Still more inflation expectations nonsense in the latest Fed minutes

Let's review the latest FOMC Minutes including Fed discussion of inflation expectations.

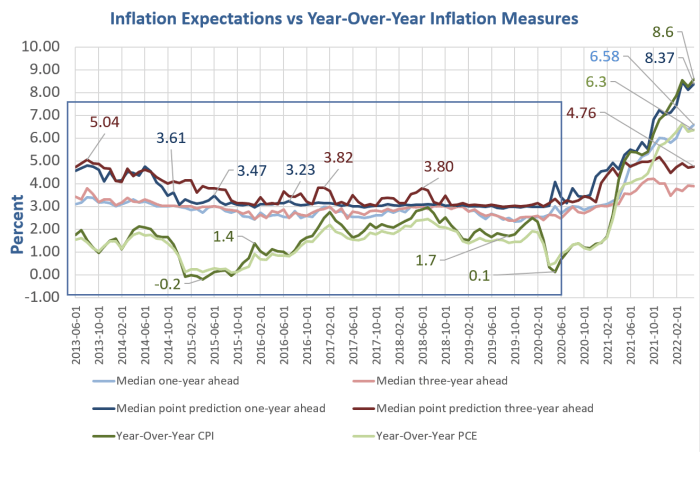

Inflation expectations from NY Fed Survey, CPI and PCE data vis St. Louis Fed, Chart by Mish

I discuss the lead chart after a review of the minutes of the latest FOMC Meeting.

Inflation risk skewed to the upside

Today, the Fed released Minutes of the June 14-15 FOMC Meeting, emphasis mine.

In their discussion of risks, participants emphasized that they were highly attentive to inflation risks and were closely monitoring developments regarding both inflation and inflation expectations. Most agreed that risks to inflation were skewed to the upside and cited several such risks, including those associated with ongoing supply bottlenecks and rising energy and commodity prices. Participants judged that uncertainty about economic growth over the next couple of years was elevated. In that context, a couple of them noted that GDP and gross domestic income had been giving conflicting signals recently regarding the pace of economic growth, making it challenging to determine the economy’s underlying momentum. Most participants assessed that the risks to the outlook for economic growth were skewed to the downside.

In their consideration of the appropriate stance of monetary policy, participants concurred that the labor market was very tight, inflation was well above the Committee’s 2 percent inflation objective, and the near-term inflation outlook had deteriorated since the time of the May meeting. Against this backdrop, almost all participants agreed that it was appropriate to raise the target range for the federal funds rate 75 basis points at this meeting.

At the current juncture, with inflation remaining well above the Committee’s objective, participants remarked that moving to a restrictive stance of policy was required to meet the Committee’s legislative mandate to promote maximum employment and price stability. In addition, such a stance would be appropriate from a risk management perspective because it would put the Committee in a better position to implement more restrictive policy if inflation came in higher than expected.

Inflation expectations and yapping as a tool

Measures of inflation expectations derived from surveys of professional forecasters and of consumers generally suggested that inflation was expected to remain high in the short run but then fall back toward levels consistent with a longer-run rate of 2 percent.

Participants observed that some measures of inflation expectations had moved up recently, including the staff index of common inflation expectations and the expectations of inflation over the next 5 to 10 years provided in the Michigan survey.

Many participants judged that a significant risk now facing the Committee was that elevated inflation could become entrenched if the public began to question the resolve of the Committee to adjust the stance of policy as warranted.

Members judged that, with high and widespread inflation pressures and some measures of longer-term inflation expectations moving up somewhat, it would be appropriate for the post meeting statement to note that the Committee was strongly committed to returning inflation to its 2 percent objective.

Hello Jerome Powell

Hello Jerome Powell, please explain the lead chart.

If inflation expectations mattered at all, how the hell did the Fed fail to reach its 2 percent target for a decade?

Not only were expectations above 3 percent between 2013 and 2020, the Fed was actively trying, via round after round of near-endless QE and constant yapping about inflation expectations.

Flashback June 16, 2021

Please recall my June 16, 2021 post Fed Will Foolishly Continue QE Purchases in Search of Higher Inflation

The post was in regards to the FOMC meeting just over a year ago.

June 2021 FOMC statement key paragraph

- The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With inflation having run persistently below this longer-run goal, the Committee will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer‑term inflation expectations remain well anchored at 2 percent. The Committee expects to maintain an accommodative stance of monetary policy until these outcomes are achieved.

- The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.

- In addition, the Federal Reserve will continue to increase its holdings of Treasury securities by at least $80 billion per month and of agency mortgage‑backed securities by at least $40 billion per month until substantial further progress has been made toward the Committee's maximum employment and price stability goals.

How clueless can you get?

Please check out my comments at the time.

Group-Think Silliness Well Anchored

I bolded the note about inflation expectations because they are totally meaningless.

The Fed believes all kinds of group-think silliness, and inflation expectations are at the top of the list.

What are the Fed and Congress going to do next with stimulus wearing off and banks choking on the Fed's QE already?

Looking ahead, the fourth quarter and 2022 GDP and will be much weaker than most expect.

The irony in the Fed's actions is they are indeed increasing inflation, but only in the most unproductive, yet uncounted ways. There's plenty of inflation now, just not as they measure it.

Fed study on inflation expectations

Please consider Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?) by Jeremy B. Rudd at the Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board.

Serious Policy Errors

Economists and economic policymakers believe that households’ and firms’ expectations of future inflation are a key determinant of actual inflation. A review of the relevant theoretical and empirical literature suggests that this belief rests on extremely shaky foundations, and a case is made that adhering to it uncritically could easily lead to serious policy errors.

The Fed does not believe its own studies!

And yes, we have policy error upon policy error with bubbles and crashes as poof.

Hello Fed

On April 11, I commented Hello Fed, Inflation Expectations Are Unglued, No Longer Well Anchored

The New York Fed survey already shows inflation expectations are not anchored.

Even the three-year median point projection is 4.88%, well over the Fed's target rate of 2.00%.

Powell was shocked that the University of Michigan survey showed the same thing.

I commented It's a good thing inflation expectations are not self-fulfilling because expectations are now unglued.

The asininity of inflation expectations, once again by Powell and the Fed

Also consider my June 25, 2022 post The Asininity of Inflation Expectations, Once Again By Powell and the Fed

I provided numerous real-world examples as to why inflation expectations are nonsense.

But the Fed won't listen to me. Heck it will not even believe its own well-researched study.

Instead, these group-think blockheads will believe what they have been trained to believe. Any data to the contrary is immediately discarded.

Historical perspective on CPI deflations: How damaging are they?

And please recall my May 3, 2020 post Historical Perspective on CPI Deflations: How Damaging are They?

The Bank of International Settlements (BIS) did a study in 2015. Here are the key snips.

Concerns about deflation – falling prices of goods and services – are rooted in the view that it is very costly. We test the historical link between output growth and deflation in a sample covering 140 years for up to 38 economies. The evidence suggests that this link is weak and derives largely from the Great Depression. But we find a stronger link between output growth and asset price deflations, particularly during postwar property price deflations. We fail to uncover evidence that high debt has so far raised the cost of goods and services price deflations, in so-called debt deflations. The most damaging interaction appears to be between property price deflations and private debt.

Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive.

The Fed tried for a decade to produce inflation, missing the asset bubble inflation it created the whole time. Then the Fed missed the very conditions that would cause CPI inflation (free money plus supply chain shocks).

Now it risks a policy error in the opposite direction.

Powell: "We understand better how little we understand about inflation”

On June 29, 2022, Powell admitted "We understand better how little we understand about inflation”

Gee, who couldda thunk?

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc

Mike “Mish” Shedlock is a registered investment advisor for SitkaPacific Capital Management.