Stockpiling Wood

I remember distinctly the moment when “retirement planning” took on a personal meaning to me.

I was kayaking with my wife along the Myakka River, which runs some 60 miles through the “Old Florida” prairies and wetlands of central Florida, just east of Sarasota.

Along with alligators, the river is teeming with history.

It’s believed Juan Ponce de León was the first European to explore the land, in the 1500s. The Seminole Indians inhabited the area in the 1700s and early 1800s. And then cattle farmers moved in on the fertile region in the late 1800s.

Somewhere along our paddle, we stopped at the abandoned camp of one of the region’s early settlers. All I remember seeing as we pulled our kayaks to shore was a small wooden structure, slightly bigger than an outhouse, and, nearby, an enormous stockpile of firewood.

The pile of wood had to have been 100-times larger than the house itself – it was stunning!

I asked our guide, “what’s with all the wood?”

He quickly answered, “that’s an old-school retirement plan right there.”

That’s when the lightbulb went off for me.

You see… retirement planning is about self-sufficiency!

Whoever settled that camp along the Myakka River hundreds of years ago…

Nobody gave him a pension-and-gold-watch retirement. He didn’t have an employer-match on his tax-advantaged 401(k). Social security… “what’s that?”

According to our guide, this early settler felled trees and split fire wood every single day of his life.

He knew that if he didn’t do it… no one else would do it for him. And further, he knew if he ever got old or injured… he wouldn’t be able to produce firewood… and if he didn’t have enough stockpiled by then… he’d die.

A bit morbid, yes – but honest. He didn’t pretend. He didn’t delude himself into thinking that someone would have his back one day. He just got down to business.

Thankfully, the retirement planning for modern Americans is not as do or die. But sadly, most hopeful retirees haven’t stockpiled nearly enough wood.

Consider the stats…

“Thirty-six percent of American workers age 55 to 64 say they have less than $25,000 in retirement savings.” — Employee Benefit Research Institute

“Fifty-one percent of households are at risk of not having enough savings to maintain their standard of living after retirement.” — The Center for Retirement Research at Boston College

“Sixty-six percent of Americans said their top financial concern was not having enough money for retirement.” — Gallup poll

But beyond the research and statistics, I’ve seen this retirement dilemma first hand. I was working as an advisor for a Fortune 500 financial planning firm throughout the 2008 market crash.

Each week, I met with dozens of families, all of whom were trying to figure out how to get to age 65 with a sufficiently large nest egg.

Most of them were looking to “buy and hold” to get them there. So, suffice to say, the 50%-plus drawdown in their buy-and-hold portfolios was threatening – particularly for those who were just a few years from that golden 65th birthday.

It was saddening to watch. These were good people with good intentions… and they couldn’t figure out how to afford retirement.

Simply put: “buy and hold” let them down!

It’s tragic, really.

Alongside the move from pensions to 401(k)s, the onus of retirement planning was shifted back to the individual. And the only best advice they’ve been able to get for much of this time has been “just buy… and hold.”

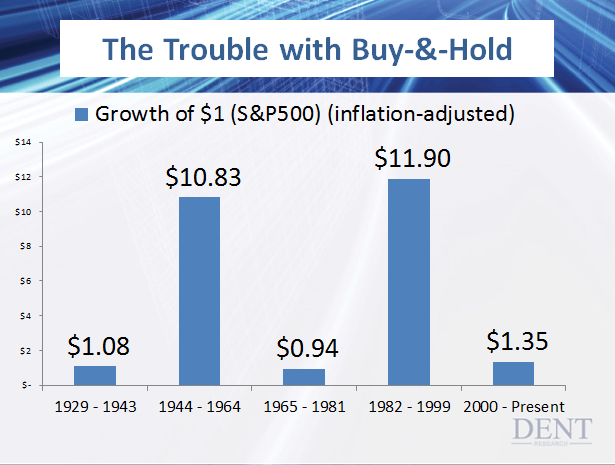

Sure, buy-and-hold has worked for some investors, but it’s sorely disappointed others. Consider this chart, which I first shared with attendees of our 2016 Irrational Economic Summit. It shows the total return of buy-and-hold for distinct periods of time.

As you can see,buy-and-hold turned $1 into $11.90 between 1982 and 1999. But between 2000 and present day, buy-and-hold has done little for retirement savers – turning $1 into a measly $1.35.

I’m sure you know by now that we’re not big fans of buy-and-hold here at Dent Research.

Each of us – Harry, Rodney, Lance, Charles, John and myself – have rejected the spoon-fed advice of buy-and-hold… and we’ve each found our own ways to grow our wealth and plan for retirement.

Me…?

I’m a trend-following systems guy – so that’s the type of firewood I’ve been stockpiling for my own retirement.

Harry…?

He’s a big thinker and risk-taker – so he’s found tremendous success building his retirement nest egg through some unconventional means, as he explained here last week.

And Charles…?

He’s a stodgy conservative – so he’s found ways to get automatic checks every month! He’ll be sharing the details with you later this week, so don’t miss it.

The great thing about investing is there are many ways to “win” at it. What’s right for me isn’t always going to be right for you. And that’s OK.

You’ve just got to figure out what works for you… and then get to chopping that firewood! Or collecting those automatic checks…

Author

Dent Research Team of Analysts

Dent Research