US dollar remains strong as risk appetite recovers

Market Overview

When there is a sharp shift in sentiment on major geopolitical newsflow, markets can act quickly, however equally this knee-jerk reaction also tends to last only briefly before markets settle down again. The reaction to the US significantly ramping up the trade dispute with China hit risk appetite hard and saw a significant move towards a safe haven assets. However, already we see markets settling down again and moves being retraced. Subsequently we see bond yields having picked up, the Japanese yen unwinding its gains and Wall Street equities closing well off the day lows. Having hit 2.85% yesterday, the US 10 year yield is back above 2.90% again whilst the US dollar remains strong as yield differentials continue to move in its favour. So risk appetite is recovering, however all the while the US yield curve continues to bull flatten, something that is not conducive to sustained medium to longer term dollar strength. Despite this though, for now the greenback is performing well, with the Dollar Index pressuring the 95.15 October/November highs. As markets settle down, will the dollar which has been trading as a safe haven recently, continue to strengthen? EUR/USD breaking below $1.1500 would be a key gauge near term. The focus will be on Sintra today with many of the major central banks’ governors all speaking. Volatility across the forex majors could be elevated.

Wall Street closed well off its lows with the S&P 500 -0.4% lower (having been as much as -1.1% at one stage) whilst US equities futures are rising by +0.2% early today too. The Asian markets have also bounced back strongly with the Nikkei +1.2% whilst European markets are also set to be positive in early moves. In forex there has been further strength for the US dollar, whilst the riskier currencies (Aussie and Kiwi) looking to rebound. Positive risk appetite and a stronger dollar does not bode well for gold which is again struggling, whilst a bigger than expected drawdown on the API inventories and better risk has helped to support oil.

The big focus today for traders will come in the central bankers forum at Sintra, where from 1430BST a clutch of governors are expected to speak, including Jerome Powell (the Fed), Mario Draghi (ECB), Haruhiko Kuroda (BoJ) and Philip Low (RBA). This will cause potential volatility for the dollar, euro, yen and Australian dollar. It is another light day for the economic calendar today which does not really get going until the US Q1 Current Account balance at 1330BST. Consensus forecasts expects the current account deficit to widen to -$129.0bn (from -$128.2bn in Q4 2018) which would be the widest level since Q2 2012. The US Existing Home Sales are at 1500BST which are expected to increase to 5.52m (from 5.46m last month). The EIA oil inventories are at 1530BST and are expected to show the crude stocks again in drawdown by -2.7m (from a drawdown of -4.1m barrels last week), whilst distillates are expected to drawdown by -0.6m barrels (from -2.1m draw last week) and also the gasoline stocks are meant to be drawing down by -1.0m barrels (-2.3m last week). New Zealand Q1 GDP is announced at 2345BST and is expected to be +0.5% (+0.6% previous).

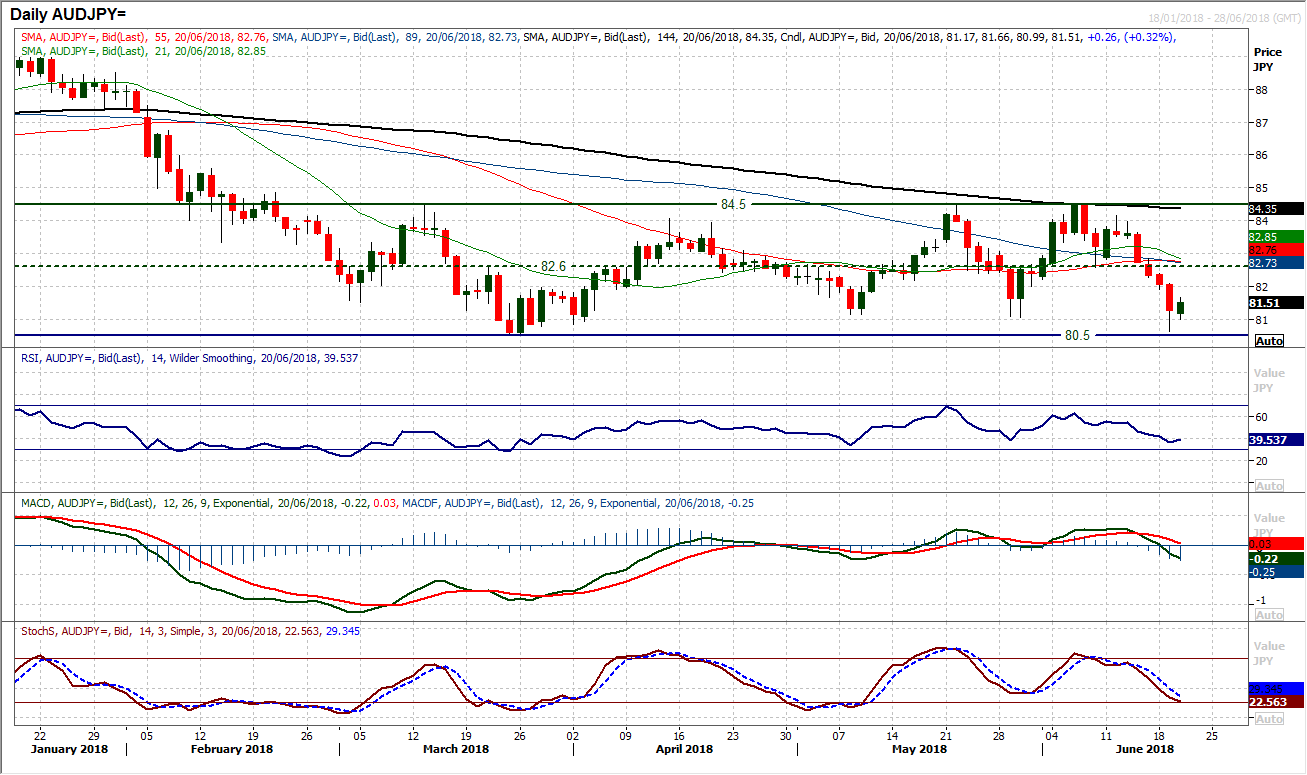

Chart of the Day – AUD/JPY

For months the range on Aussie/Yen has pulled higher and lower around the pivot at 82.60. This range of 400 pips between 80.50/84.50 has been very well-defined and conformed to some excellent ranging indicators. So with the Aussie under huge pressure yesterday and the safe haven yen finding significant gains, the pair pulled sharply lower yesterday to test the key support of the range low at 80.50. Is this the time to break the range? The technical indicators currently suggest that this is a test of the support and is not the precursor to a significant downside break. The RSI is into an area in the low 30s where rallies tend to take hold during this range, whilst there is no lead signal from either the MACD or Stochastics lines. The market closed outside the Bollinger Bands yesterday but the bands are broadly ranging still and this points towards a limited immediate downside potential. A decisive close below 80.50 would certainly increase the pressure, but the follow up candle to yesterday’s sharp session is crucial today. A close well off the low yesterday and an early rebound today raises expectations of playing the range. Building on initial support at 81.00 will help further.

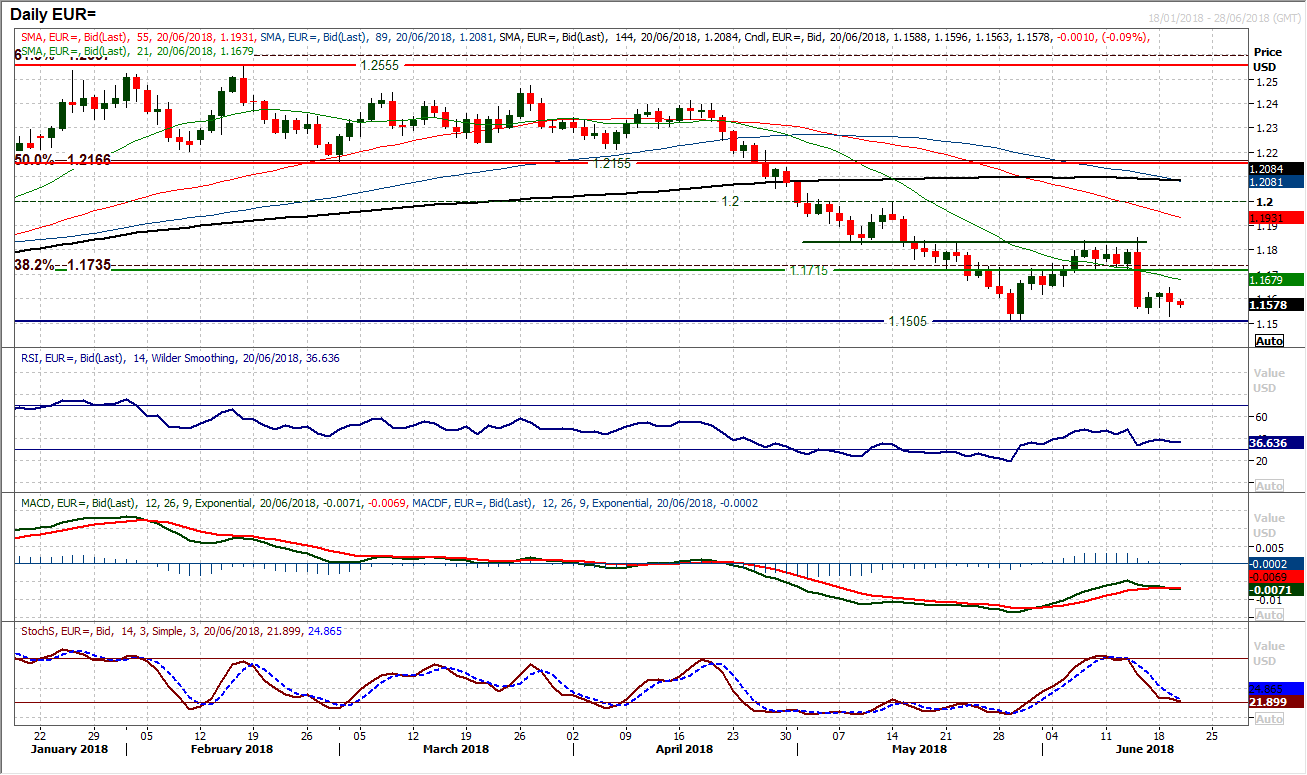

EUR/USD

In the context of recent moves on the euro, the implications of yesterday’s candlestick is rather difficult to ascertain. The support that looked to be building last Friday was broken by a sharp move to the downside yesterday morning, only for the market to partially rebound to leave a long lower candlestick shadow into the close. However a 35 pip close lower on the session can hardly be positive and the market has dropped back further initially today. The bulls will take the positives in that the key support at $1.1505 remains intact, but the threat remains. Momentum indicators are taking on an ominous deterioration once more and the resistance around a near term pivot on the hourly chart at $1.1640 is building. The bulls will have to work very hard to prevent a key breach of $1.1505.

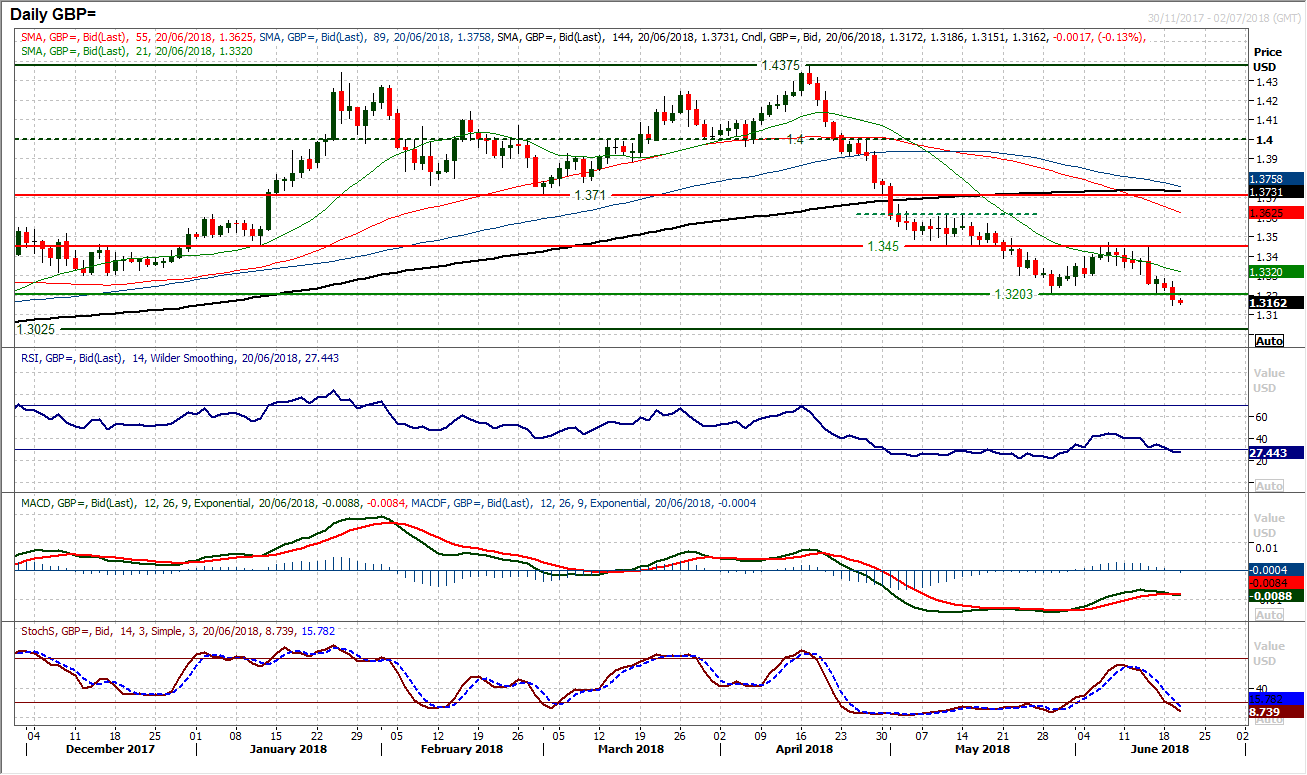

GBP/USD

The negative pressure on sterling in addition to the dollar strength, has pulled Cable lower to break below the key May low at $1.3203. The decisive closing breach of support continues the corrective move and opens $1.3025 which is the support from the October/November lows. The configuration on the momentum indicators does not look encouraging for the bulls as the RSI and Stochastics continue to track lower but also the MACD lines are just crossing back lower again too. The old floor around $1.3200 now becomes a basis of initial resistance today, with the hourly cart showing more considerable resistance $1.3275/$1.3300. Hourly momentum configuration is negatively configured to show that intraday rallies that unwind the hourly RSI towards 50/60 and the MACD lines towards neutral are a chance to sell. Initial support at $1.3150 but a retest of $1.3025 is looming.

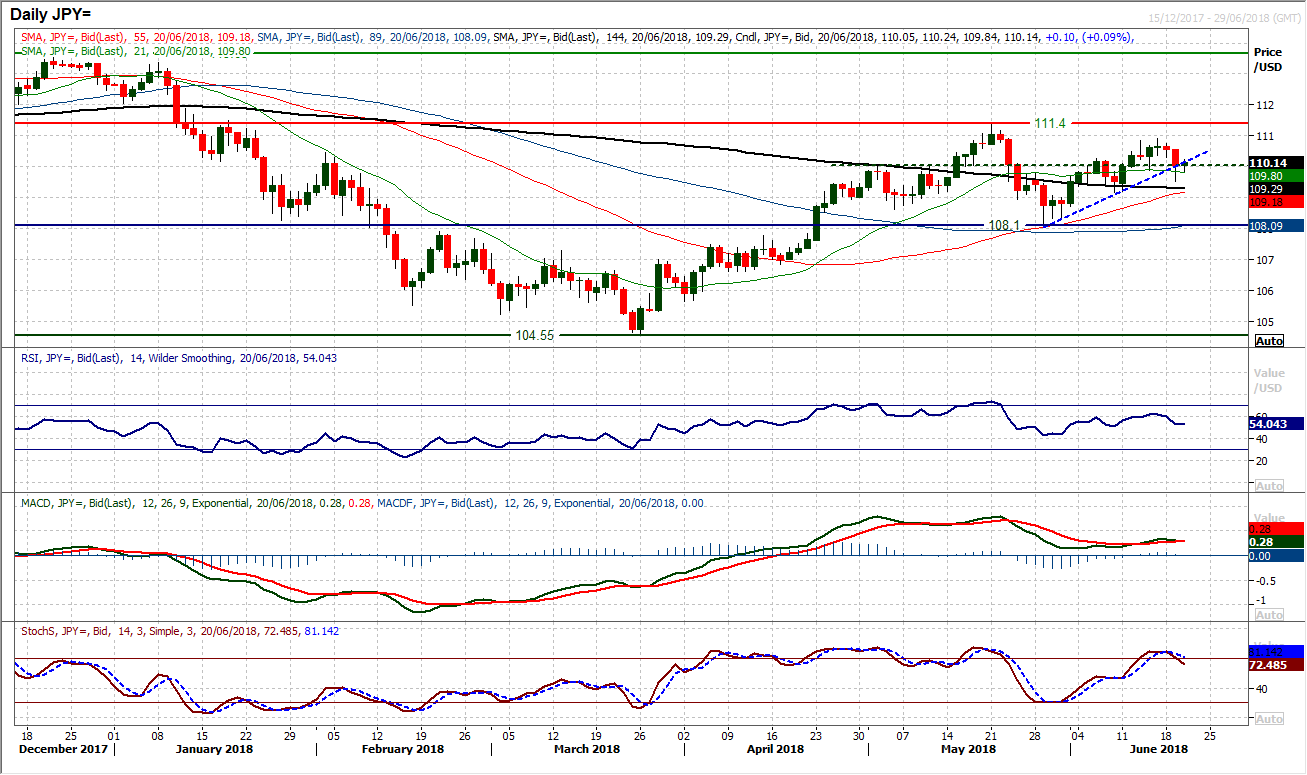

USD/JPY

Breaking the support of the three week uptrend shows how tentative the rally has been and suggests that this is a range play below 111.40. However, the bulls have rebounded off yesterday’s low around 109.50 and look to start again. An immediate bounce back above 110.00 is certainly encouraging, whilst the hourly chart shows how pushing through the resistance band 109.90/110.25 will be important near term for the bulls to consider pushing back towards 110.90 again. Momentum indicators are now configured marginally positive within a ranging outlook, which is fairly consistent with the market outlook in the range 108.10/111.40. The hourly chart shows the market needs to push consistently above 60 on hourly RSI and above neutral on MACD to form more consistently positive configuration. Above 110.25 initial resistance is 110.60 today.

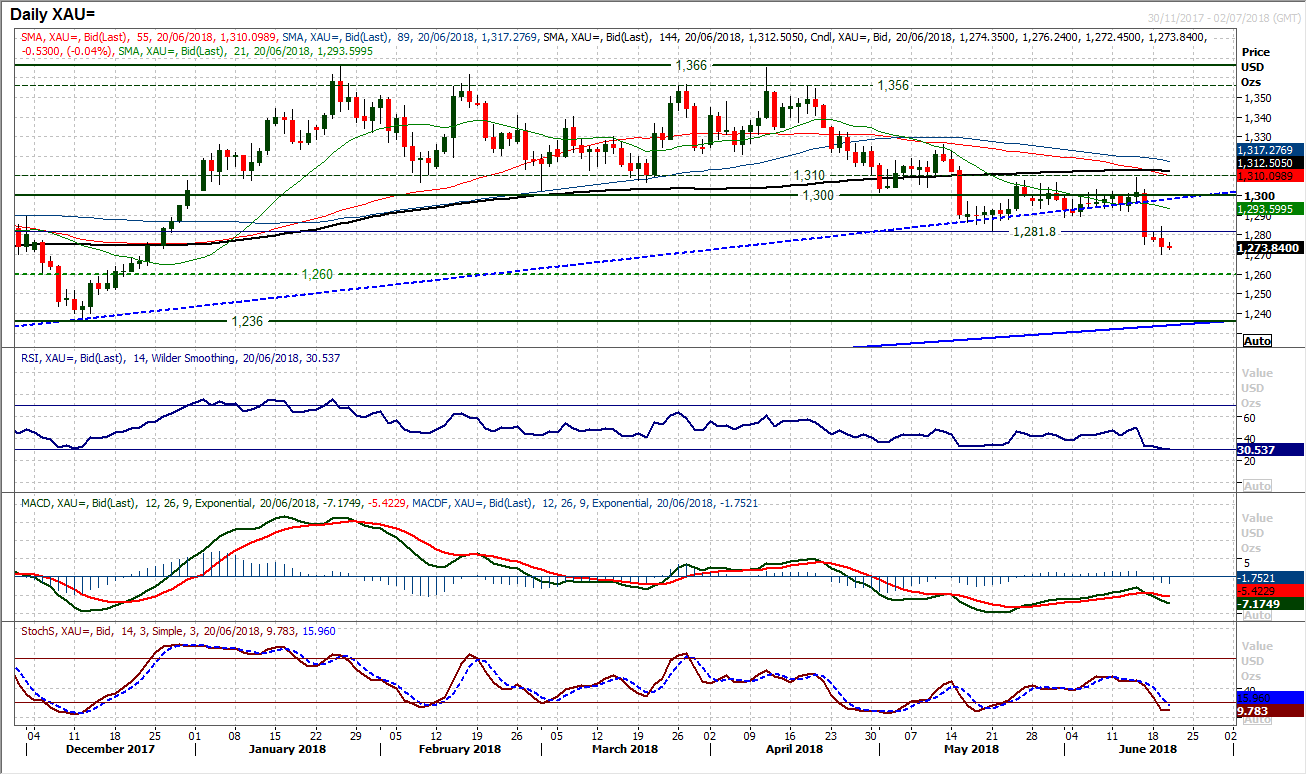

Gold

With such a significant risk-off bias across markets yesterday, the fact that gold fell into the close and posted a fairly negative one day candlestick will be a real concern for the bulls. Having broken below $1282 support on Friday, the market has done very little to suggest there could be a recovery and yesterday’s session will have been a real disappointment as the market fell back from $1284. Momentum indicators are very negatively configured with the RSI hovering in the low 30s, whilst MACD and Stochastics are in decline. This all suggests using intraday rallies as a chance to sell. Resistance at $1284 now adds to the overhead supply between $1289 and the key pivot band $1300/$1310. The medium term top pattern continues to imply a target of the key December low at $1236. Yesterday’s low at $1270 is initial support with minor support around $1260/$1265. The hourly chart shows around 60 on RSI and around neutral on MACD lines limits the rallies.

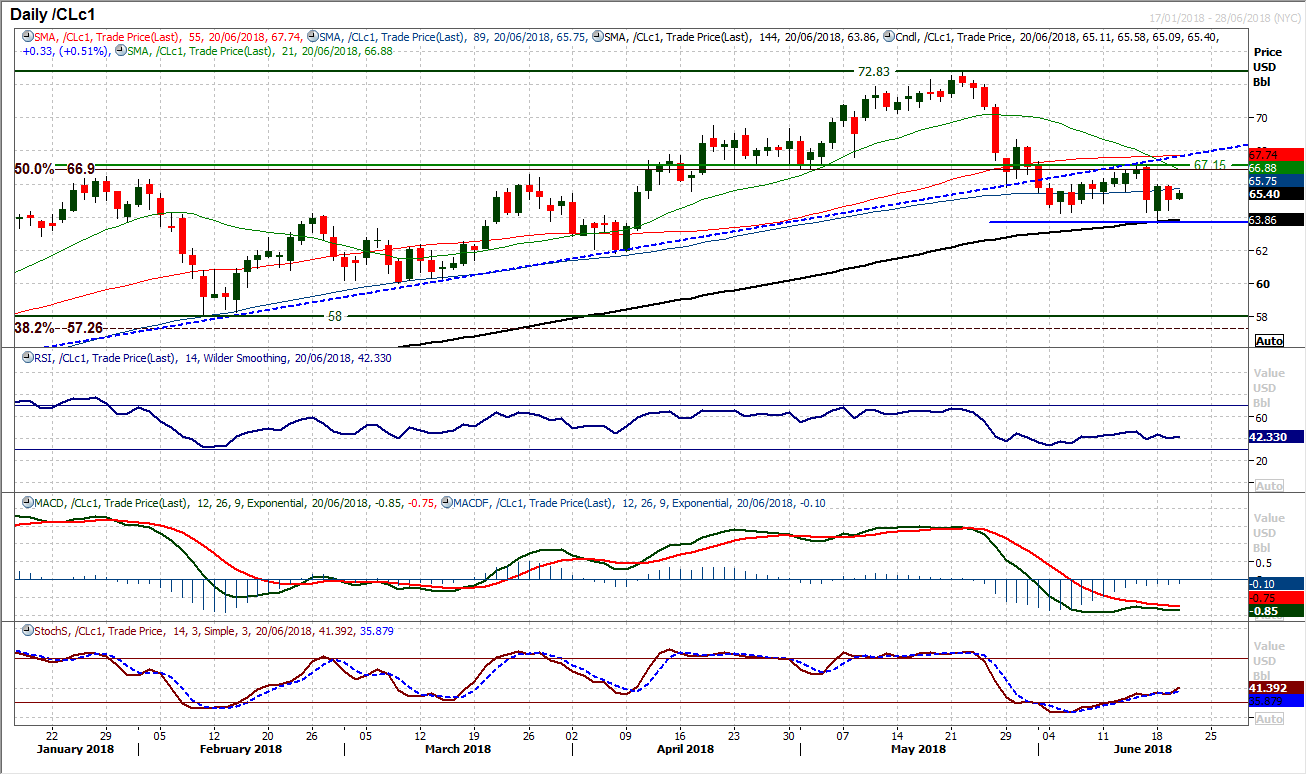

WTI Oil

Volatility has increased in the past few sessions as the market has flown around. Monday’s strong rebound was initially sold into, but then the market has gained support again on the API inventories drawdown yesterday. There is a negative bias over the past few weeks, but this phase of trading is turning into a range play now. Coming ahead of the OPEC meeting on Friday, perhaps this is understandable. The negative bias comes with the run of lower highs, the latest at $67.15 and with the RSI and MACD momentum indicators sitting in negative configuration. However, this is balanced to a degree by an improving Stochastics. Monday’s intraday low at $63.60 is support now and the market has bounced from $64.40 too. Once the volatility of today’s EIA inventories is digested, the market is likely to settle for OPEC. There is resistance around $66.00 which protects $67.15 now.

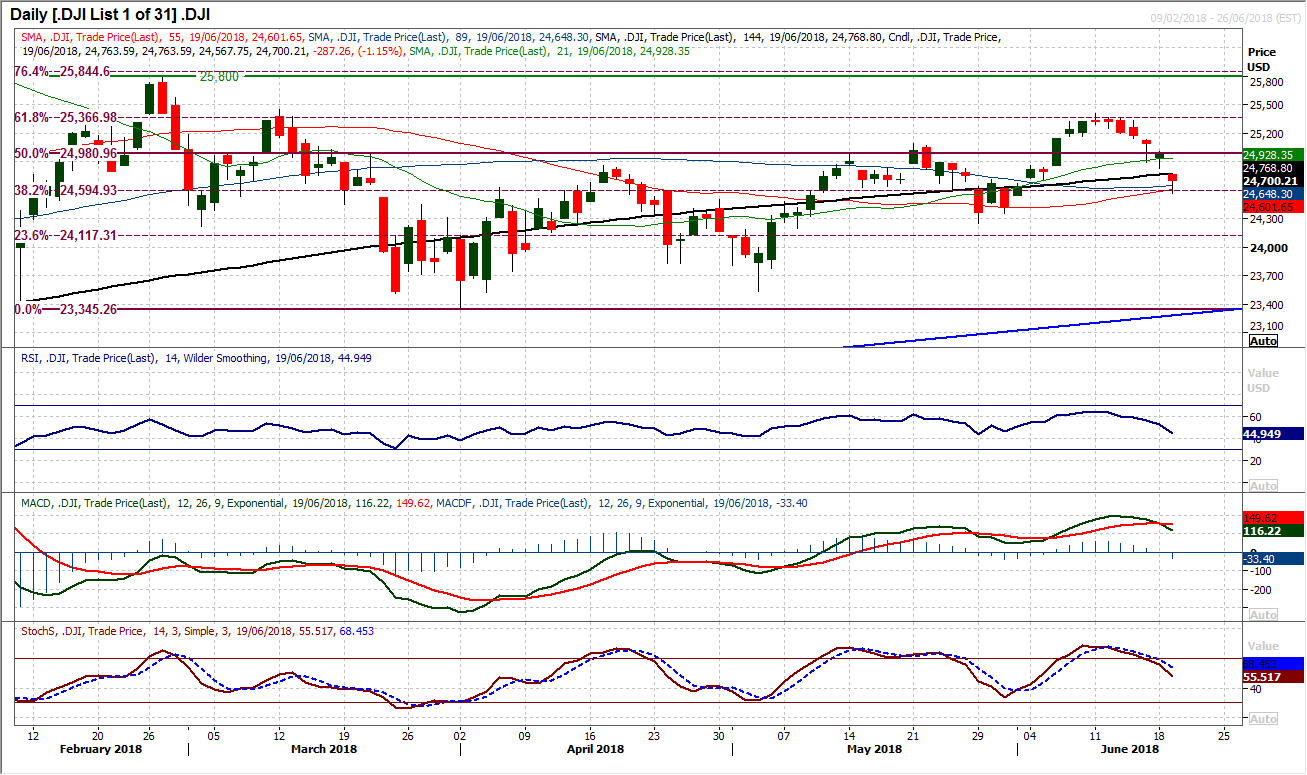

Dow Jones Industrial Average

Another significantly negative session has formed on the Dow as the move to the downside continues to accelerate lower, however interestingly, the market has again closed well off the lows of the day. The Fibonacci retracements of the 26,616/23,345 January to April bear run have been playing a significant role in the market in recent weeks, and turning back from 61.8% Fib at 25,367 last week, the market has gone quickly through 50% at 24,980 to interestingly bounce off around the 38.2% Fib at 24,595. This means that 24,595 is a potential consolidation zone for the Dow and could be where support now begins to form. However momentum indicators are now sharply deteriorating and with further downside potential too. The RSI has fallen quickly below 50, whilst the MACD lines have just crossed lower and the Stochastics are in sharp deterioration. A close decisively below 24,595 opens the 23.6% Fib level at 24,117 whilst the key May low at 24,248 is the next price support. However with yesterday’s intraday rebound, the 50% Fib at 24,980 becomes a potential target area should a rebound begin to gather momentum. There is also near term gap open a 24,825 that needs to be filled, whilst yesterday’s traded high at 24,765 is also resistance.

Author

Richard Perry

Independent Analyst