US economy picks up, greenback, Wall Street extend gains into Q3

Private Payroll Increase, Vaccine Take-Up, Fed Speak Lift USD

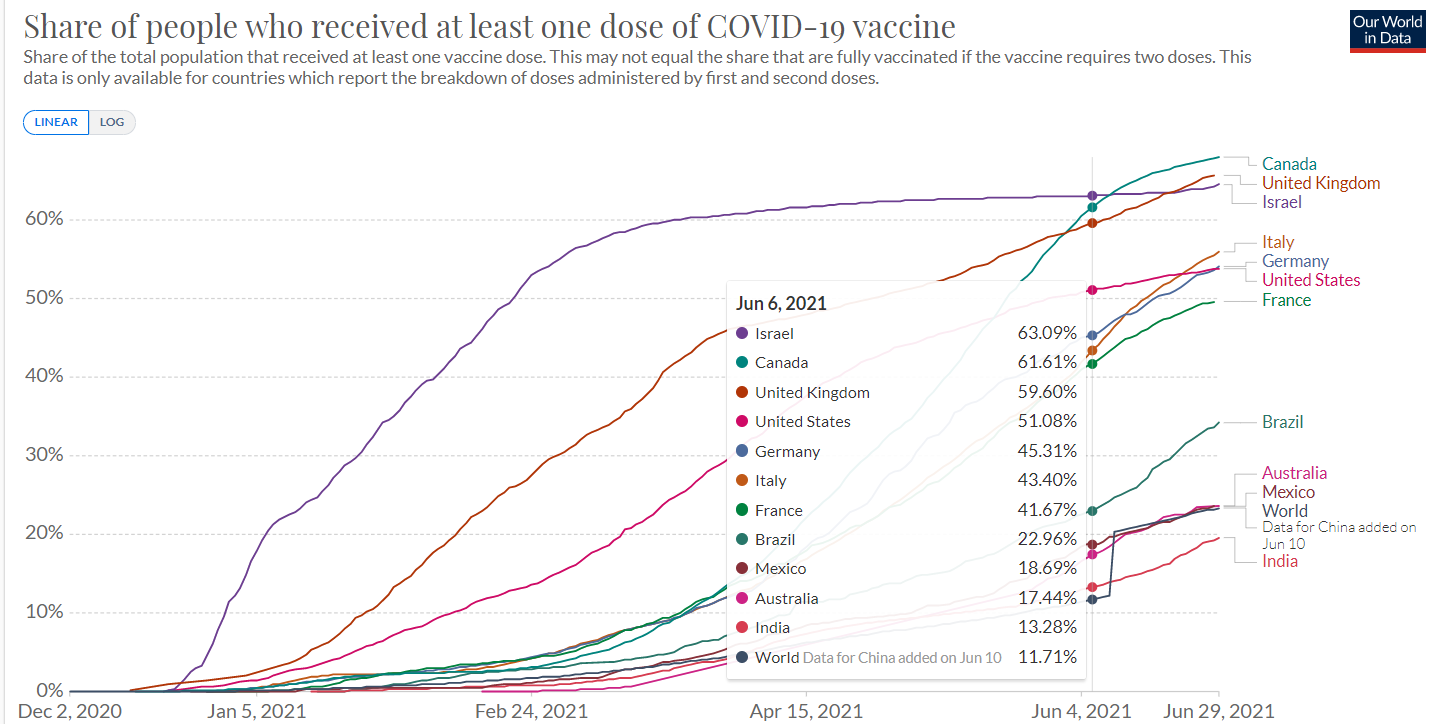

Summary: US Stocks and the Dollar ended the final day of June higher after ADP Private Payrollsrose 692,000 in June, beating expectations (600,000). Although the May number was revised down, investor optimism for an economic comeback continued. With nearly 60% of US adults having received a Covid-19 vaccine, investors are expecting the economy to start strong in H2. In contrast, many other parts of the world are struggling with lagging vaccine roll outs where the Delta variant is spreading quickly. The Dollar Index (USD/DXY), a popular gauge of the Greenback’s value against a basket of 6 major currencies, rose 0.33% to 92.35,(92.05 yesterday) its highest close since early April. The Euro extended its losses, sliding 0.36% to 1.1858(1.1902), the lowest close since April 9. Sterling lost 0.21%, settling at 1.3835 (1.3850) weighed by broad-based USD strength. The Aussie (AUD/USD) grinded lower to 0.7495 from 0.7515 amidst a Covid-19 resurgence coupled with a slow vaccine take-up and which saw state borders closed. Against the Japanese Yen, the Dollar soared 0.50% to 111.08 (110.53), a 15-month high.Yesterday, new Bank of Japan board member Junko Nakagawa said that it was important to maintain monetary easing sustainably. The Dollar advanced 0.45% against the Swiss Franc (USD/CHF) to 0.9250 (0.9207). Against the Asian and Emerging Market currencies, the Greenback was mostly higher. USD/CNH rose to 6.46920 from 6.4640.

Wall Street stocks ended higher in slow trade to end the first half of 2021. The DOW gained 0.7% to 34,580 (34,340) while the S&P 500 rose to 4,305 (4,297). Bond yields were steady. The US 10-yearbond yield was unchanged at 1.47%. Germany’s 10-year Bund rate settled at -0.21% from -0.17%. Australia’s 10-year bond yielded 1.52% (1.53% yesterday) while Japan’s 10-year JGB yield was unchanged (0.05%).Dallas Fed President Robert Kaplan said he would prefer tapering soonerrather than later which would give more flexibility in the future.

Data released yesterday saw Japanese Preliminary IndustrialProduction in May (m/m) fall -5.9%, missing forecasts at -2.4%. China’s June Manufacturing PMI eased to 50.9 from 51.0 while Non-Manufacturing PMI slid to 53.5 from 55.2. Australia’s Private Sector Credit in May rose to 0.4%, beating estimates at 0.3%.Japan’s Consumer Confidence Index in June rose to 37.4 from 34.1 while Housing Starts climbed 9.9%, beating median forecasts at 8.3%.UK’s Final Q1 GDP slid to -1.6%, missing expectations of -1.5%. Switzerland’s KOF Economic Barometer fell to 133.4 from 143.2, lower than estimates at 144.7. Eurozone Core CPI in June matched forecasts at 0.9%.Canada’s GDPin May eased -0.3%, beating forecasts of -0.8%.US Pending Home Sales jumped 8.0% in May from a fall of 4.4% in April and the highest level since 2005. ECB President Christine Lagarde and Bank of England Governor both have speaking engagements at separate functions.

On the Lookout: While the Dollar starts off strong on the first trading day of Q3, today sees the release of more global economic data (Manufacturing PMI’s) as well as the US Weekly Jobless Claims. Tomorrow US Payrolls are released with economists expecting the US economy to have added between 683,000 and 690,000 (ACY Finlogix) jobs.

Today kicks off with Australia’s AIG Manufacturing Index for June (no forecasts, May was 61.8). New Zealand Building Consents for May follow (April was 4.8%, no forecasts). Japanese Q2 Large Tankan Manufacturing Index (f/c 15 from previous 5) and Tankan Non-Manufacturing Index (f/c 3 from -1) as well as Japanese Jibun June Manufacturing Index (f/c 51.5 from 53.0) follow. Australia’s May Trade Balance is next (f/c +AUD 10.0 billion from previous +AUD 8.02 billion). China follows next with its Caixin Manufacturing PMI for June report (f/c 51.8 from 52.0 – FX Factory). German May Retail Sales follows (f/c 5.0% from -5.5%). Swiss June CPI (f/c 0.2% from 0.3%) and May Retail Sales follow (f/c 17.5% from 35.7%). Spanish Manufacturing PMI (f/c 59.6 from 59.4), Italian Manufacturing PMI (f/c 62.2 from 62.3), French Manufacturing PMI (f/c 58.6 from 59.4), German Manufacturing PMI (f/c 64.9 from 64.4), and Eurozone Final Manufacturing PMI (f/c 63.1 from 63.1) are next.

UK Final Manufacturing PMI (f/c 64.2 from 65.6) and Eurozone Unemployment Rate for May (f/c 8% from 8%) round up European data. The US reports its Weekly Unemployment Claims (f/c 393,000 from 411,000), Challenger Job Cuts (last was 24.58k), Final Manufacturing PMI (f/c 62.6 from 62.1), ISM Manufacturing PMI (f/c 61.0 from 61.2), Construction Spending for June (f/c 0.4% from 0.2%), and finally, US ISM Manufacturing Prices (f/c 86.5 from 88.0). ECB President Christine Lagarde and Bank of England Governor Andrew Bailey have speaking engagements at separate functions.

Trading Perspective: With more economic data releases due in the next two days culminating with US Payrolls, expect the Dollar to consolidate its gains within recent ranges. While the Greenback’s gains were solid against most of the major currencies, against others (Asian and EM Currencies) advances were mild. A bit of caution warranted into Day one of Q3.

- USD/JPY – The Dollar outperformed against the Yen and Swiss Franc, considered the low-yielders. Yet US bond yields were unchanged with the benchmark 10-year note settling at 1.47%. Interestingly yields from global rivals were lower which added to the overall USD strength. Immediate resistance lies at 111.20 (overnight high 111.125) followed by 111.60 and then 112.00. Immediate support can be found at 110.70 and 110.40. Look for consolidation between 110.80 and 111.30 today. Tempted to sell near overnight highs but will be patient and see how this currency pair develops.

- AUD/USD – Slip-sliding away although the 0.7470/80 support level is solid. Next support comes in at 0.7440 and 0.7400. Immediate resistance lies at 0.7515 and 0.7545 and 0.7570. The Australian government is struggling to get its population to get vaccinated but the rising number of Covid infections may be the catalyst the Morrison government needs. Meantime border closures, particularly during current school holidays are hurting the economy. Interesting times for the Battler. Gut feel is to buy the dip first up.

- EUR/USD – the shared currency slumped, closing below the 1.1900 support level to finish at 1.1858, down 0.36%. Today Euro area and Eurozone Manufacturing PMIs are released, and ECB President Lagarde is due to deliver the opening remarks at the Hearing before the Committee on Economic and Monetary Affairs (via satellite). EUR/USD has immediate support at 1.1840 (overnight low 1.1845) followed by 1.1805. Immediate resistance lies at 1.1885 and 1.1915. Look for consolidation in a likely 1.1840-1.1890 range. Just trade the range shag on this one for now. Watch for the PMIs and Lagarde.

- GBP/USD – Sterling eased a modest 0.10% to 1.3835 from 1.3850 yesterday, mostly on broad-based US Dollar strength. GBP/USD has immediate support at 1.3800 (overnight low 1.37984) followed by 1.3760 and 1.3730 (strong). Immediate resistance can be found at 1.3850 and 1.3890. Bank of England Governor Andrew Bailey is due to speak at Mansion House in London (6 pm Sydney time). While the UK has had a relatively successful vaccine take up, the latest news sees a sharp increase in cases due to the EURO 2020 football Competition in stadiums at Wembley (London, England) and Hampton Park (Glasgow, Scotland). Sterling could be in for a pounding. Meantime, look to trade a likely range today between 1.3775-1.3875.

Happy Thursday and trading all.

Author

Michael Moran

ACY Securities

Michael has over 40 years’ FX experience, including running FX trading desks for some of the largest banks in the world.