Rates spark: The long way up

Higher rates are ongoing, but we wouldn’t blame it on the, very moderate in our view, central bank tone. Improving economic data after the Covid 19-induced soft patch is a more credible, and durable, driver for higher rates. The structure of the always pivotal US curve has also been bearish, as the belly has cheapened. That signal remains in place.

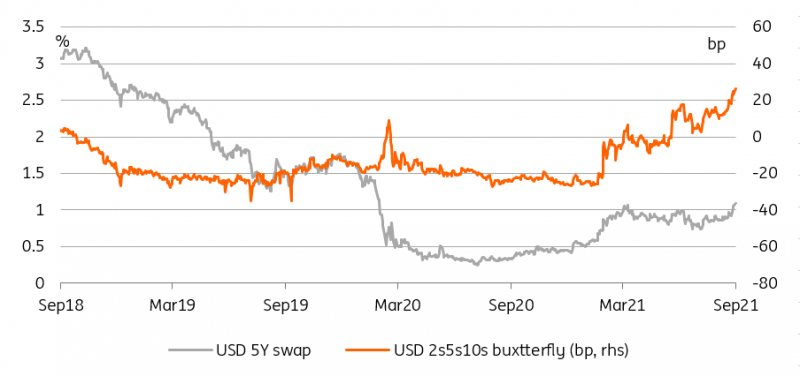

US market rates lead the way up, as the belly cheapens further

The move in US rates is coming from the belly of the curve. That's a classic bearish construction. It's what you would expect to see happen as a curve begins to position for a future rate hike, but not an imminent one. The 5yr area has been cheapening over the past couple of weeks in fact, quietly but surely. It snapped cheaper again after the FOMC last week. Not immediately after, but by the end of the US trading day. The move has also been driven by a nudge higher in real rates, which is good to see.

There has been some de-risking in evidence from flows in the past couple of weeks. Evergrande masked some of this on Monday of last week, and saw market rates come down, back below 1.3%. But the tendency since has been to test higher. We've now hit 1.5%. Big move. A bold 20bp move from the 1.3% area. It feels like a breakout that will see some follow through to the upside in rates, but we'd expect some consolidation first as there is a lot going on in the background to be cognizant of.

The belly of the USD curve keeps cheapening up in this sell-off

Source: Refinitiv, ING

We need to keep a firm watch on system risk. USD Libor is a reasonable measure of this. It's been edging higher since Evergrande really broke as a global story last week. Any material correlation from this story would add further to system risk, putting a bid back into Treasuries. That apart, the test higher in yield makes sense. It was coming...

Expect mostly soothing words from central bankers today

Central bankers have no intention to leave the centre stage judging from the schedule of officials due to speak today. The main event is the beginning of the ECB’s virtual conference (usually held in Sintra). We think EUR rates had nothing more than a passenger’s role in the rise of global rates of late, with ECB speakers making abundantly clear that the recent, and upcoming, rise in inflation does not warrant a policy response. Lagarde was the latest hinting at a broadening role of its APP QE programme, saying the involvement of Greece will be looked at in late 2021, or early 2022. In short, more easing is indeed still on the table and the ECB will be prudent in reacting to any inflation overshoot.

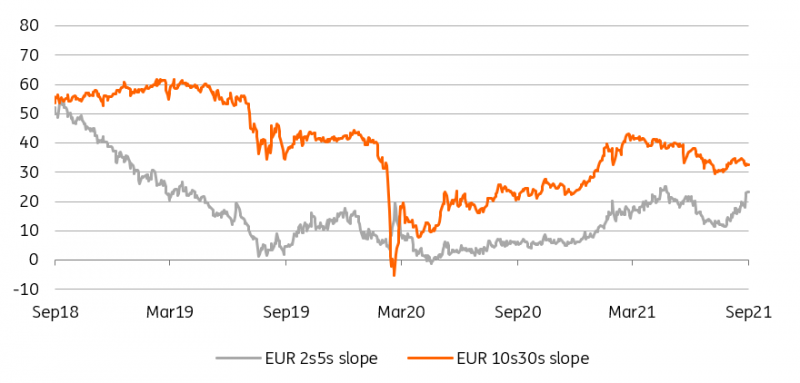

The EUR curve is also concerned with ECB tightening, prematurely

Source: Refinitiv, ING

Fed and BoE communication are more likely culprits for the back-up in yields but, here too, we think fears of an immediate policy U-turn are misplaced. BoE Governor Andrew Bailey stressed that point in a speech yesterday saying that the Bank is not equipped to remedy supply-side constraints, the main reason for the current inflation spike. Another interesting takeaway was his insistence that any tightening would come from hikes in the Bank Rate rather than through QE tweaks. This confirms the view that balance sheet reduction, once it starts, will largely happen in the background, unaffected by changes in policy outlook.

The path forward for developed market rates is undeniably higher, in our opinion. We share the view that rising inflation and economic recovery will prompt central bank tightening but we struggle to see reasons for a market panic to happen now. Fed balance sheet reduction is a case in point. We find it difficult to blame bond weakness on it, since tapering has been talked about pretty much since the start of the year. The improvement in economic data we expect after the Covid 19-related soft patch seems like a much more credible driver for higher rates going forward. It also brings hope of a re-steepening of the US yield curve as markets shed their gloomy outlook, eventually giving space for the Fed to engage in a meaningful hiking cycle.

Today’s events and market view

The main event today for rates markets is the ECB’s Sintra (online) conference with interventions from President Christine Lagarde and board members Luis de Guindos, Isabel Schnabel, Fabio Panetta, and others. Also on the topic of central banks, Treasury Secretary Janet Yellen and Fed Chair Jerome Powell are due to testify in front of a senate panel. If anything, an abundance of central bank communication (see above) should help bond markets to regain their footing. We expect yields to drop this week, with 1.5% in 10Y US Treasury yields acting as a near-term resistance. The medium term towards higher rates remains intact in our view.

Economic releases of note will mostly come in the US session, with house prices and consumer confidence the highlights.

The Netherlands will launch a new 2029 bond for €3-5bn. The US Treasury will auction $62bn of 7Y debt.

Read the original analysis: Rates spark: The long way up

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.