Rocky Canadian recovery

Brief Review of Canada’s Fiscal & Monetary Situation

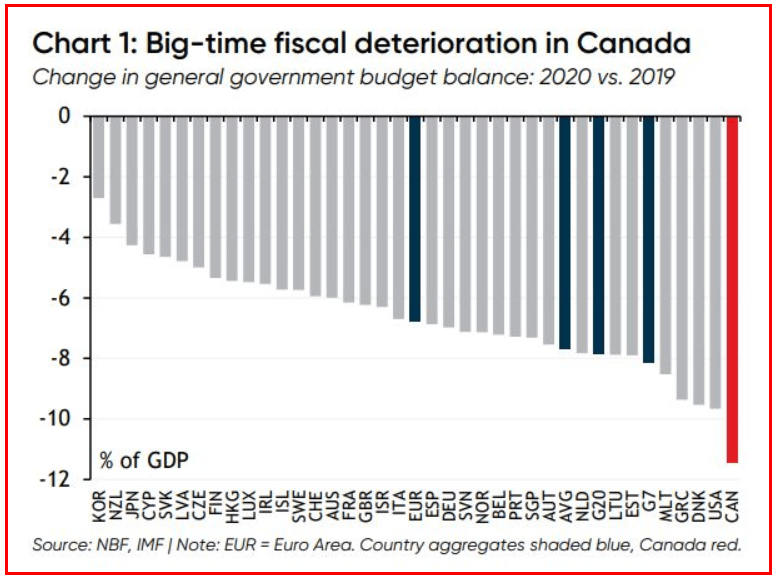

Notwithstanding political rhetoric, the fact is Canada’s fiscal deficit was larger than any other advanced nation as a percentage of GDP in 2020 (over 15%). Whether fully warranted or not, the government spending spree was record-breaking, while GDP and government tax revenues plunged.

Below, the chart provides some visual context:

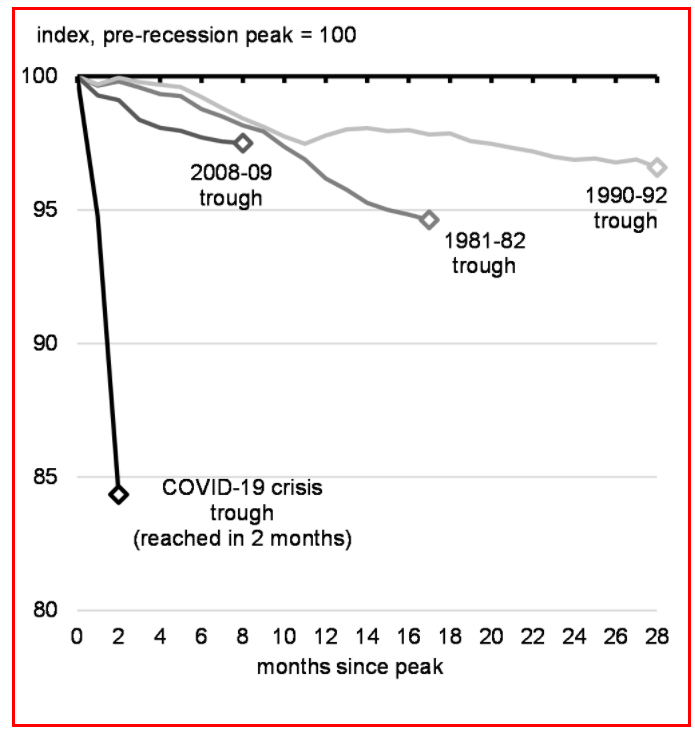

To get an idea of how seismic the economic shock was in 2020, see the chart below where the peak to trough of the 2020 recession is compared to others in the past.

Source: Government of Canada/ budget.gc.ca

The big question becomes, how did Canada manage to spend so much?

Simply put, Canada’s debt to GDP ratio is on a glaringly unsustainable path. In a completely free market, there would be nowhere near enough demand for Canadian Government Bonds to maintain record-low borrowing rates for the government.

Enter The Bank of Canada (BoC). The central bank has stepped in to fill the demand void, but there are real consequences to their actions. Many new monetary policies were implemented many brand new policy tools in 2020 to allow government financing at artificially low interest rates. The BoC has (so far) monetized over $200 billion in government debt, and stay tuned because there is much more issuance to come!

The most impactful tools to keep an eye on when it comes to the BoC’s balance sheet are term repos and government bond purchases.

Repurchase agreements, or “term repos” are conducted by means of the BoC temporarily buying assets from dealers in government securities (the largest banks in Canada). The BoC provides liquidity by holding the assets in exchange for cash, with an agreement the large banking entities/ counterparties will repurchase these assets at a later date. Repos often carry one or three-month terms and as of October 2020, repo operations are being conducted on a bi-weekly basis. The repo process has helped keep lending markets liquid and interest rates artificially low in the banking system. This is a big reason why we’ve seen such a huge wealth transfer to those who were already the wealthiest before the pandemic.

The other main liquidity boosting tool at the BoC’s disposal is of course QE, government bond purchases. This increases the money supply at a faster rate because entirely new securities are being issued by the government and the bank simply buys them with new bank reserves it has created out of thin air by simply marking up accounts digitally with the click of a button.

The BoC government Tiff Macklem recently stated that the BoC is not near the point where they would consider slowing the pace of QE. The BoC’s QE program currently stands at $4 billion per week!

The BoC’s website has more detailed information on repos & QE operations.

The end result of the BoC’s extremely “creative” monetary policy measures is to encourage more leverage in the banking system by keeping interest rates artificially low, boosting the pace of debt creation, and therefore accelerating growth in the total number of currency units in circulation (monetary inflation).

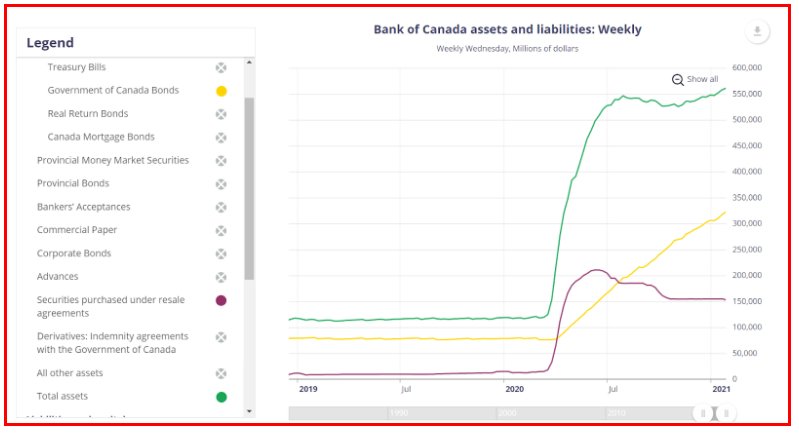

The chart below shows how the staggering pace of BoC asset purchases has impacted its balance sheet in the last year. From under $120 billion at the beginning of 2020, the balance sheet had shot up to nearly $550 billion by the end of the summer! It’s now making new highs after a brief and insignificant period of decline.

Note: the speed at which the BoC is monetizing Canadian Government Bonds is steady and speedy!

Perhaps most startling to Canadian taxpayers is the fact that the BoC’s asset purchases have been the largest as a percentage increase compared to any other advanced nations’ central bank. It’s important to note that the BoC balance sheet was not even needed as a significant tool to dig out of the great recession of 2008! It goes to show how quickly Canada’s fiscal situation has deteriorated.

One of the biggest issues many economists and analysts who study monetary policy have with such an aggressive balance sheet expansion is that the process actively encourages credit flows into the financial economy, rather than the real economy. This is known as the “Cantillon Effect,” where the wealthiest in society situated closest to the source of money creation stand to benefit unfairly. As credit is diverted away from the real economy, malinvestment and financial bubbles are produced. Richard Werner has expertly explained this through his “Quantity Theory of Credit” - a superb contribution to economic thought.

In truth, the BoC’s tools have divorced the financial sector from the real economy. By monetizing government debt and expanding the money supply so quickly, the central bank risks destabilizing the financial system moving forward - indeed, they’ve created the perfect recipe for even bigger future bubbles with dangerous amounts of credit sloshing around the system.

One solution to this problem would be to implement policies that encourage a larger amount of credit to flow into the real economy. In the past, one of the most efficient ways to accomplish this was through community banking. Post-WWII German banking has proven that with many more small community banking institutions, the lending process becomes more “human.” There are fewer excessively large banks, and the system naturally prioritizes the creation of productive loans rather than just counting on a “repo window” to stuff their balance sheets with liquidity if needed. Community banking can also eliminate the idea of “too big to fail banks,” an idea that has become the root of much societal tension in the past decade.

So, what did Canada get for all this anyway?

Perhaps most importantly, we must ask what the Canadian taxpayers have gained from record spending and easy central bank monetary policy. After all, the BoC’s balance sheet is technically a taxpayer liability and the average Canadian will be on the hook for it in the years to come, along with the deficits run by the government.

Well, it doesn’t look pretty!

Canada seems to be suffering from an economic principle I will term “low return-on-printing” - the law of diminishing returns applied to currency debasement as a tool to alleviate deflationary economic pressures.

Source: Government of Canada, Fall Economic Statement

Any private institution or individual will take investment risks only when they perceive their return on investment to be positive. Therefore, it’s fair to assume that the Canadian taxpayers might expect big results after such big-spending... Right?

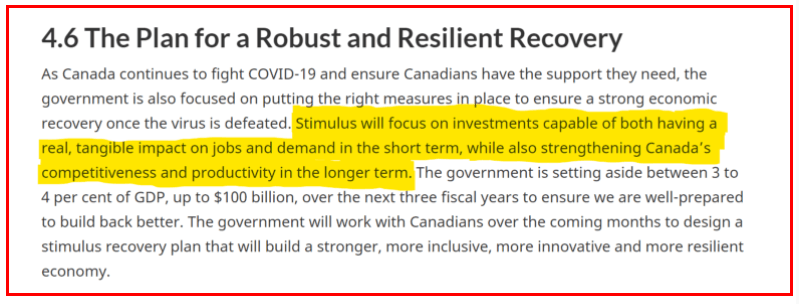

Data suggests the Canadian government is falling short when it comes to making “a real tangible impact on jobs in the short term.” Worse, it’s highly unlikely the spending done in 2020 has built a solid foundation for a robust long-term recovery for the reasons discussed above. When the government spends with so much central bank/ monetary intervention, capital is directed in excess quantities to non-GDP producing activity in the financial sector. This doesn’t help the labour market and instead produces a “paper” economic recovery.

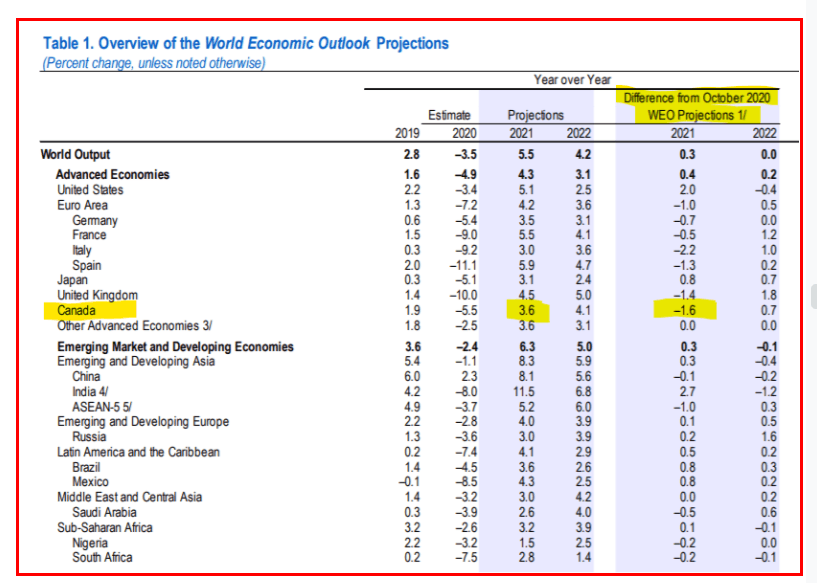

There have been two major developments recently that should be a cause for concern in Canada. First, the IMF downgraded Canada’s growth expectations. The preliminary GDP numbers suggest Canada’s economy contracted by slightly over 5% last year. The nation is also expected to lag the average advanced economy significantly on the global “road to recovery.”

I’ve highlighted Canada’s downgraded GDP projection below:

Source: IMF data

GDP does not equal productivity!

Consider the following thought experiment to explain why Canada’s “return on printing” is so low, and why this is so detrimental to the private sector’s productivity and ultimately the economic well-being of Canadians in the long run.

Canada’s GDP was about $1.73 trillion (USD) in 2019, and 5% lower by year’s end in 2020 let’s say. Many might argue that “it could have been much worse!” Or, “after all the lockdowns, being within a few percentage points isn’t so bad!”

There’s a problem with this perspective. Investors and concerned taxpayers must break down the total GDP as part government spending (drain) and part private sector activity (wealth-creating).

Imagine the Government made one single transaction in 2020, and the entire nation was locked down producing absolutely zero dollars in nominal GDP. If the government’s single transaction was the purchase of a farm for $1.73 trillion (money created out of thin air by the BoC), the GDP would technically still be the same as the year prior! Headline GDP would look great in nominal terms, nothing to worry about, right?

We all know that example would mean no wealth is being created. This is why headline GDP can be very misleading. If the government’s spending has greatly increased to reach the same level of GDP, then by default the private sector has shrunk and Canadians are less wealthy.

If the government needed to spend a record amount (15 +% deficit as % of GDP) for GDP to “only” be down 5% from 2019, the real wealth created for Canadians in the private sector is down by much more than just 5%, closer to 20%!

The point is, the Canadian economy can grow exponentially in “official GDP” terms through government spending while the average Canadian’s standard of living is actually being crushed. Government spending and monetary debasement cannot fill the void of a GDP based on honest productivity. Real goods and services and the velocity of money are what produce a higher standard of living. Academic and bureaucrats seem to be forgetting this.

February 5th jobs report, “low return on printing” confirmed!

Today, Canada’s monthly jobs report came out as it does the first Friday of every month. It will go down as one of the most disappointing in history.

We learned that in January the Canadian economy lost over 2oo thousand jobs. The unemployment rate shot up to 9.4%, which is far worse than expected.

For context, the unemployment rate peaked at 13.7% in the early summer last year and had steadily declined to 8.5% more recently. Canada’s economy is now headed in the wrong direction.

Make no mistake, these are abysmal numbers. In the chart below, I circled the peak unemployment rate Canada’s economy endured in the wake of the 2008 financial crisis and recession. It was 8.6%. As you can see, a full year after the world began to first take the pandemic seriously, Canada’s labour market is still in worse shape than at the peak of 2008’s crisis.

Adding to Canada’s economic woes are the jobs lost with the termination of the Keystone Pipeline project. The new administration in the United States axed the pipeline via executive order.

The blow to Canada’s oil sector will also likely mean less demand for the Canadian dollar. Canadian crude has been steadily less in-demand internationally, and the sector represents nearly a tenth of national GDP and an even larger percentage of exports.

Why does it all matter?

Business and Investment Risk

If the key was to simply spend, spend spend and monetize government debt, Canada would indeed be leading the world with the strongest economic recovery among advanced nations.

The negative IMF outlook and rising unemployment data suggest that Canada’s current economic situation is a perfect example of Keynesian excess. The law of diminishing returns is kicking in and Canada’s “low return on printing” is building a fragile economic recovery. This will dampen future growth for the coming decade.

What is required is less government, and a more robust private sector producing real goods and services - real wealth! No nation has ever achieved a high standard of living solely based on an increasing supply of currency units and higher nominal prices.

At this rate, the Bank of Canada’s policy risks pushing a huge segment of the Canadian economy out of its overpriced housing market, one of many Canadian financial bubbles. The burden of inflation risk crippling the middle class while job opportunities are hard to come by.

If Canada continues to expand its currency supply as the main remedy to economic turmoil and deflationary pressures, it’s only a matter of time before painful stagflation is felt across the country. This economic phenomenon is marked by structurally high unemployment, with rising prices of everyday goods and services.

Ironically, the BoC seems to want stagflation. They’ve repeatedly called for higher inflation, promising to achieve a rate in excess of 2 percent per year. This policy decision stands against the best interests of the working class, which is still facing a record unemployment crisis.

Market impacts

It’s difficult to maintain a positive outlook on the Canadian oil sector. Moreover, Canadian banks are dangerously leveraged, vulnerable to another deflationary shock to their balance sheets.

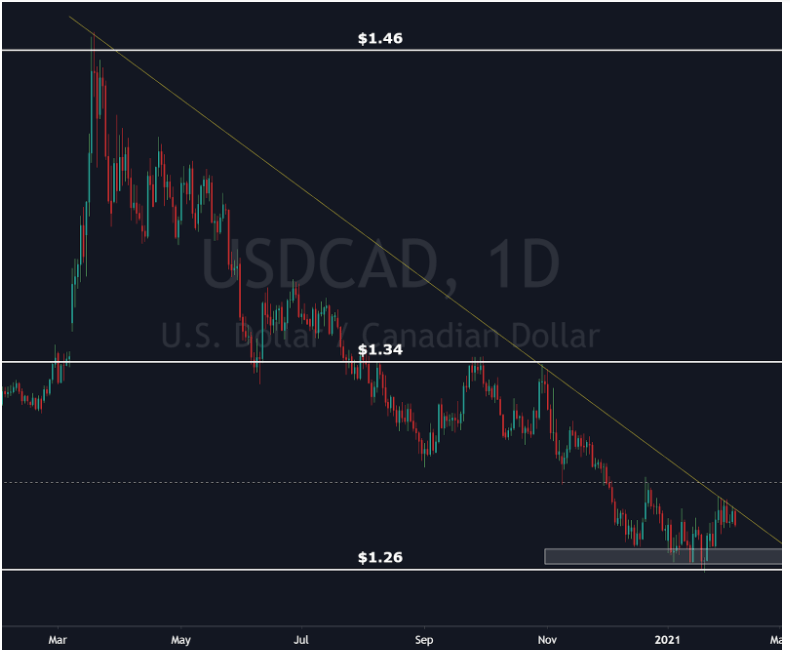

It seems that the Canadian loonie is relatively over-priced compared to the US dollar for now. USDCAD has fallen since last March’s panic in markets, but it seems the bad is fully priced into the USD and there is not much good left to price into the CAD in comparison.

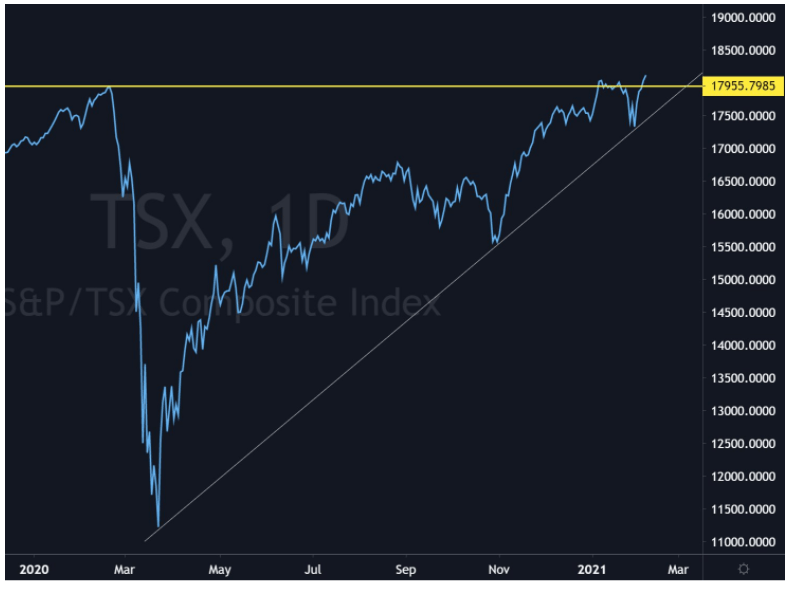

Below, we see the TSX (Toronto Stock Exchange) making all-time highs. The index is breaking above $18000 (CAD) amid dreadful real economic conditions. Betting on these valuations heading higher from here is akin to betting on the ability of policymakers to further distort the economy.

In theory, it’s possible Canada experiences a “melt-up” scenario. If another round of deflation never materializes and currency debasement continues to drive financial assets higher, the BoC risks finding out the hard way what it’s like for the public to lose faith in cash, preferring financial assets at any price.

For now, deflationary pressures will persist in the real Canadian economy, while monetary inflation rates drive financial market activity and credit flows.

Emerging market equities seem relatively attractive for Canadians considering the currency risks associated with the Canadian markets and lack of robust economic activity.

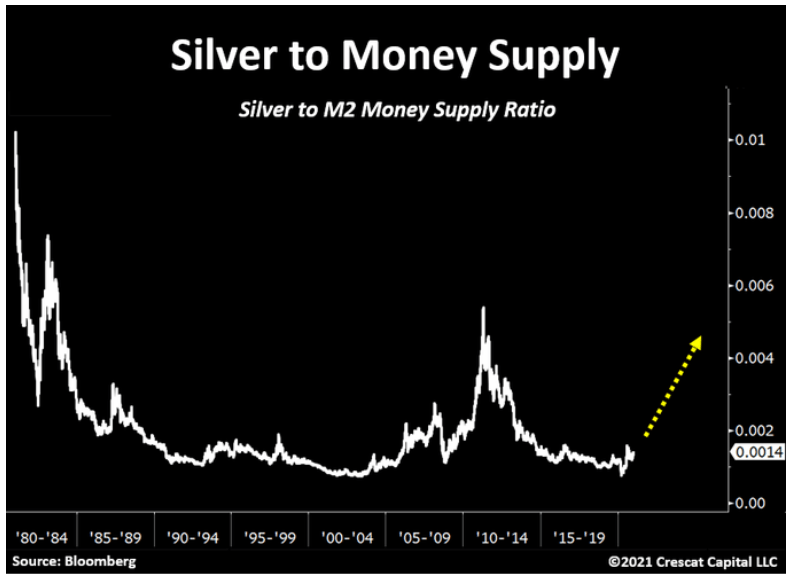

One bright spot in the Canadian investment matrix lies within the mining sector. Precious metals, battery metals and commodities are abundant in Canada. Many of the top mining sector producers and explorers are traded on the TSX and represent some of the best value the investing world has to offer.

Here’s a reminder of how cheap silver is compared to the M2 money supply in the US, the same goes for gold:

For Canadian businesses and investors, it will be important to plan for more currency risk on the horizon. As many of the brightest minds in macroeconomics have been repeating, it’s always prudent to own an insurance policy in the form of physical precious metals.

Author

Miles Ruttan

Bytown Capital

Miles' focus at the firm is to oversee our macro analysis, with the emphasis being placed on global credit and liquidity flows.