Rates spark: The dam holds, just in time for the Fed

It looks far more likely that the Fed delivers a 25bp hike than goes for no change. This is (just about, or nearly) discounted. Not to deliver would in fact be a shock. Calmer market conditions should breed cautious optimism at the ECB’s Watchers conference. Further hawkish re-pricing should take 10Y Bund yields above 2.5% (equivalent to 3.2% in 10Y swaps).

The Fed set to go ahead and deliver the 25bp that's discounted. But then what?

With a 25bp hike 80% discounted there is a green light for the Fed to go ahead and deliver that. It's unlikely the Fed will provide much guidance for the May meeting though, but it's also unlikely we get a so-called dovish hike. The Fed needs to keep some form of pressure on. The big take-away is likely to come from the press conference, which should include lots of questions on the banking system, and the (emergency) measures already employed to secure it.

There will be a keen ear to any commentary from Chair Powell on the new Term Funding Program. The terms on this facility are so good that a significant take-up is quite probable. Initially there may be reluctance to take advantage, so as to avoid raising red flags on individual names. But names will not be published, and once volumes build, more and more (mostly smaller) banks will likely use the facility. Note that this will re-build bonds on the Fed’s balance sheet. Not quite quantitative easing, but going in the opposite direction to the quantitative tightening process that’s ongoing (through allowing redeeming bonds to roll off the front end at a pace of US$95bn per month). Meanwhile, there is still some US$2tn of liquidity going back to the Fed through the reverse repo facility, the counter of which shows up in lower excess reserves than there would otherwise be. In fact, falling deposits in the banking system generally is reflected here too, with many such deposits showing up in money markets funds, and from there into the Fed reverse repo facility.

Directionally we doubt there is huge room to the downside for market rates, especially given the virtual collapse seen in the past week or so. That said, further falls in the near term are entirely possible should the banking story deteriorate further. But so far the banking issues are more idiosyncratic than systemic, and a system breakdown has become far less likely in the wake of the extraordinary deposit support announced by the Fed in the wake of the Silicon Valley Bank collapse. Plus, delivery of a 25bp hike still means the Fed is tightening, there is likely at least another hike to come. In the background we envisage a medium-term fed funds rate equilibrium at 3%, so long rates should not really be shooting below this, barring exceptional circumstances. There is in fact a probable scenario where longer dated rates are under rising pressure, even as the front end ultimately sees pressure for lower rates later in 2023. The inflation issue remains a significant one, and any let-off through interest rate cuts, or even the discount thereof, would leave longer rates less protected from residual medium-term inflation risks.

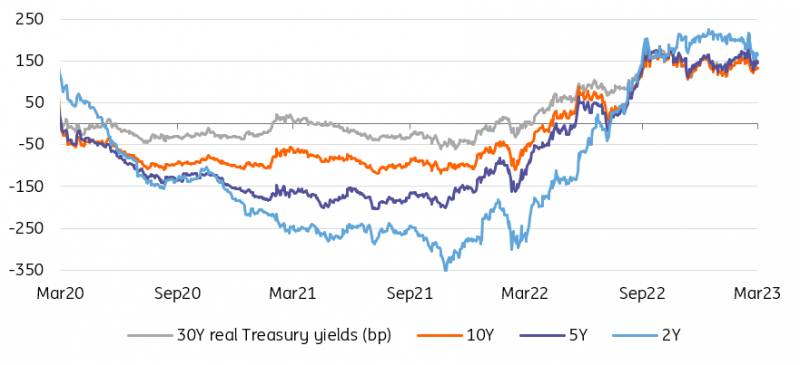

Treasury real yields have not materially changed despite US regional bank jitters

Source: Refinitiv, ING

How high can Euro rates go?

The stabilisation of various banking stress and broader financial market indicators has put markets back on alert for more monetary tightening. In Europe, the swap curve is implying a terminal deposit rate around 3.25%, only 25bp higher than the current rate. This compares with our (pre-banking crisis) call for a 3.50% peak, and market pricing of around 4% just two weeks ago. Clearly, the world has changed since then, but European Central Bank (ECB) officials have, in recent days, implied that more tightening will be required. In some instance, this took the form to oblique references to too high inflation. In other cases, of a direct rebuttal of markets pricing a terminal rate under 3.25%.

The ECB’s Watchers conference today should be an opportunity for governing council members to drive the message home. ECB Supervisory Board chairman Andrea Enria’s parliament hearing yesterday seemed to suggest the central bank sees it as its base case that no further contagion will occur. We surmise that as time passes with no further lapses in banking stability, the central bank will progressively become more confident in its ability to deliver further hikes. The question is how many.

Using the previous peak in Estr forwards as a guide, we think the curve can at least price one more 25bp hike than currently, which would take us to June, in line with our earlier call. Even 50bp would not be a surprise at all. Based on recent trading relationships, this should translate one-to-one into 2Y yields, and roughly half of that should be reflected into 10Y yields (a little more for Bund, a little less for swaps). This should put 2Y German yields above 3%, and 10Y above 2.5% (equivalent in 10Y swaps of 3.2%) in case of further hawkish re-pricing, with 2.80% and 2.40% realistic short term forecast for 2Y and 10Y yields respectively. This, of course, is subject to no further banking contagion, and provided the Fed presses ahead with its own hike at this evening.

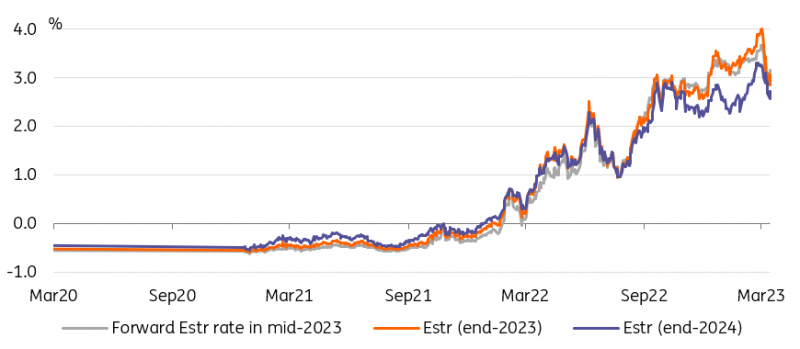

The EUR curve can easily price one or two further 25bp hikes this year

Source: Refinitiv, ING

Read the original analysis: Rates spark: The dam holds, just in time for the Fed

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.