Unwarranted spread widening: Measurement issues (Part 2)

A lasting, unwarranted widening of sovereign spreads in the euro area would represent an excessive tightening of financial conditions and weigh on activity and demand. It would run into conflict with the objectives of the ECB in the context of its monetary policy normalisation. Spreads are influenced by various fundamental variables that are directly or indirectly related to debt sustainability issues. These tend to be slow-moving. Sovereign spreads also depend on the level of risk aversion, a variable that fluctuates a lot and which is influenced by global factors. This complicates the assessment of whether an observed spread widening is warranted or not.

The recent, significant widening of sovereign spreads in the euro area has triggered a renewed interest in the drivers of the difference between government bond yields in a given country and the yield on German government bonds of equivalent maturity. This interest is influenced by comments from ECB governing council members about the need to address unwarranted spread widening.

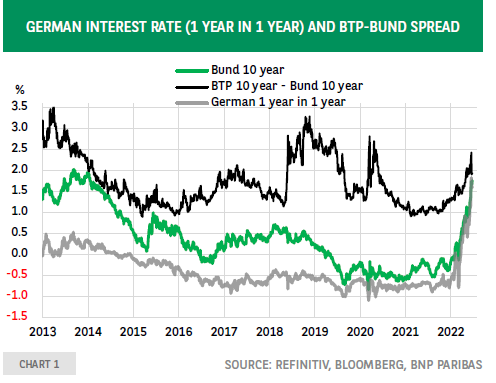

Putting a number on ‘unwarranted’ is a huge challenge considering that the sovereign spread depends on several variables. Moreover, the relationship – the beta in statistical terms – is time-varying. When Bund yields rise, the spread between Italian and German government bonds – the BTP-Bund spread – often widens but sometimes the opposite happens. Recently, the relationship has been positive and increasingly so1. The prospect of higher policy rates has played an important role. As shown in chart 1, the rise of the one-year forward rate of German government paper with a maturity of one year – a measure of monetary policy expectations – to a very large degree corresponds with the increase in 10-year Bund yields and both series are highly correlated with the rise in the BTP-Bund spread.

From a Finance theory perspective, one would indeed expect a positive beta between German rates and sovereign spreads. When the riskfree rate increases, a smaller exposure to riskier assets is needed to meet the target return. Macroeconomic theory also sees a positive relationship but for another reason: higher interest rates influence the debt sustainability parameters. Indeed, supposing that the debt ratio was initially stable, a permanent increase in the average borrowing cost would require, ceteris paribus, a reduction in the public sector primary deficit or a smaller primary surplus to keep the debt ratio stable2. Especially in case of a lasting, significant increase in interest rates, there may be concern that measures taken to stabilize the debt ratio would be slow or insufficient. Such concern would be reflected in a higher spread.

ECB research3 for the period 1999-2010 shows that in the euro area4 the public sector balance and the debt ratio play a statistically significant role in explaining the behaviour of sovereign spreads. The latter are positively correlated with financial risk, represented by the VIX index. Slower growth, an appreciation of the real exchange rate or a decline in bond market liquidity are associated with a widening of spreads. Credit ratings are significant but their influence is small. Importantly, during the European sovereign debt crisis, the sensitivity of bond prices to fundamentals increased. More recent research comes to similar conclusions on these variables and identifies the role of QEmeasures in influencing spreads.5 Jordi Paniaguaa et al6 emphasize that market sentiment and hence spreads also depend on differences in output growth between core and peripheral countries. This argues for macroeonomic policy coordination to enhance convergence within the Eurozone. Research by the IMF7 highlights the role of global risk aversion in the behaviour of spreads. Between July 2007 and September 2008 – a period that the authors call the financial crisis build-up – Germany and other core countries benefitted from flight-to-quality flows whereas risk aversion was weighing adversely on peripheral countries.

Spreads are influenced by slow-moving fundamental variables that are directly or indirectly related to debt sustainability issues but also by short-term fluctuations in risk aversion. This complicates the assessment of whether an observed spread widening is warranted or not.

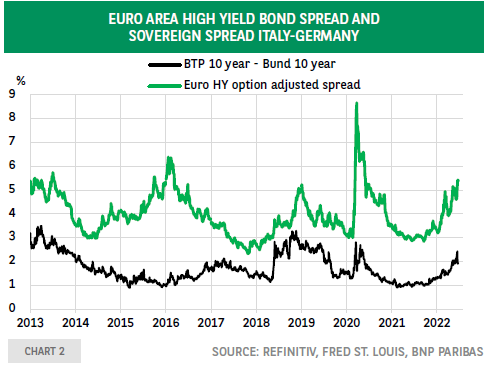

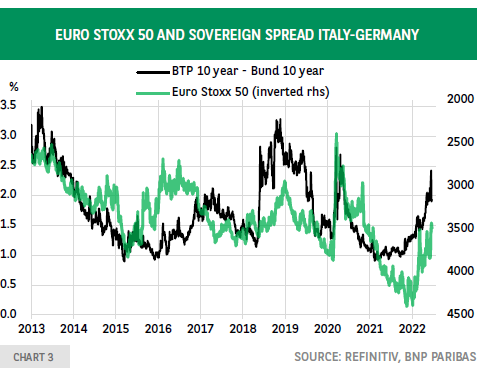

To illustrate the role of risk aversion, charts 2 and 3 compare the evolution of the BTP-Bund spread and, respectively, the euro high yield spread and the Euro Stoxx 50 equity index. Recently, the correlation between the sovereign spread and the high yield spread has been high and this also applies to the sovereign spread and equity market developments. This suggests that in recent months, risk aversion has increased, probably on the back of a prospect of higher ECB policy rates and a more uncertain growth outlook, in relation with elevated inflation and the war in Ukraine.

To conclude, spreads are influenced by various fundamental variables that are directly – public balance, debt – or indirectly economic growthrelated to debt sustainability issues. These tend to be slow-moving. Sovereign spreads also depend on the level of risk aversion, a variable that fluctuates a lot and which is influenced by global factors. This complicates the assessment of whether an observed spread widening is warranted: it may be unwarranted based on the (expected) evolution of the fundamentals whilst making sense in an environment of rising risk aversion.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.