The stock market has reached new record highs

The markets went risk-on last week following better-than-expected economic data releases, as China virus fears eased. This week we will have a lot of Fed talk and another pretty important set of economic data releases. Let's take a look at the details.

The week behind

The corona virus fears eased last week, as financial markets reacted to better-than-expected economic data releases, U.S. quarterly corporate earnings. Overall, we've seen a risk-on trading action. The stock market has reached new record highs, but gold fluctuated following recent advances. Friday's Nonfarm Payrolls, Unemployment Rate were the most important economic data releases of the week. However, they were pretty much mixed and the markets were going sideways.

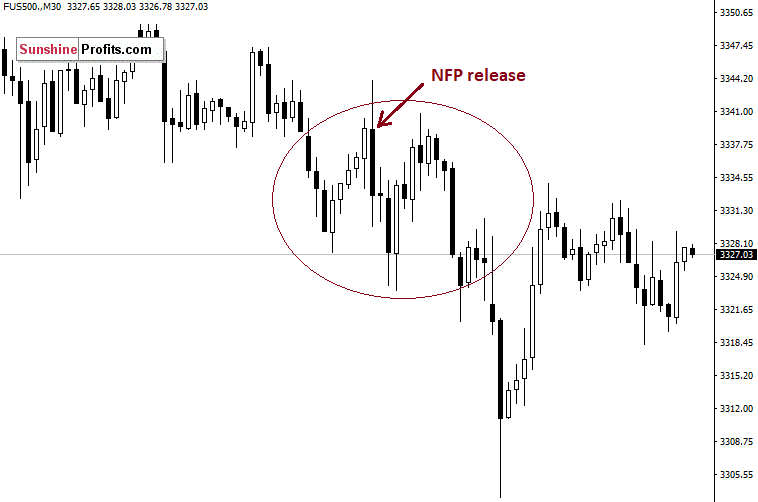

Let's take a look at 30-minute chart of the S&P 500 futures contract. The market was advancing following Friday's Nonfarm Payrolls release, but then it has quickly reversed lower. However, we didn't see that much of changes. And later in the day stocks were declining ahead of weekend's pause and some China virus uncertainty:

The week ahead

What about the coming week? We will have a lot of so-called Fed talk this week, including Tuesday's-Wednesday's Testimony from Powell. Then the markets will be focusing on two important economic data releases: Thursday's CPI and Friday's Retail Sales number. On Tuesday we will get the GDP number in the U.K. Investors will continue to react to quarterly earnings releases. Let's take a look at key highlights:

-

Friday's U.S. Retail Sales number will be the most important economic data release this week.

-

We will also have Jerome Powell's Testimony on Tuesday and Wednesday.

-

The U.S. Consumer Price Index will be released on Thursday.

-

Tuesday's U.K. GDP number release will be important for the British Pound currency pairs.

-

There will also be some quarterly corporate earnings releases this week.

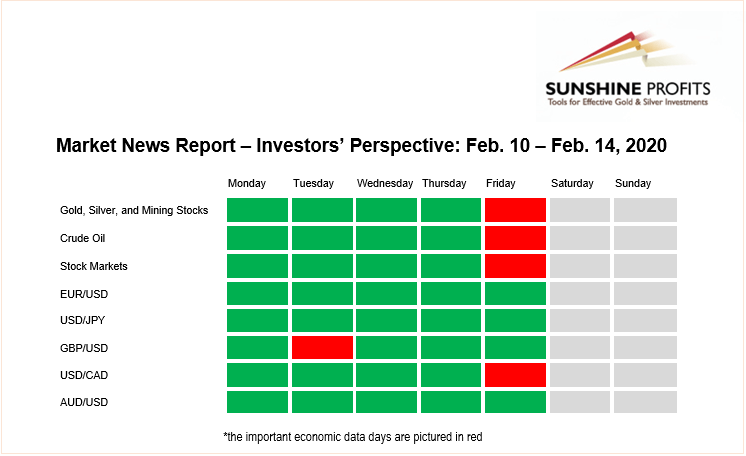

You will find this week's the key news releases below (EST time zone). For your convenience, we broken them down per market to which they are particularly important, so that you know what to pay extra attention to, if you have or plan to have positions in one of them. Moreover, we put the particularly important news in bold. This kind of news is what is more likely to trigger volatile movements. The news that are not in bold usually don't result in bigger intraday moves, so unless one is engaging in a particularly active form of day trading, it might be best to focus on the news that we put in bold. Of course, you are free to use the below indications as you see fit. As far as we are concerned, we are usually not engaging in any day trading during days with "bold" events on a given market. However, in case of more medium-term trades, we usually choose to be aware of the increased intraday volatility, but not change the currently opened position.

Our Market News Report consists of two different time-related perspectives. The investors' perspective is only suitable for the long-term investments. The single economic data releases rarely cause major outlook changes. Hence, we will only see a handful of bold markings every week. On the other hand, the traders' perspective is for traders and day-traders, because the assets' prices are likely to react on a single piece of economic data. So, there will be a lot more bold markings on potentially market-moving news every week.

Investors' Perspective

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Paul Rejczak

Sunshine Profits

Paul Rejczak is a stock market strategist who has been known for the quality of his technical and fundamental analysis since the late nineties.