Economic forecasting in the run-up to and during recessions is particularly challenging. An analysis of the Federal Reserve of Philadelphia’s survey of professional forecasters shows that, since 1968, forecast errors during recessions are significantly higher than during non-recession periods. Moreover, forecast errors during recessions are predominantly positive, so forecasts tend to be too optimistic, even if they concern the next quarter. At the current juncture, there is broad consensus, if not unanimity, that downside risks to growth dominate due to the multiple headwinds and uncertainties. The historical forecast record is another reason to be mindful of these risks.

A recession is a period of high uncertainty: how much will demand, activity, employment, and corporate profits decline? How long will it last? For economic forecasters, it is a stressful period: the pressure to produce good forecasts rises proportionally to the difficulty of doing so because during a recession, the economy is in a state of flux. The relationships between the components of final demand -consumption, capital formation, exports- and their drivers become less predictable due to confidence effects, financial constraints, non-linearities, etc.

In 2018, a working paper of the IMF concluded that “while forecasts in recession years are revised each month, they do not capture the onset of recessions in a timely way and the extent of output decline during recessions is missed by a wide margin.” This result held for private as well as public sector forecasts.

Capturing the onset of a recession is particularly difficult: when will the tipping point be reached whereby an economy reacts to recent shocks in such a way that it corresponds to a recession? The IMF paper gives a sobering conclusion for advanced and emerging economies, but what about forecasts for the US specifically? The question is important given the weight of the US in the world.

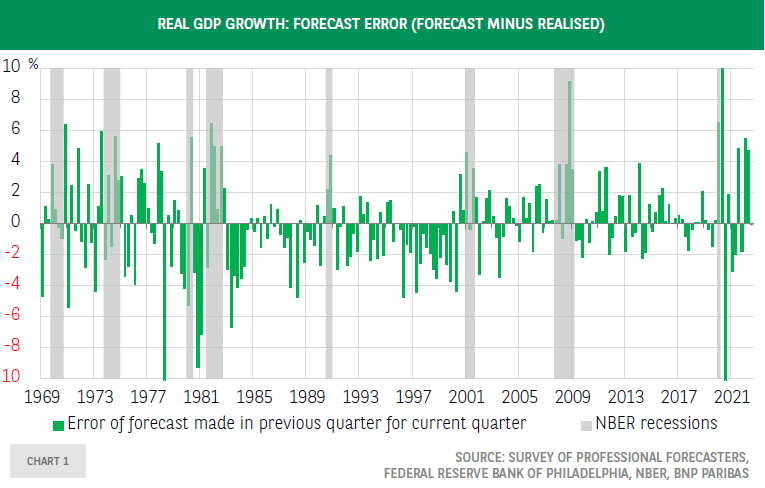

Chart 1 shows the forecast errors of the Survey of Professional Forecasters (SPF) conducted by the Federal Reserve Bank of Philadelphia.23 The forecasts concern those made in the current quarter for the next quarter (henceforth labeled as Q-1).

At first glance it seems that recessions tend to be marked by large positive forecast errors, which implies that the depth of the recessions was underestimated. To analyse this in detail, chart 2 distinguishes between recession and non-recession periods and shows the results for various forecast horizons. The metric that is used is the root mean squared error (RMSE). One would expect an improvement of the forecast quality -a decline in the RMSE- when the forecast horizon shortens.

This is indeed the case during recession periods, but outside these, the RMSE is stable across the different forecast horizons. The forecast errors for periods when the US was in recession are also considerably higher compared to non-recession periods. For longer forecast horizons -four or three quarters ahead-, this could reflect that recessions come as a surprise. For shorter horizons, including quarters when the economy was already in recession when the forecasts were made, it could be the result of new shocks and hard to anticipate dynamics during the recession. Another interpretation is that it is extremely difficult to anticipate the contraction of GDP during recessions.

Finally, as shown by the table, forecasts covering periods when the US was in recession, are too optimistic by a wide margin: this is the case for 70% of the forecasts for the next quarter and the number increases to 89% for the four quarters ahead forecast. At the current juncture, there is broad consensus, if not unanimity, amongst forecasters that downside risks to growth dominate due to the multiple headwinds and uncertainties. The historical forecast record also underpins this distribution of risks.

BNP Paribas is regulated by the FSA for the conduct of its designated investment business in the UK and is a member of the London Stock Exchange. The information and opinions contained in this report have been obtained from public sources believed to be reliable, but no representation or warranty, express or implied, is made that such information is accurate or complete and it should not be relied upon as such. This report does not constitute a prospectus or other offering document or an offer or solicitation to buy any securities or other investment. Information and opinions contained in the report are published for the assistance of recipients, but are not to be relied upon as authoritative or taken in substitution for the exercise of judgement by any recipient, they are subject to change without notice and not intended to provide the sole basis of any evaluation of the instruments discussed herein. Any reference to past performance should not be taken as an indication of future performance. No BNP Paribas Group Company accepts any liability whatsoever for any direct or consequential loss arising from any use of material contained in this report. All estimates and opinions included in this report constitute our judgements as of the date of this report. BNP Paribas and their affiliates ("collectively "BNP Paribas") may make a market in, or may, as principal or agent, buy or sell securities of the issuers mentioned in this report or derivatives thereon. BNP Paribas may have a financial interest in the issuers mentioned in this report, including a long or short position in their securities, and or options, futures or other derivative instruments based thereon. BNP Paribas, including its officers and employees may serve or have served as an officer, director or in an advisory capacity for any issuer mentioned in this report. BNP Paribas may, from time to time, solicit, perform or have performed investment banking, underwriting or other services (including acting as adviser, manager, underwriter or lender) within the last 12 months for any issuer referred to in this report. BNP Paribas, may to the extent permitted by law, have acted upon or used the information contained herein, or the research or analysis on which it was based, before its publication. BNP Paribas may receive or intend to seek compensation for investment banking services in the next three months from an issuer mentioned in this report. Any issuer mentioned in this report may have been provided with sections of this report prior to its publication in order to verify its factual accuracy. This report was produced by a BNP Paribas Group Company. This report is for the use of intended recipients and may not be reproduced (in whole or in part) or delivered or transmitted to any other person without the prior written consent of BNP Paribas. By accepting this document you agree to be bound by the foregoing limitations. Analyst Certification Each analyst responsible for the preparation of this report certifies that (i) all views expressed in this report accurately reflect the analyst's personal views about any and all of the issuers and securities named in this report, and (ii) no part of the analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed herein. United States: This report is being distributed to US persons by BNP Paribas Securities Corp., or by a subsidiary or affiliate of BNP Paribas that is not registered as a US broker-dealer, to US major institutional investors only. BNP Paribas Securities Corp., a subsidiary of BNP Paribas, is a broker-dealer registered with the Securities and Exchange Commission and is a member of the National Association of Securities Dealers, Inc. BNP Paribas Securities Corp. accepts responsibility for the content of a report prepared by another non-US affiliate only when distributed to US persons by BNP Paribas Securities Corp. United Kingdom: This report has been approved for publication in the United Kingdom by BNP Paribas London Branch, a branch of BNP Paribas whose head office is in Paris, France. BNP Paribas London Branch is regulated by the Financial Services Authority ("FSA") for the conduct of its designated investment business in the United Kingdom and is a member of the London Stock Exchange. This report is prepared for professional investors and is not intended for Private Customers in the United Kingdom as defined in FSA rules and should not be passed on to any such persons. Japan: This report is being distributed to Japanese based firms by BNP Paribas Securities (Japan) Limited, Tokyo Branch, or by a subsidiary or affiliate of BNP Paribas not registered as a financial instruments firm in Japan, to certain financial institutions permitted by regulation. BNP Paribas Securities (Japan) Limited, Tokyo Branch, a subsidiary of BNP Paribas, is a financial instruments firm registered according to the Financial Instruments and Exchange Law of Japan and a member of the Japan Securities Dealers Association. BNP Paribas Securities (Japan) Limited, Tokyo Branch accepts responsibility for the content of a report prepared by another non-Japan affiliate only when distributed to Japanese based firms by BNP Paribas Securities (Japan) Limited, Tokyo Branch. Hong Kong: This report is being distributed in Hong Kong by BNP Paribas Hong Kong Branch, a branch of BNP Paribas whose head office is in Paris, France. BNP Paribas Hong Kong Branch is regulated as a Licensed Bank by the Hong Kong Monetary Authority and is deemed as a Registered Institution by the Securities and Futures Commission for the conduct of Advising on Securities [Regulated Activity Type 4] under the Securities and Futures Ordinance Transitional Arrangements. Singapore: This report is being distributed in Singapore by BNP Paribas Singapore Branch, a branch of BNP Paribas whose head office is in Paris, France. BNP Paribas Singapore is a licensed bank regulated by the Monetary Authority of Singapore is exempted from holding the required licenses to conduct regulated activities and provide financial advisory services under the Securities and Futures Act and the Financial Advisors Act. © BNP Paribas (2011). All rights reserved.

Recommended Content

Editors’ Picks

EUR/USD edges lower toward 1.0700 post-US PCE

EUR/USD stays under modest bearish pressure but manages to hold above 1.0700 in the American session on Friday. The US Dollar (USD) gathers strength against its rivals after the stronger-than-forecast PCE inflation data, not allowing the pair to gain traction.

GBP/USD retreats to 1.2500 on renewed USD strength

GBP/USD lost its traction and turned negative on the day near 1.2500. Following the stronger-than-expected PCE inflation readings from the US, the USD stays resilient and makes it difficult for the pair to gather recovery momentum.

Gold struggles to hold above $2,350 following US inflation

Gold turned south and declined toward $2,340, erasing a large portion of its daily gains, as the USD benefited from PCE inflation data. The benchmark 10-year US yield, however, stays in negative territory and helps XAU/USD limit its losses.

Bitcoin Weekly Forecast: BTC’s next breakout could propel it to $80,000 Premium

Bitcoin’s recent price consolidation could be nearing its end as technical indicators and on-chain metrics suggest a potential upward breakout. However, this move would not be straightforward and could punish impatient investors.

Week ahead – Hawkish risk as Fed and NFP on tap, Eurozone data eyed too

Fed meets on Wednesday as US inflation stays elevated. Will Friday’s jobs report bring relief or more angst for the markets? Eurozone flash GDP and CPI numbers in focus for the Euro.