Should forex traders watch governments and ignore central banks? Examining USD, EUR, GBP

- Fiscal policy is having a growing impact on currency movements.

- Debt has become a non-issue for policymakers in most jurisdictions.

- Central banks have limited impact amid diminishing ammunition for the time being.

More debt, more value? Currencies are moving not on higher interest rates but rather in response to growing government liabilities. Investors are buying up currencies of governments that spend while disregarding debt. While piling obligations may come home to roost – that is unlikely to happen anytime soon.

UK: Paving a road, not fixing the roof

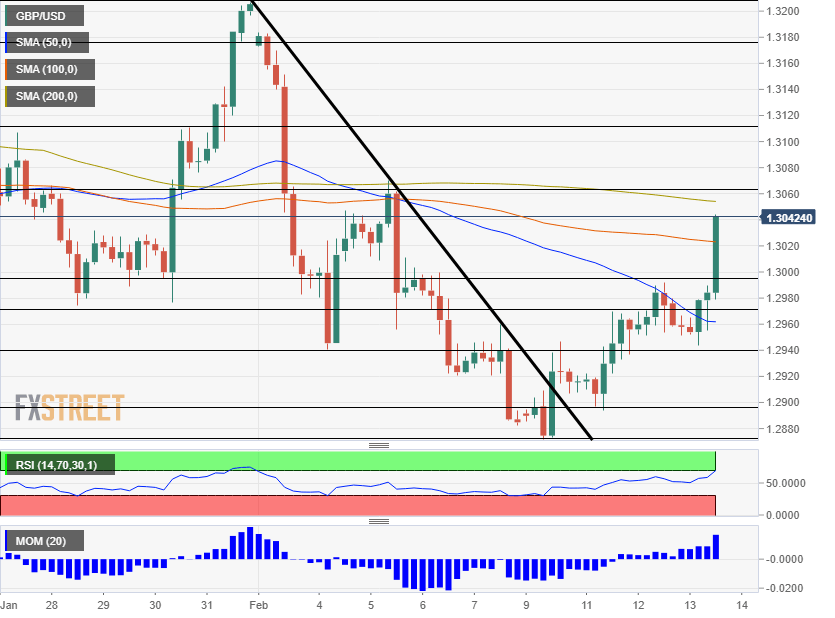

The latest "reshuffle rally" in the pound proves the point but is only the latest case. Prime Minister Boris Johnson forced out his fiscally-prudent Chancellor of the Exchequer Sajid Javid with lesser-known Rishi Sunak in what is seen as a power grab. The new team is on course to loosen the purse strings – abandoning deficit and debt rules set by Javid and pushing infrastructure spending.

GBP/USD reshuffle rally

First, it is set to boost the economy through both the potential public splurge and by creating confidence that may encourage private-sector spending. The underlying currency has room to rise alongside stronger growth.

Secondly, it alleviates pressure from the Bank of England to provide additional monetary accommodation. Even if inflation fails to rise, the BOE will be under no pressure an in no rush to cut interest rates or expand its bond-buying scheme. Higher rates also underpin the pound.

Austerity – enacted by former PM David Cameron and his Chancellor George Osborne – seems to belong to a different era. The previous pair at Downing Street aimed to "fix the roof while the sun is shining" while Johnson wants to get things done – Brexit, trains, anything – regardless of costs.

Dollar cheers ballooning US debt

In the US, concerns about the deficit and the debt seem to belong to the past. Republicans – who blasted then-President Barrack Obama for growing America's liabilities after the debt crisis – are now overseeing a ballooning national debt. The mix of spending increases – supported by Democrats – and President Donald Trump's massive tax cuts, are taking their toll.

The US budget deficit has jumped by $389.2 billion in the first four months of fiscal 2020 – October 2019 through January 2020. That is an increase of 25% from the first third of fiscal 2019. On a 12-month basis, the gap between income and expenses topped $1 trillion with total American debt topping $23 billion.

The debt-to-GDP ratio has topped 100% and continues rising while the economy is nearing full employment – contrary to the perceived wisdom of saving money when the economy is high.

And similar to the pound, the US dollar is on the rise. The greenback is hit multi-month highs against the yen, multi-year lows against the euro, and decade peaks against the Australian dollar.

-637172876935099046.png)

Euro falls as German "Schuld" weighs

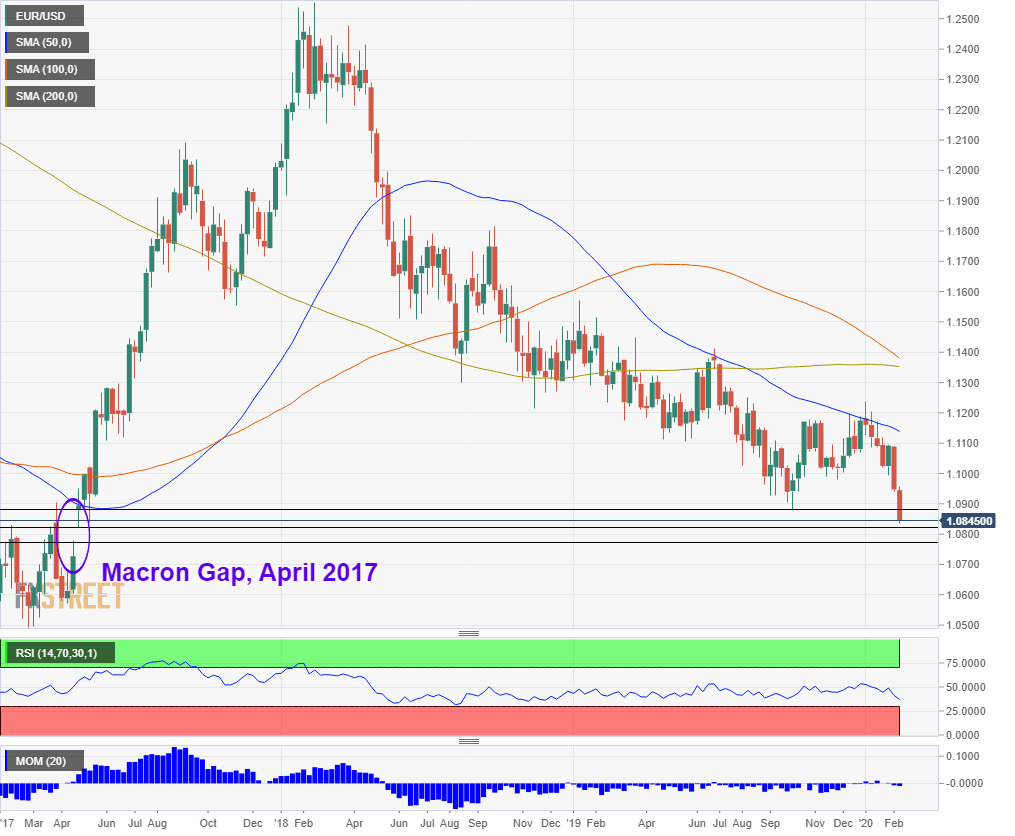

The opposite case is in the old continent. As mentioned earlier, the euro has fallen to 34-month lows against the dollar and is struggling across the board.

Germany, the eurozone's locomotive, has ground to an economic halt and refuses to change its constitutional brake on deficit spending. Berlin's reluctance comes despite crumbling roads – its famous autobahns are not up to speed – and low borrowing costs. Years of austerity and the European Central Bank's bond-buying schemes have pushed German yields to the negative territory – investors are paying the country to take their money.

Why? The ghosts of the past are weighing on policymakers. Back in 1923, the young Weimar Republic suffered from hyperinflation due to war reparations and the consequent French occupation of its industrial Ruhr valley. Scenes of people carrying wheelbarrows of worthless cash are seen as contributing to the rise of the Nazi regime.

Moreover, the German word Schuld means both debt and guilt. Citizens of this wealthy nation are used to save, not borrow, to spend. Chancellor Angela Merkel's current grand coalition has stuck with the Schwarze Null – black zero – surplus policy despite installing a center-left finance minister.

As the largest and most prominent member in the EU, Berlin's way of thinking has shaped Brussels' policy as well. The fall in the exchange rate of the euro has failed to boost exports enough to compensate for the absence of inward investment.

Will Germany change and lift the euro? At the time of writing, the lack of an heir to Merkel means political change may take longer, but new forces inside and outside the country may make a change at some point.

See The optimist's guide to the old continent – Why Germany will change and how EUR/USD may surge

In the meantime, EUR/USD is at near three-year lows:

Governments vs. central banks

The importance of fiscal spending is rising as central banks' ammunition is running low. The ECB's deposit rate is at -0.50% – deep in negative territory. The BOE's interest rate is at 0.75%, and the Federal Reserve stands out with 1.75% – still well below pre-crisis levels.

Should traders write off central banks?

Not so fast. As the examples above show, public spending has a growing impact, but central banks may still move markets. First and foremost, fiscal spending is amplified by reduced stimulus from rate-setters – and that is what eventually moves currencies.

Moreover, central bankers still have some tools in the shed. All three institutions mentioned above can restart or expand their bond-buying, or Quantitative Easing schemes. Corporate bonds and even stocks may come into play.

Finally, if government spending goes into overdrive, elusive inflation might show up – triggering rate hikes and a greater role for monetary policy down the road. Central banks have gone from being puzzled with the dearth of inflation to being resigned to "lowflation" as a fact of life. However, nothing lasts forever.

Conclusion

Fiscal policy will probably have a growing impact on currencies in the medium term, and indebted governments' currencies are likely to be rewarded with higher valuations. Central banks' impact is diminishing amid low rates, but they still have influence and may return to battling inflation in the longer term.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.