan consumer sentiment and inflation expectations.

The important one is personal income and spending on Friday, which is sure to renew talk about the missing inflation.

Central bank speakers abound, including Draghi today and Kashkari and Yellen tomorrow. All told, we get five Fed speakers this week. The task is to convince the fixed income crowd that inflation and infla-tion expectations are not the relevant data. Good luck with that.

The US yield curve continues to flatten on falling inflation expectations—and foreign inflows. The FT shows a chart of the falling 10-year breakeven rate and another, from Bloomberg, of the 2-30 yield curve. The spread is now a 10-year low of 137 basis points, from over 200 bp near year-end.

"The difference between two and 10-year Treasury yields, another popular measure, has fallen to 80bp, close to the nine-year low of 75bp touched last summer. The yield curve has been flattening as a result of the Federal Reserve raising interest rates, which pushes up the policy-sensitive two-year Treasury yield. Meanwhile, longer term government bond yields have fallen, reflecting ebbing expectations for growth and inflation, with the latter reinforced of late by weakening oil prices."

Well, okay, but without showing comparable rate spreads, the FT admits the long end is being propped up by global inflows from places (Europe, Japan) where the return is negative. And as Greenspan iden-tified a long time ago in his conundrum, this has almost nothing to do with the US economic outlook. Besides, it's nice for the mortgage market.

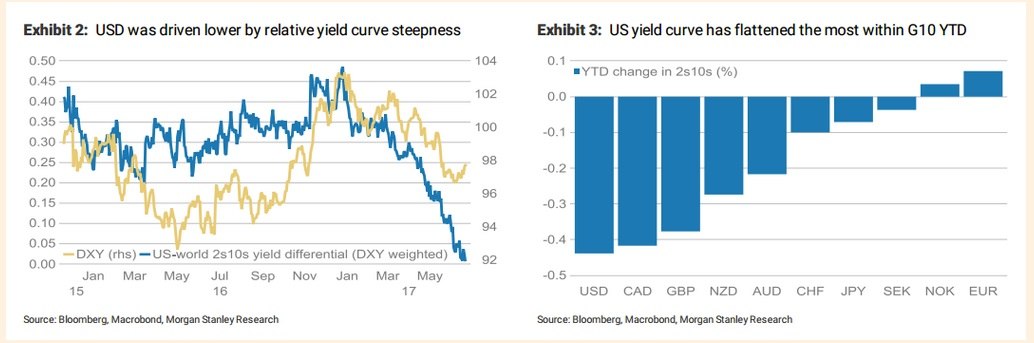

The contrary view is held by Morgan Stanley, which points out that the relative yield curve is flattening in the US more than elsewhere and the most among G10. The chart seems to show a strong correlation of the dollar with the falling yield curve. The Fed speaks but the market decides, and the market thinks the Fed is making a mistake. "... the markets increasingly disagree with the Fed. Despite the Fed pro-jecting it will hike rates by 100bp by the end of next year, the markets are only pricing in 37bp."

Here's the question: do FX traders make decisions based on relative yield curves? Do their big investment managers? On the whole, the correlation is with the 10-year yield differential alone, not the curve.

We know that foreign money has been flooding into the US fixed income market and presumably it comes from some other market, assuming it stays in the same asset class. Why would global investors not be buying dollars? One answer may be that they already have the dollars on hand, in cash or possibly from sales of equities. And to bring up the ghost of Greenspan again, at some point investors will decide they have enough dollars.

In a nutshell, determining sentiment about the dollar is as tricky as it ever gets, full of conflicting information.

Politics: Congress is aiming for a vote on the new healthcare bill this week, before the July 4th holiday next Tuesday. We get the verdict of the green eyeshade boys at the Congressional Budget Office today. As noted before, Trump promised not to touch Medicaid and promised coverage for everyone and on better terms than Obamacare, but this will not be true. There is some possibility the bill not get to the floor because a sufficient number of Republicans will break ranks. Meanwhile, the Dems are tiresomely hysterical.

The issue is that so far, the 38% of voters who supported Trump in the first place still support him. It remains to be seen whether losing Medicaid will affect that support. If not, the pitchfork mentality— throw the bums out—will have won. This is the outcome we expect—this time. But longer run, Bernie Sanders is right. The US is the only major country that doesn't provide universal healthcare at the federal level. Of course, all those other major countries don't pay anything close to what the US pays for its military capability, either.

On Friday the NYT published a lengthy story, with graphics, about Trump's many, many lies. "There is simply no precedent for an American president to spend so much time telling untruths. Every president has shaded the truth or told occasional whoppers. No other president — of either party — has behaved as Trump is behaving. He is trying to create an atmosphere in which reality is irrelevant." We like this one:

Note to Readers: RTS has launched a Trade Copier service. We place our trades from the Afternoon Traders' Advisory in the retail spot market and your MT4 account mirrors the trades taken in the RTS account. You don't have to lift a finger. You get to pick how much leverage and exactly which curren-cies you want to include. If you are interested, please contact Paul Harris at [email protected] or visit http://www.rtsforex.com/trade-copier/.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 111.70 | LONG USD | 06/21/17 | STRONG | 111.09 | 0.55% |

| GBP/USD | 1.2716 | SHORT GBP | 06/12/17 | STRONG | 1.2701 | -0.12% |

| EUR/USD | 1.1180 | SHORT EURO | 06/12/17 | WEAK | 1.1218 | 0.34% |

| EUR/JPY | 124.87 | SHORT EURO | 07/08/17 | WEAK | 123.65 | -0.99% |

| EUR/GBP | 0.8791 | LONG EURO | 04/25/17 | STRONG | 0.8490 | 3.55% |

| USD/CHF | 0.9730 | LONG USD | 06/12/17 | WEAK | 0.9675 | 0.57% |

| USD/CAD | 1.3251 | SHORT USD | 05/17/17 | STRONG | 1.3621 | 2.72% |

| NZD/USD | 0.7266 | LONG NZD | 05/30/17 | STRONG | 0.7062 | 2.89% |

| AUD/USD | 0.7571 | LONG AUD | 06/08/17 | STRONG | 0.7548 | 0.30% |

| AUD/JPY | 84.56 | LONG AUD | 06/16/17 | WEAK | 84.65 | -0.11% |

| USD/MXN | 17.9462 | SHORT USD | 05/17/17 | STRONG | 18.7098 | 4.08% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat