The market believes Trump

Outlook:

On the data front, the biggie this week is US inflation, which Bloomberg projects at a whopping 2.4% (from below 0.5% percent in Sept 2015).

CPI is not what the Fed watches but a data point like that will roil markets. The CPI report is on Wednesday, the first day of Fed chair Yellen testimony (to the Senate finance committee). The FT calls her the "outgoing" Fed chair, obviously believing Trump will dump her when her term is up next year. Assuming Yellen affirms a more robust economy and the three hikes expected this year, the testimony should be dollar-favorable, although she will no doubt decline to answer any specific questions about the dollar. Her comments will be examined thoroughly for any hint that the next hike will be closer than June, the current expectation, according to the CME FedWatch tool. The probability of March is tiny--about 13%.

If we get a giant CPI number like Bloomberg's 2.4%, all this chatter about two vs. three hikes and March vs. June will shift. And again we will hear about the Fed being "behind the curve." Buckle up your boots.

Offsetting any caution on the Fed's part is the prospect of fiscal stimulus. The key reason for the US yields to start rising again late last week was a possibly off-hand comment by Trump to the latest group of business executives he had summoned to the White House to bully. Trump said the tax plan is ahead of schedule. "Lowering the overall tax burden on American business is big league. And we're going to be announcing something I would say over the next two or three weeks that will be phenomenal in terms of tax and developing our aviation infrastructure."

The market believes Trump. Ostensibly serious newspapers like the WSJ call this a promised plan. "Before Mr. Trump's remarks, the 10-year yield had registered its largest three-day decline since June and was closing in on its lowest level since late November." For what it's worth, the 10-year breakeven rate (regular T notes minus TIPS) rose to 2.018% on Friday from 1.992% on Thursday.

For yields to reverse (and equities to hit new historic highs) on Trump's mention of a plan that does not exist is downright silly. Actually serious analysts warn that yes, keeping campaign promises (or appear-ing to try to keep them) is a goal, but there is Congress to contend with, not to mention the public. Now we are in a countdown to "two or three weeks" to get the actual plan. Trump lies so much—over two-thirds of the time--that it's possible the plan had not even been started at the time he spoke. There is a substantial risk that Trump doesn't appreciate he has set an actual deadline, another risk that he misses it, a third risk that he fails to consult Congress and comes up with something massively stupid, a fourth risk that Congress rejects his plan (a parallel to the recent court ruling on the travel ban), and a fifth risk that the public rejects the Trump ideas.

For the bond market to behave with confidence in upcoming tax reform—the first since 1986—in ridic-ulous. It's more than the triumph of hope over experience—it's delusional.

This goes to show financial markets are still at the mercy of Event Risk from the president. Oddly, de-spite displays of narcissistic personality disorder, including numerous lies, Trump did not disrupt the markets last week. He backed off from a trade war with both Japan and China, refrained from insulting any international leaders, and didn't propose any new dumb policies. Does this mean he is "pivoting" to a more sane and reasonable self-presentation or was he perhaps reined in? The press, mostly the NYT, keeps trying to discover who the rein-holder might be.

The Guardian wonders if Trump was a paper tiger all along. "The US leader has softened on a range of issues. Is he a bully who relents when challenged, or is he learning the limits of his power?" Trump seems to have backed down on NATO, accepting 1250 refugees from Australia, tearing up the Iran deal and even approval of unlimited Israeli settlements, now "not helpful."

Trump has another chance to be restrained today at a meeting with Canadian PM Trudeau, who will remind Trump that trade is roughly in balance and jobs attributable to sales to Canada number about nine million and in exactly the mid-west states Trump did the best. Canada wants to keep NAFTA. The FT notes that usually it's the US president that goes to Ottawa, but the Canadians were worried Trump would be offended by the inevitable protesters. Canada also prepared well ahead of time, speaking to Kushner and Bannon, among others.

Other signs of restraint include not lambasting the Bureau of Labor Statistics on the unemployment rate and not responding, so far, to the N. Korean provocation. Does a less bombastic demeanor mean Trump is changing his tune—only three weeks in—or was the bombast just a way to get elected? It's an im-portant question because a top promise was a trade and currency war. This was implied rather than promised, but nobody doubted that's what it meant. Then it appeared Trump and advisors didn't know whether they wanted a strong dollar to be macho or a weak one to push exports. Numerous editorials later, we still don't know. The Trumpies likely don't know themselves. Last week the newswires picked up a Huffington Post story that Trump called National Security Adviser Flynn at 3 a.m. to ask whether a strong dollar is good or bad for the economy. Flynn replied Trump should ask an economist instead.

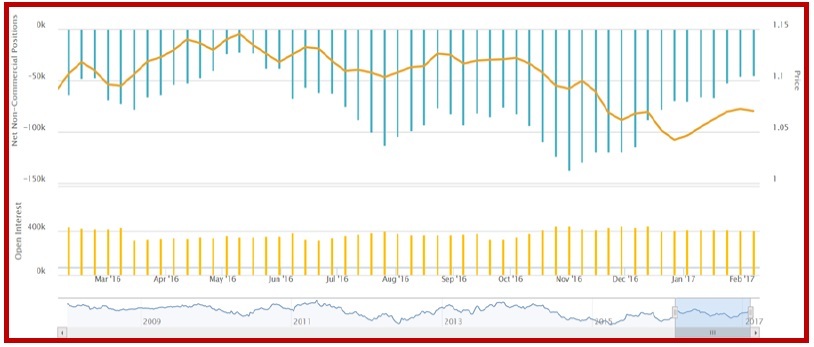

Here's the issue: if the market comes to perceive Trump never intended to start a currency war and it was just bombast to get elected—or alternatively, that Trump learned ranting about trade and currency wars is counter-productive--at some point they will become dollar buyers again. That point may be closer than we think. It may even be here. Reuters writes about the Commitments of Traders report that the dollar put in "the worst January performance in three decades." Trump may think he wants a weak dollar but he won't like the implications of his name being associated with "worst performance."

We can't say how much the prospect of a currency war damaged the dollar, but it's not zero. Last week Citibank chief economist Buiter said the Trump comments on FX are "hogwash" and "hot air." Buiter said "No matter how hard the Trump administration rattles the cage in an attempt to talk the dollar down, if the markets anticipate significant future stimulus in the U.S. and further tightening by the Fed, then whatever short-term wobbles there may be in the U.S. dollar, the dollar will only go one way rela-tive to most other currencies. And that's up." The Bloomberg version of the dollar index has lost steadi-ly for the past six weeks and about 50% since the election.

Accordingly, the Citi forecast is a stronger dollar across the board—to 124 against the yen and "beyond parity" against the euro. And yet the CFTC commitments of Traders report is not showing this senti-ment change. Reuters reports speculators cut their net-long dollar bets for the 5th week and to the lowest contract level since mid-October. "The value of the dollar's net long position totaled $17.07 bil-lion in the week ended Feb. 7, down from $18.47 billion the previous week.

Euro shorts were reduced. In the latest week, specs were short 44,951 contracts, less short than the week before at 45,713. Here is the net non-commercial (speculator) position in the euros futures con-tract (from Oanda). Notice the spike down on Nov 1 to 137,385 contracts short euros. This got cut back to 69,408 by Dec 27, and as of last week (Feb 7), shorts were 44,951, or one-third smaller than near election day. The short euro position is the smallest since May.

Bottom line—the market has not yet identified "currency war" as a false ruse. This may mean they are still clinging to the idea that the Trump trade war will drive the dollar down. Here's a strange question: for how long do the Trumpies have to maintain silence on the level of the dollar for the Citibank forecast of a dollar rally to resume? And to complicate matters, if the dollar automatically goes up on promises of tax reform and other fiscal stimulus, how will the Trumpies respond?

As a footnote—we find the COT report fundamentally unreadable. But in the absence of information on FX trading volumes, which is private information between the big banks and customers (including governments), the COT report is all we've got as a volume sentiment indicator. It's a spectacularly bad one, too. A dozen websites have sprung up over the past 15 years to explain how to re-jigger the data into something a normal human being can understand, usually a chart, mostly involving new software and usually for a fat fee. Using the COT as an indicator is a great deal of work—and even then, you might get the wrong deduction. That's what we think we have today.

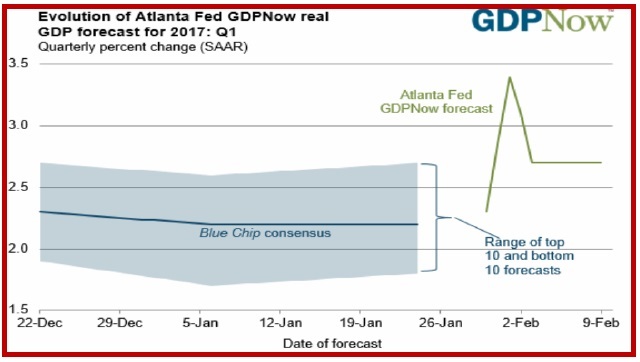

Presumably we need the economy to keep delivering good results to get a more hawkish Fed and the return of the Trump reflation trade. Just how strong is the US economy? The Atlanta Fed GDPNow has 2.7% for Q1 as of Feb 9, to be updated this Wednesday (Feb 15). In Q4, the Atlanta Fed consistently posted higher numbers than what we got in the end, the disappointing 1.9%. To be fair, almost no fore-caster got Q4 right. Here's the issue—the Atlanta Fed continues to judge the data more favorably than even the most optimistic of the Blue Chip forecasters.

We had to go back and refresh our memory of what, exactly, is the Blue Chip Economic Indicator set and the Blue Chip Financial Indicators. The Blue Chip publisher is a private company that publishes a monthly report based on surveys and interviews with business economists. The report covers GDP and 15 other factors, and costs about $1000 per year.

But nowhere could we find a track record, i.e, a forecast vs. the actual outcome on any of the 15 varia-bles. We have to admit, again, that economists' bad reputation is justified. In finance, you must report how your forecasts turned out. In economics, they shirk that duty. For shame.

Developments are coming. Event Risk is high. We guess the dollar will rise on both the Fed outlook and the Trump tax plan idea, but don't count on it.

Tidbit: One of the bigger retail FX brokers, FXCM, was put out of business and fined $7 million by the CFTC last week for cheating customers by having a financial stake in one of its dealers while claiming a "No Dealing Desk" platform, meaning without a conflict of interest with the customers. The conflict of interest was big—the WSJ reports FXCM received about $77 million in kickbacks, paid monthly, from the dealer from 2010 through 2014. The three FXCM principals are permanently banned from FX. The business is being sold to Gain Capital—ironically, a company FXCM tried to acquire a few years ago. Zerohedge, not always the most reliable or objective of reporters, "As for FXCM's thou-sands of retail clients, they may soon have to find more creative ways of losing their money than ‘investing' in 50x levered, central-bank dominated, HFT-infested currency markets whose only purpose these days seems to be to inflict the greater damage by stopping out the largest number of positions possible."

We don't buy that retail FX clients are suckers or even mostly HFT (high frequency traders), but it is true that if your stops are always getting hit, it may not because you set the wrong stop—it could be stop-hunting by your broker. To bring up our old complaint: futures are a better venue than spot for retail traders. Everybody gets the same bid and offer. Everybody gets the same open, high, low and close, and you can check that any particular price was met by consulting Time & Sales. Plus your trades are guaranteed by the exchange. The problem is that the CME futures contract, although now monthly instead of quarterly, is big—$125,000 in most contracts, more than the little guy can manage.

There is a mini contract but it lacks liquidity and has never been promoted. In the spot market, you can trade any old amount you choose, even $100 per contract.

We see conflicting highs and lows all the time in our spot trading advisory report. We use eSignal as an aggregator of retail brokerage quotes and quite often have a low or a high that hardly anyone else got. That's the retail brokers stop-hunting, or at least one of them. It will be interesting to see if discrepan-cies between our eSignal quotes and other big brokers disappear now that FXCM is gone.

Politics: The Washington Post, using wiretap transcripts leaked by the intelligence community for a total of 9 confirming sources, reports that National Security Advisor Flynn all but promised the Russian ambassador that Trump would lift the Obama sanctions against Russia for hacking the election and helping Trump win. He did this as a private citizen before the inauguration. This is illegal, albeit under the never-applied Logan Act of 1799. After several days of denials, Flynn admitted it on Friday, acknowledging that he had misled VP Pence and other insiders who were standing up for him. Anyone qualified to be national security advisor should have known the Russian ambassador was being wire-tapped, therefore Flynn is not qualified on three counts: doing it, lying about it (cover up), and not knowing about the wiretap. Besides, in 2015 Flynn was paid to sit near Putin at some kind of gala. How much and what for? The

list of factors pointing to Trump being in Putin's pocket is getting longer by the minute. Flynn's job is increasingly untenable.

The list of inappropriate, low-class and embarrassing behavior by Trump is growing longer, too, in-cluding holding on to Mr. Abe's handshake so long that Abe rolled his eyes when finally released. They are not disclosing the golf score although during the campaign, Trump's own golf club pro told the press that Trump routinely cheats. It's only the third week and the list of un-presidential behaviors is longer. Among the worst is moving individual stock prices like Nordstrom with tweets. Also longer is the list of lies. Last week it was that New Hampshire, one of the few states Trump lost, gave the election to Clinton because of bussing in thousands of illegal voters from Massachusetts. As with the 3-5 million illegals voting for Clinton, there is not one shred of evidence of Mass bussing. Politifact is keeping score—it has 19 from last week alone.

Trump's habit and practice of lying and making up data on the fly has the potential to be dangerous. The first international confrontation might be with North Korea. Is there a "deal" to be made with the unstable Un? There is no single best way to deal with Pyongyang, although Obama left a playbook of scenarios for Trump. Interestingly, PBS has been replaying documentaries about the October 1962 Cu-ban missile crisis. In the end, the US traded some nukes in Turkey for Soviet removal of nukes in Cuba, although the US action was secret at the time (and the Soviets, surprisingly, kept the secret).

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 113.73 | SHORT USD | 01/05/17 | WEAK | 115.93 | 0.11% |

| GBP/USD | 1.2516 | LONG GBP | 01/24/17 | WEAK | 1.2451 | 0.52% |

| EUR/USD | 1.0638 | LONG EURO | 01/10/17 | WEAK | 1.0587 | 0.05% |

| EUR/JPY | 120.99 | SHORT EURO | 02/03/17 | WEAK | 121.56 | 0.47% |

| EUR/GBP | 0.8499 | LONG EURO | 02/06/17 | WEAK | 0.8605 | -1.23% |

| USD/CHF | 1.0028 | SHORT USD | 01/05/17 | WEAK | 1.0113 | 0.04% |

| USD/CAD | 1.3098 | SHORT USD | 01/05/17 | WEAK | 1.3253 | 1.17% |

| NZD/USD | 0.7193 | LONG NZD | 01/10/17 | STRONG | 0.7014 | -0.11% |

| AUD/USD | 0.7674 | LONG AUD | 01/05/17 | WEAK | 0.7343 | 4.51% |

| AUD/JPY | 87.28 | LONG AUD | 10/06/16 | STRONG | 78.48 | -1.58% |

| USD/MXN | 20.3117 | SHORT USD | 01/31/17 | WEAK | 20.8108 | 2.40% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat