The Partial US Government Shutdown: Much ado about politics

A quarter of the US government has been shuttered for a month and the economic impact is hard to discern.

There has been no shortage of political warnings from the Democrats and the Republicans and the media has been full of the dire consequences if the closure continues. This headline from Bloomberg on the 17th is typical," Wall Street Grown Antsy as Shutdown Threat to Stocks Intensifies."

But though the partial shutdown is now the longest on record, markets have been as blasé about the rhetoric emanating from DC as they have been about the financial and economic effects.

The shutdown began on December 22nd as the Democratic led House of Representatives, where all spending bills must originate, refused to include any funding for a barrier on parts of the country's southern border as demanded by President Trump. Trump in turn has said he will veto any bill without funding and the Republican controlled Senate has declined to take up any House bill that the President has promised to veto. All legislation must pass the House and Senate and be signed by the president to become law.

Because the Federal government is funded in a series of bills the status of any individual department, agency, division or program depends on whether the particular bill containing its funding was completed and signed by the President before the shutdown.

Nine of 15 federal agencies are affected in varying degrees by the budget dispute. Most of the agencies concerned are at least partially funded but as time passes more departments and divisions will run out of cash and either close or curtail services in order to continue functioning.

About 420,000 employees whose jobs are considered essential are working without pay and another 380,000 have been placed on temporary furlough. Among the workers considered mandatory are air-traffic controllers, food safety inspectors, prison guards, FBI agents, borders patrol agents and TSA workers. President Trump has said that all workers will receive whatever back pay is warranted after the closure ends.

Many federal agencies and programs including the Defense Department. Energy Department. Centers for Disease Control and Prevention and the National Institute of Health are completely funded through the end of the current fiscal year.

Others such as the Justice Department, Homeland Security, State Department, Housing and Urban Development , Transportation Department, Agriculture Department, Commerce and Interior Departments face partial or complete closure as their specific funding runs out.

Mail delivery continues as does the issuance of social security checks. Tax refunds from the Internal Revenue Service will be paid if the shutdown last through April 15th the filing deadline.

The Federal courts have begun restricting their operations with each court deciding on staffing and resources necessary for essential services under the Antideficiency Act. The Justice Department considers criminal litigation essential and it will continue but civil cases could be curtailed or postponed.

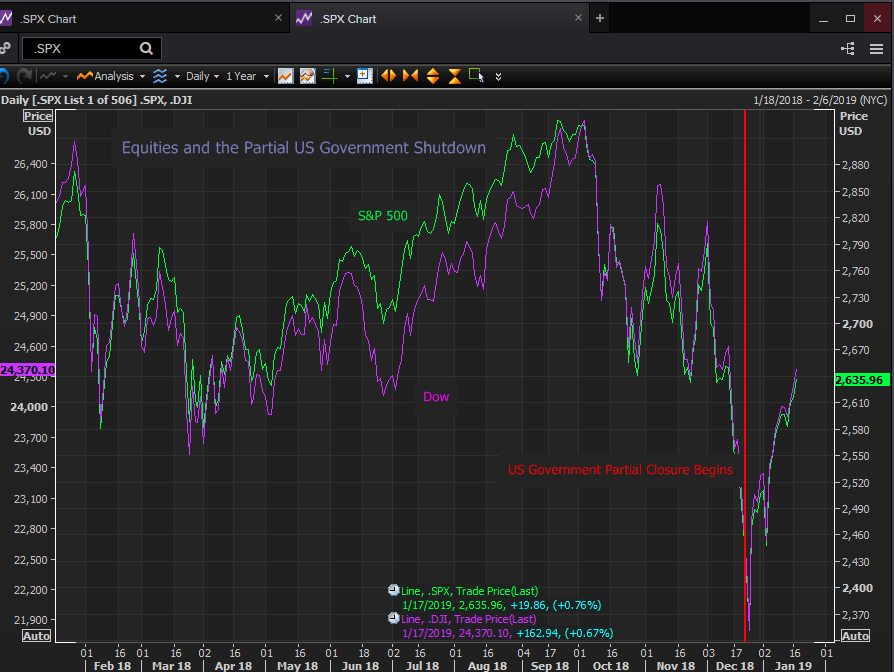

Turning from the government itself negative reactions from the markets are hard to find.

Equities have gained smartly throughout the shutdown. The S&P 500 closed on December 21st at 2,416.62. To the finish on Thursday January 17th it was up 9.07% at 2,635.96. The Dow has climbed 8.57% from 22,445.37 on the Friday before the closure started to 24,370.10 on the 17th. The Nasdaq Composite is up 11.86%.

The dollar is largely unchanged against the euro, 1.1367 to 1.1390, 1.7% lower versus the yen 111.21 to 109.32, and down 2.4% against the Canadian Dollar. The pound was the biggest winner against the dollar gaining 2.7% from December 21st to January 17th as the failure of Prime Minister May’s Brexit deal in Parliament is seen as boosting the softer exit alternatives or even no exit at all. The Dollar Index (DXY) lost 1% in the same period.

One of the chief market effects of the closure has be the postponement of some government economic statistics. Retail sales for December, durable goods, construction spending, housing starts and wholesale inventories for November and others are delayed.

The Federal Reserve will report on December industrial production and capacity utilization on Friday January 18th.

Of the few January statistics that have been reported, jobless claims for the week of January 12th fell 7,000 and the four –week moving average dropped to 220,750 from 221,750, both indicative of continuing labor market strength. The Philadelphia Fed Business Index for January came in at 17.0 up from 9.4 in December and well ahead of the 7.0 forecast. Though the employment sub-index fell to 9.6 from 19.1 in December it remains above the vast majority of post-recessions readings.

On Friday the 18th the University of Michigan will release its preliminary consumer sentiment index for January. If there is a consumer impact from the partial government closure this is where it should show up. The forecast is for a slight drop to 97.0 from 98.3 in December. The current conditions gauge is predicted to drop to 114.5 from 116.1 and the expectations measure to decline to 86.0 from 87.0.

All of these indexes are near the top of their ranges for the past decade. If they perform as expected, it would be a sign that consumer sentiment remains healthy and unaffected by the politics in Washington.

There have been no appreciable shift in Treasury yields. The 10-year Treasury rate closed at 2.79% on December 21st. On January 17th it finished at 2.75%.

For the people involved whose paychecks are delayed and for the politicians in Washington the shutdown is real and for some a hardship but for the overall economy there has been scant impact.

That could change as the closure lengthens and more units run out of funding on but with the bulk of the government operating the economic effect will likely remain small.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.