The RBA says the Australian economy looks fine – homeowners don’t think so

Won’t someone please think of householders?

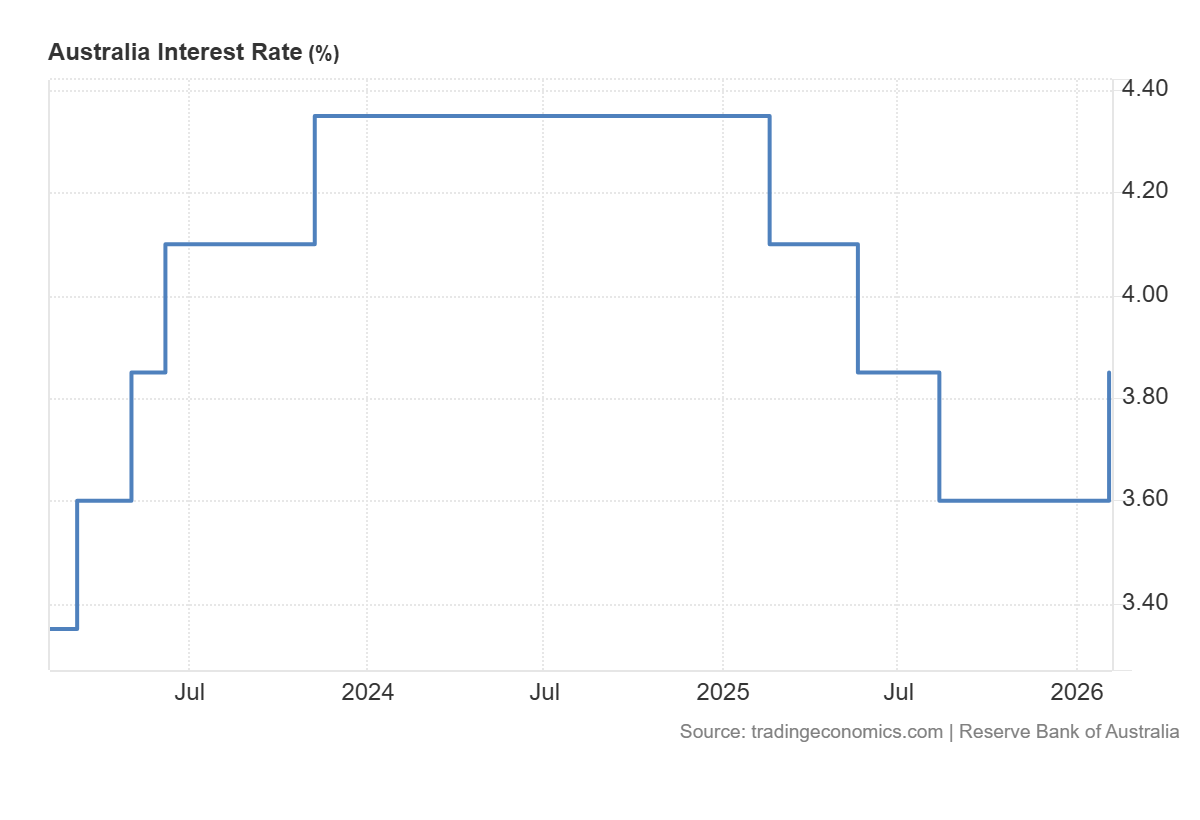

The Reserve Bank of Australia (RBA) just hiked interest rates, without the fact being a surprise to financial markets. Policymakers claimed increased inflation through the second half of 2025 was the catalyst behind the anticipated decision, but is it really all about inflation?

Interest rates are not just about banks offering a return for savings, and hence, helping restrict consumption and tame inflation. Interest rates are also about mortgages, and Australian families have been financially struggling for long enough.

Australian households suffer from rate hikes

According to realestate.com.au, since 2023, more than 30% of homeowners have said they were struggling to pay their loans. Currently, the total sits at 35%, consistent with previous January periods: 36% in 2025, 37% in 2024, and 34% in 2023. In 2022, however, the number was sitting at “only” 24%.

2022 was the year the RBA chose to start hiking interest rates. It’s easy to connect the dots.

Beyond inflation stubbornly staying above 3%, the Australian economy has been doing relatively well, with steady growth and low unemployment.

Yet those numbers clearly indicate the increasing disconnection between macroeconomic data and the common person's day-to-day life, which is basically assessed by how difficult it is to get to the end of the month. The truth is that, after a brief period of relief, the current debt-to-income ratio has severely strained household budgets.

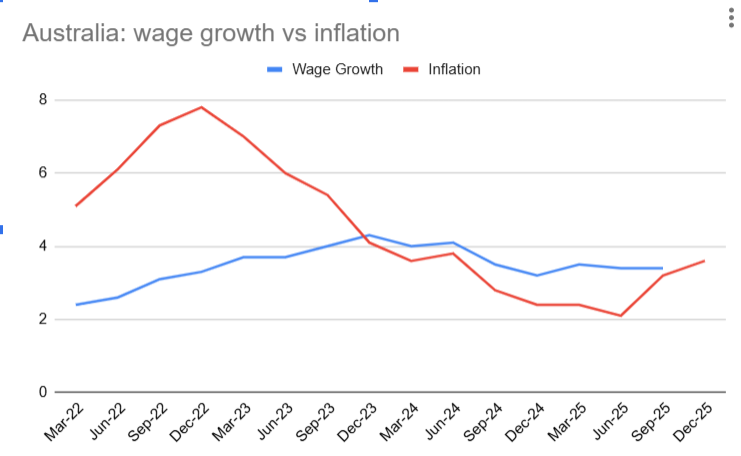

Wages grew faster than inflation between 2024 and late 2025. But recently inflation jumped to 3.8%, surpassing wage growth once again and triggering the RBA’s rate hike. The decision to hike rates is a bitter pill to swallow for households, which are now gearing up for renewed mortgage pressures.

According to Roy Morgan’s data, 1.4 million Australians were considered at risk of mortgage stress in August 2025. And that was before inflation spiked and before the RBA hiked rates. Say goodbye to wages growing faster than inflation, which, once passed on to mortgage holders, will leave mortgage rates around levels prevailing 13 years ago.

And this could be just the beginning after RBA Governor Michele Bullock has left the door open for further interest rate hikes if needed.

The outlook isn’t promising for Australian families

So, what would happen if the RBA follows the suspected pact of adding at least two more rate hikes this year?

Australian consumer confidence already deteriorated in February amid the rate hike, putting pressure on household finances, according to the latest Westpac survey. The same survey showed House Price Expectations rose to its highest in fifteen years.

Financial conditions for mortgage holders are not only expected to remain tight but also to worsen. Indeed, consumption should recede and hence, the inflation monster may be tamed.

But that’s far enough to be a long-term solution; instead, it looks more like a vicious cycle, one that the RBA has no intention to interrupt in the foreseeable future.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.