Subdued inflation should keep Fed on hold after next hike

Market Recap

|

Market Recap |

% |

Close Price |

|

XAUUSD |

0.90% |

1,292.12 |

|

EURUSD |

0.72% |

1.1822 |

|

NIKKEI 225 |

0.58% |

22,580 |

|

USDTRY |

0.97% |

3.9183 |

|

USDJPY |

1.09% |

111.22 |

|

DAX(Dec. 2017) |

1.17% |

13,009.00 |

Prices as of previous day instrument closing.

-

US equity indices closed mixed as the Nasdaq Composite rose 4.88 points or 0.07% to 6,887.36. DJIA slid 64.65 points or 0.27% to 23,526 and the S&P500 could not keep area 2,600 as the gauge lost 1.95 points or 0.08% to 2,597.08. The FOMC Minutes showed that while US labor market and economic activity as well has been rising at a solid rate, inflation remained soft. The next month FED funds are expected to be hiked to 125-150 bp, as the FEDWatch tool gives a 91.5% probability of a rate hike. However, if inflation does not take off, FED funds could stay between 125-150 bp until next June, as at the moment it seems the level with the highest probability, which is calculated from the FED Funds Futures prices.

-

In the FX market the Japanese Yen rallied again. USDJPY slid 1.09% to 111.22 and GBPJPY dropped to 148.18, down 0.45%. AUDJPY closed at 84.71, down 0.58% while NZDJPY lost ground as well and closed at 76.55, down 0.28%. EURUSD advanced versus the greenback thus Yen gained only 0.36% against the shared currency and EURJPY closed at 131.51.

-

Crude Oil WTI rallied +2.06% to 58.02 $/barrel while Brent rose to 63.33 $/barrel, up 1.20%; both contracts expire on January. Gold rose to 1,292.12 $/oz, up 0.89% and XAGUSD outperformed the shiny metal and closed at 17.15 $/oz, up 1.09%.

Charts of the day:

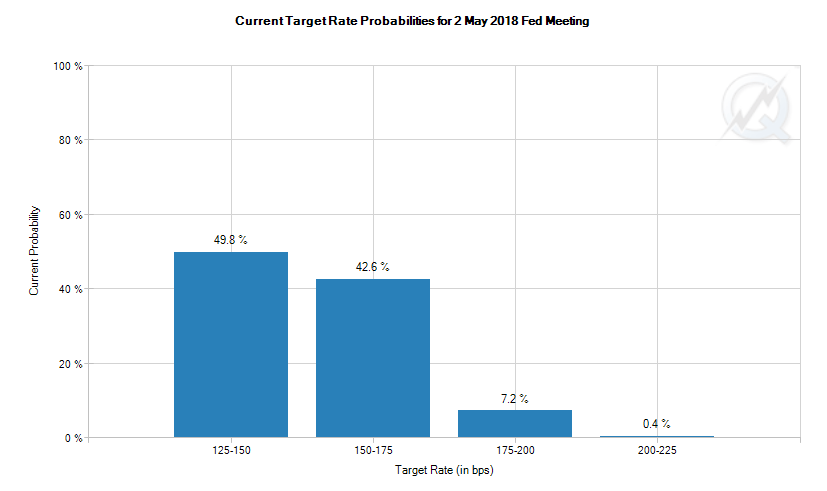

FED CME WatchTool

FED funds between 125-150 bp have the highest probability for the 2nd of May, 2018 FOMC Meeting. The probability is calculated from FED Funds Futures traded on the Chicago Mercantile Exchange. The economy in US could be at full or above full employment and GDP grow could exceed its potential output. The FOMC Minutes at page 8 mentioned that “Many participants observed, however, that continued low readings on inflation, which had occurred even as the labor market tightened, might reflect not only transitory factors, but also the influence of developments that could prove more persistent”.

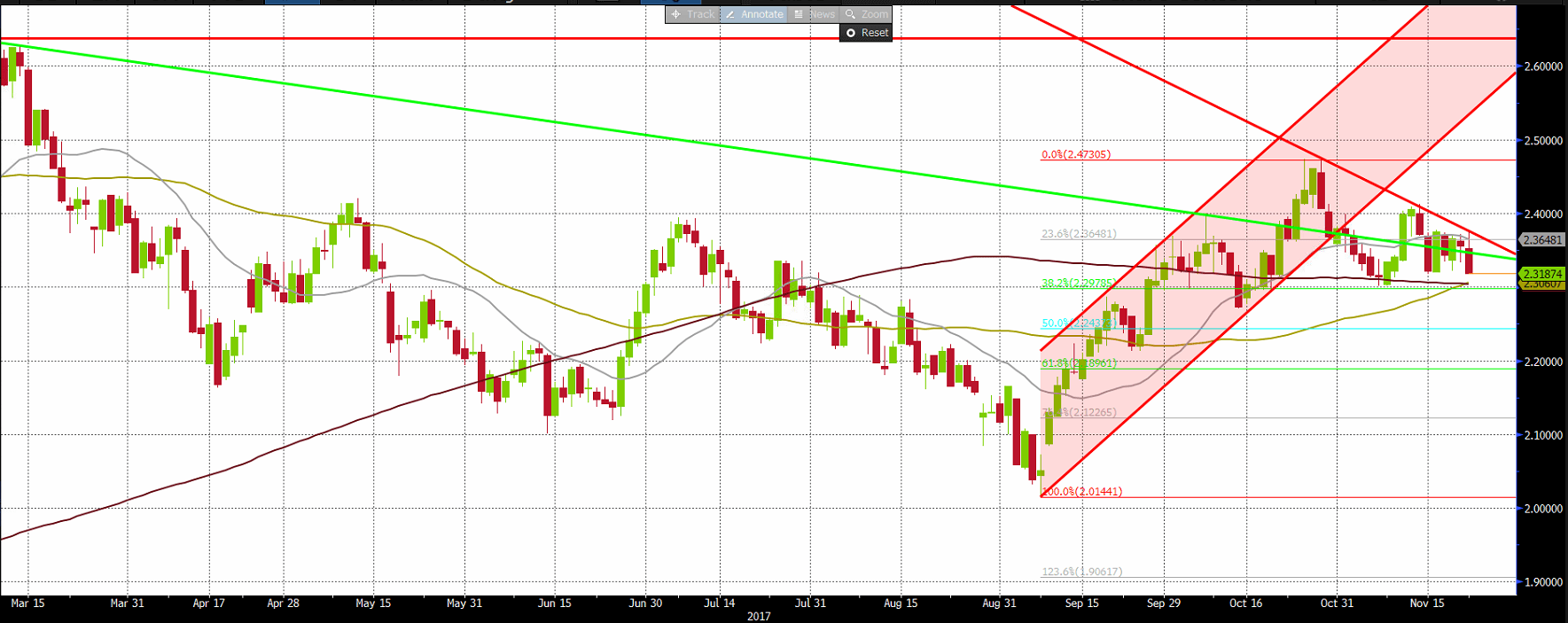

US 10 Year T-Note Yield

The yield is making lower highs after it broke its bullish channel and seems that it found support on its 200MA and 55MA as well. From a technical perspective, the width of the channel is equal to the distance between the 61.8% Fibonacci retracement (2.18%) and the broken lower side of the channel. In case of a breakout of the supply line, the yield could reach again area 2.47%. It seems quite difficult to see the 10 Year T-Note yield above its 2017 top 2.63% in the short term.

Economic Calendar

|

Thursday November 23, 2017 CET Time |

Forecast |

Previous | ||

|

USD |

Thanksgiving Day | |||

|

JPY |

Labor Thanksgiving Day | |||

|

09:00 |

EUR |

Markit France Manufacturing PMI – Preliminary (Nov) |

55.9 |

56.1 |

|

09:00 |

EUR |

Markit France Services PMI – Preliminary (Nov) |

57.0 |

57.3 |

|

09:30 |

EUR |

Markit Germany Manufacturing PMI – Preliminary (Nov) |

60.4 |

60.6 |

|

09:30 |

EUR |

Markit Germany Services PMI – Preliminary (Nov) |

55.0 |

54.7 |

|

09:35 |

EUR |

ECB’s Praet speaks | ||

|

10:00 |

EUR |

Markit Eurozone Manufacturing PMI – Preliminary (Nov) |

58.2 |

58.5 |

|

10:00 |

EUR |

Markit Eurozone Services PMI – Preliminary (Nov) |

55.2 |

55.0 |

|

10:30 |

GBP |

GDP – 2nd reading (3Q; QoQ) |

0.4% |

0.4% |

|

13:30 |

EUR |

ECB Account of the Monetary Policy Meeting | ||

|

19:15 |

EUR |

ECB’s Cœuré speaks | ||

US markets are closed today in observance of Thanksgiving Day and the Japanese are celebrating Labor Thanksgiving Day. Between 9 and 10:00 CET, Markit manufacturing and services PMI is released for the eurozone. Manufacturing activity is looking to broadly decline, while services are expected to remain solid. At 10:30 CET, the second reading of the UK’s GDP is released. The QoQ figure is forecasted to remain unchanged at 0.4%, the same with the YoY figure at 1.5%.

Speeches by ECB’s Praet and Cœuré are planned at 9:35 and 19:15 CET respectively but they are unlikely to be of significance as focus for the eurozone indices and euro crosses is on the accounts of the ECB’s monetary policy meeting at 13:30 CET. In the last ECB meeting, the QE program was extended until at least September at a reduced pace. Traders should merit attention to any comments by individual policy makers on the implementation of this scenario.

Technical Analysis

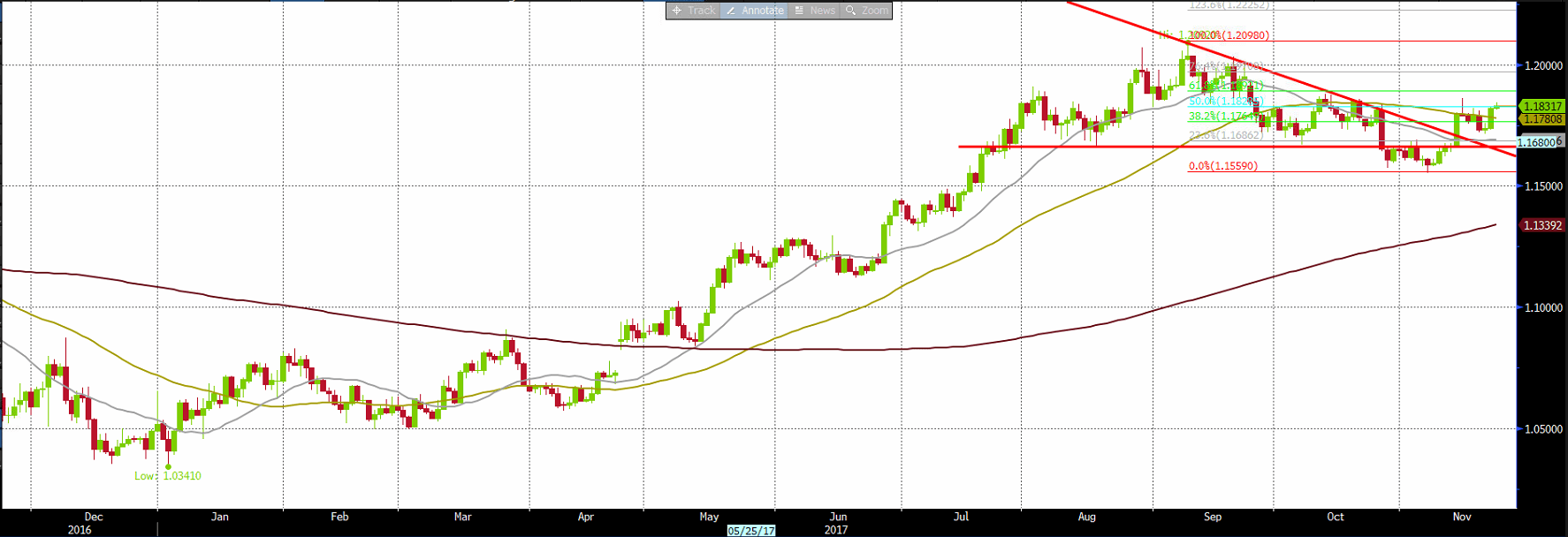

EURUSD (Daily timeframe)

EURUSD could test soon its last week high and rise above the 61.8% Fibonacci retracement from the selling wave triggered from its 2017 top. Above 1.1890 the pair could rise to 1.20 and then 1.2092. Beneath 1.1720 EURUSD could slide to 1.1660 and in case sellers will be in control the pair would test again 1.1590.

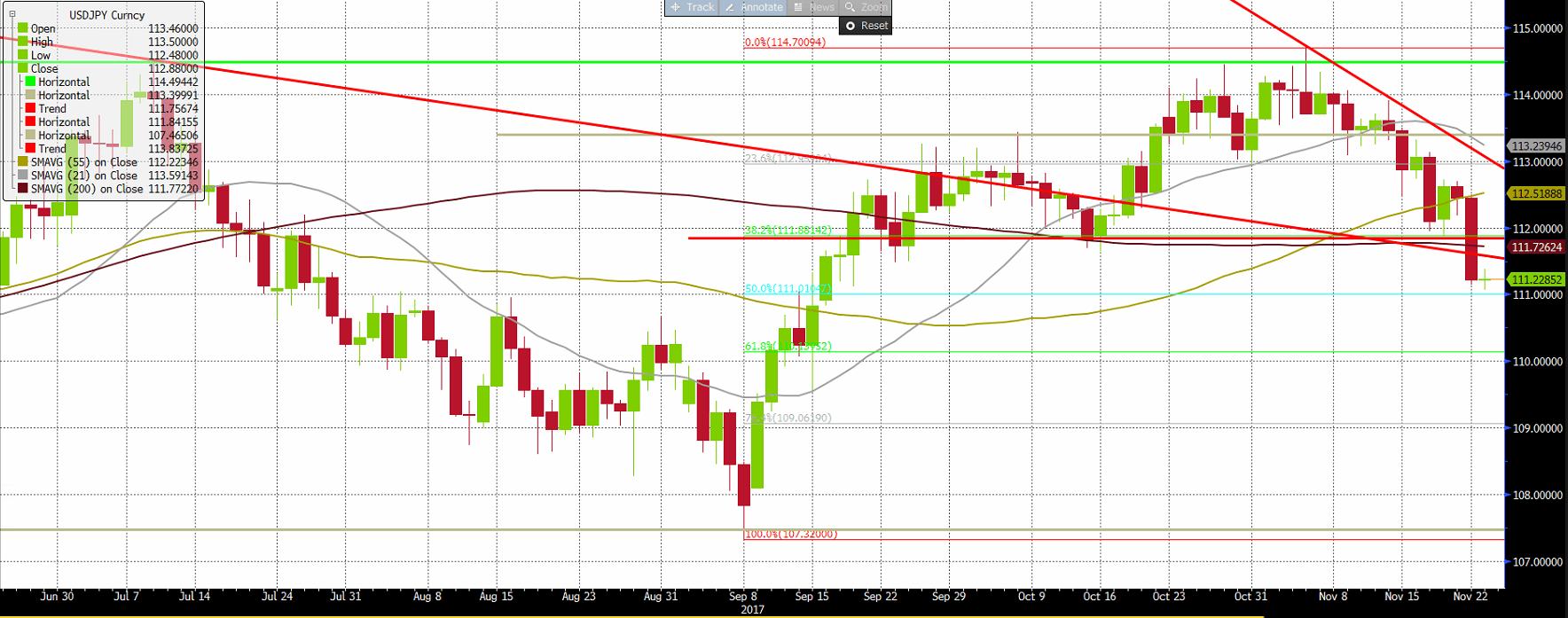

USDJPY (Daily timeframe)

USD/JPY broke the static support and could test soon area 111. Beneath this level there is the 61.8% Fibonacci retracement in area 110. If selling pressure would continue then USDJPY could make a 100% retracement. Only above 112 the pair could gain momentum and test its supply line. Above 113 USDJPY could test again area 114.70.

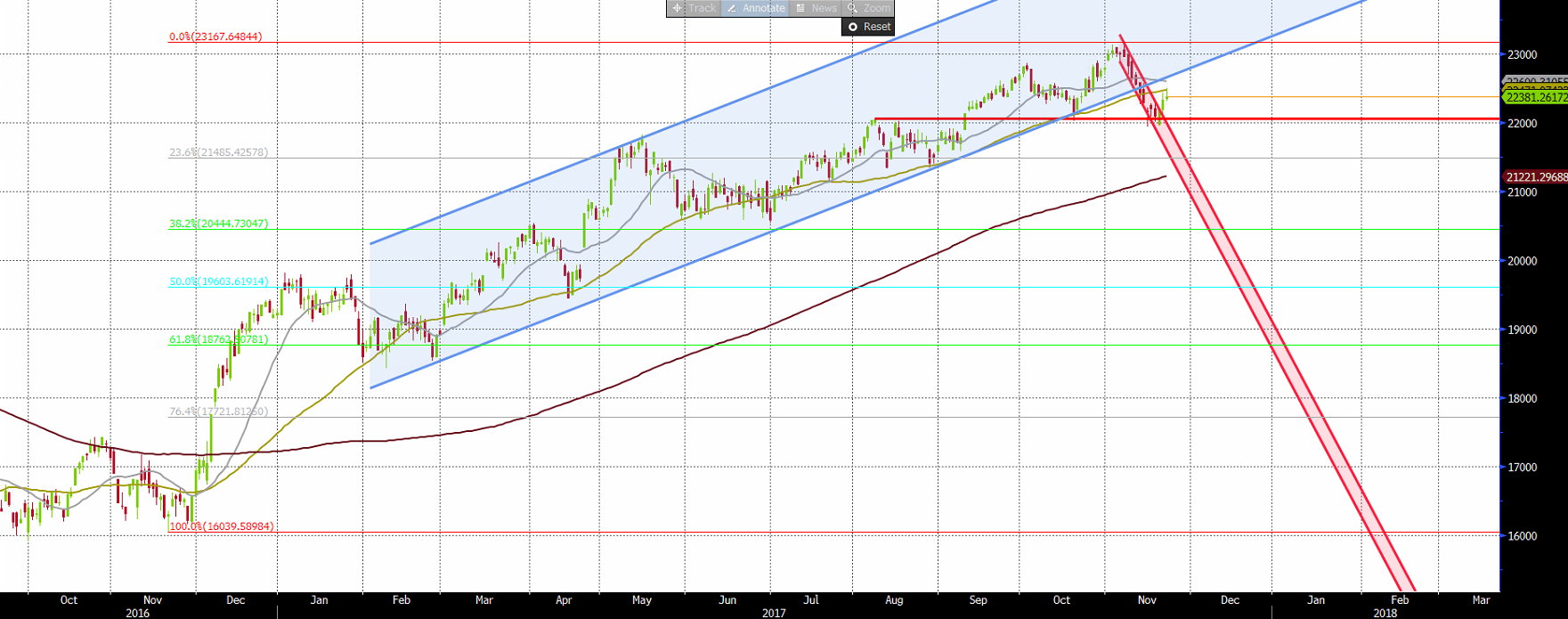

FTSEMIB (Daily timeframe)

The 55-day moving average held gains and the index pared some of its strength. FTSEMIB index will need to surpass 22460 and 22600 for strength to resume to 23000. 22000 remains key support in the near-term.

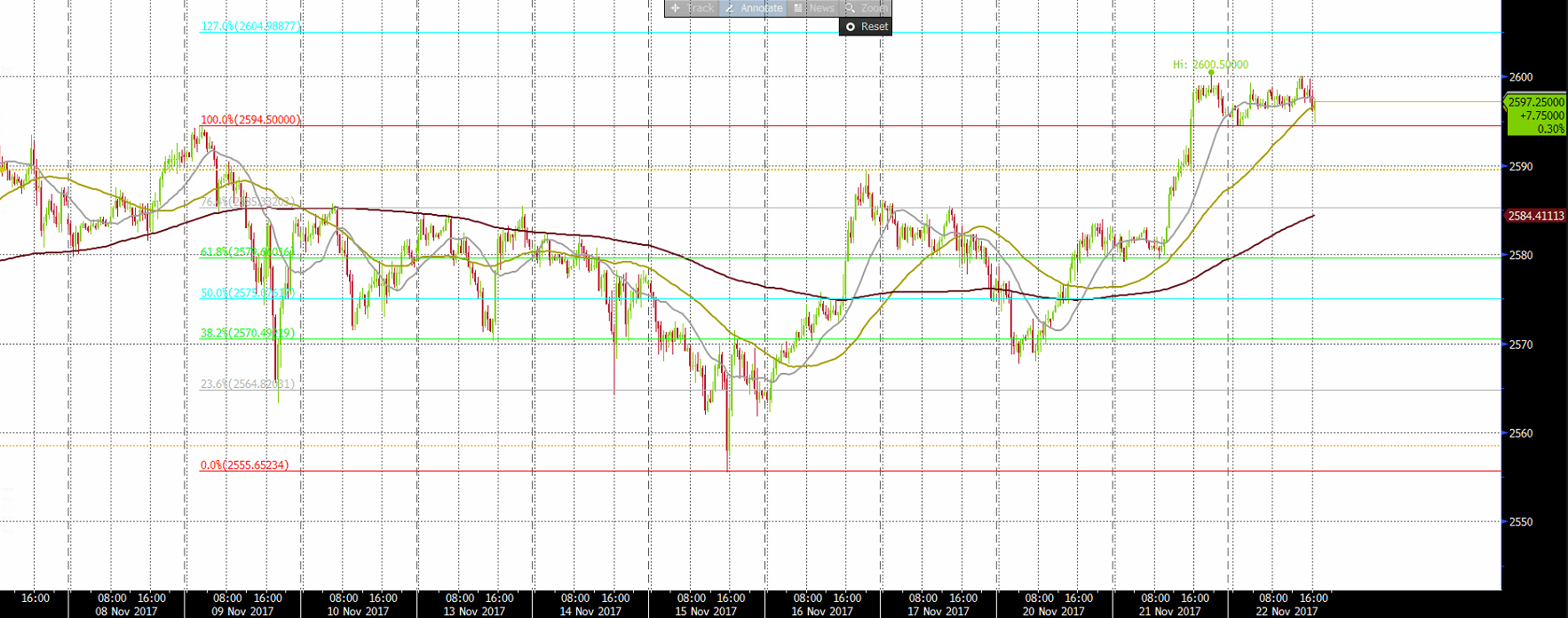

SPX500 (4-Hour timeframe)

SPX500 bounced once again on the 2594.50 level, which is a key support in the near-term from the previous all-time high earlier this month. Strength should resume and the price should test the all-time high 2600.50, with a break here to possibly accelerate gains to 2605, the 127% Fibonacci extension of the November previous high to low move. Key support remains at 2594.

Author

ALB Team

ALB Forex Trading

ALB Research Department is the research department of ALB Forex Trading Ltd.