The USD rout after a positive Fed is puzzling

Outlook:

Fed normalization and affirmation of a third hike this year is a Big Deal. Granted, the dollar rally on the news is on a far lesser scale than an event like Brexit, but it shouldn't flop after only one day, either.

The first thought on seeing the rates before dawn this morning was "What did Trump do?" The answer, of course, is he escalated the war of words with North Korean leader Kim Jun Un, calling him a madman after Un called him a mentally deranged dotard. North Korea is now threatening to drop an H-bomb in the Pacific, outside its own territory, which is some kind of provocation. Exports cited in the FT say it doesn't have the technical capability to do that. The US imposed another round of sanctions and China agreed to take no new banking customers from N. Korea and wind down current relationships. This is not something the US can police and we doubt it will really take place, but the gesture is US-supportive. The US hammer is cutting off Chinese banks from the US, something already done with one small Chi-nese bank, so not a small hammer.

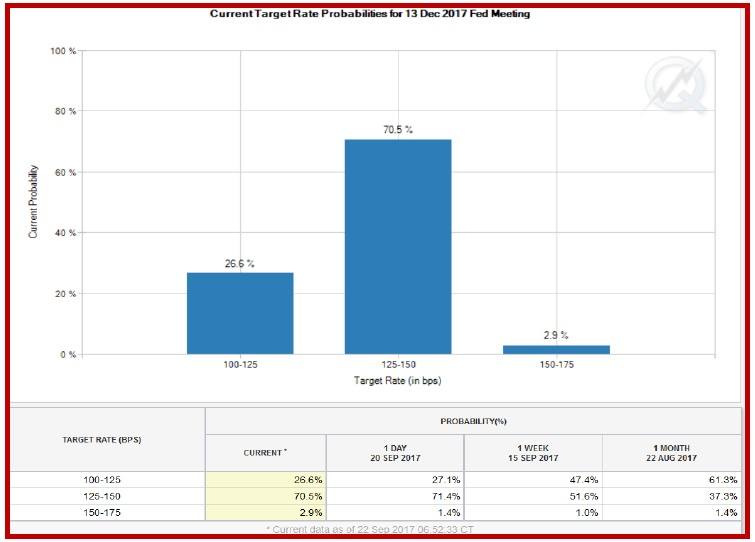

The alternating influence of the North Korean situation is hard to grasp. Sometimes it's a big deal that rattles markets, like this time, and other times equivalent noise fails to stir traders' imagination. What happened to that supportive rate hike talk? It's still in evidence. See the CME FedWatch tool below. The probability of the Dec hike is 70.5%, a little less than yesterday but far better than 37.3% a month ago.

This estimate is not likely to change after release of the manufacturing and services PMIs this morning (9:45 am ET), not usually a market-mover.

Coming up this weekend is another round of NAFTA talks in Ottawa, with the US displaying a new Commerce Dept report that shows US' falling share of sales of manufactured goods. The White House is using it to zoom in on "rules of origin." Parts and components made in (say) China make their way to Mexico or Canada and thence to the US under tariff-free NAFTA rules. The US wants to stop that and to hell with efficient supply chains.

The original goal of NAFTA was to benefit N. American workers, including US workers, so the stance is not factually wrong. The NYT example is that a car can have 37.5% of its components made outside NAFTA and still quality for preferential treatment. The US position is that this is a back door for for-eign products. The US components for goods made in Mexico and exported to the US was 26% in 1995 and 16% in 2011. US content in Canadian exports to the US was 21% and fell to 15% over the same period.

Commerce Secy Ross repeats "the point of a free-trade agreement is to advantage those within the agreement — not to help outsiders." Auto-makers and steel-makers, among others, will likely just pay the additional tariff if it's imposed—it's not terribly high, about 2.5%. We have been writing about the US dilemma for decades. Economists can prove that free trade benefits the most people. But a large percentage of those people may be outside the N. American continent and it's certainly true that Nafta is a back door. At a guess, the White House is going to win this one. Its rhetoric is deplorable but the political message is acceptable.

Bottom line, we are puzzled by the dollar rout coming so close on the heels of the positive message from the Fed. The economy is strong enough to take another hike and too-low inflation is a mystery, but normalization is an important goal. In the normal course of FX events, the rising interest rate ad-vantage "should" favor the dollar, whatever the temporary re-positioning may do to prices on an intraday basis. So, do we stick with the stronger dollar scenario or give up? The answer lies in what happens in the euro/dollar rate over the next two or three trading days. It may rise some more on Merkel on Sun-day evening, for example. But we think the cap lies around the recent high, say 1.2030. Nobody can name the timing, but by the middle of next week, barring war, the dollar could come creeping back. The operative word is "could." No guarantees.

In the meanwhile, remember Rocky's Rule—when in doubt, sell dollars. For what it's worth, we expect something of a military nature to occur sometime soon. Both of these leaders are vain, inept, unstable, and impulsive. In the US, we have "the generals" to keep Trump in check, so whatever military event occurs should be a lot less than outright war. This time.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 111.94 | LONG USD | 09/13/17 | WEAK | 110.05 | 1.72% |

| GBP/USD | 1.3557 | LONG GBP | 09/07/17 | STRONG | 1.3075 | 3.69% |

| EUR/USD | 1.1976 | LONG EURO | 06/28/17 | WEAK | 1.1218 | 6.76% |

| EUR/JPY | 134.05 | LONG EURO | 09/13/17 | STRONG | 131.76 | 1.74% |

| EUR/GBP | 0.8833 | SHORT EURO | 09/13/17 | WEAK | 0.9033 | 2.21% |

| USD/CHF | 0.9695 | SHORT USD | 08/10/17 | STRONG | 0.9655 | -0.41% |

| USD/CAD | 1.2274 | SHORT USD | 08/24/17 | WEAK | 1.2533 | 2.07% |

| NZD/USD | 0.7324 | LONG NZD | 09/13/17 | WEAK | 0.7282 | 0.58% |

| AUD/USD | 0.7966 | LONG AUD | 08/17/17 | WEAK | 0.7931 | 0.44% |

| AUD/JPY | 89.17 | LONG AUD | 09/05/17 | STRONG | 87.30 | 2.14% |

| USD/MXN | 17.8066 | LONG USD | 09/22/17 | NEW*STRONG | 17.8066 | 0.00% |

| USD/BRL | 3.1377 | WEAK | 09/05/17 | WEAK | 3.1409 | 0.10% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat