Rates spark: No news is good news for rates

No banking contagion news allows rates to jump back but we doubt more than one Fed hike can be priced by the curve. This means the 2Y hovering around a 4% yield. Euro rates have more upside on a hawkish European Central Bank but monetary tightening is working its way through the system.

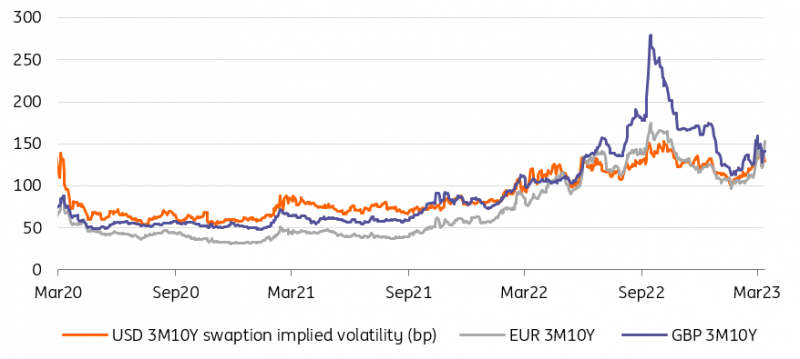

2Y Treasuries stuck around 4% until data catches up to the economic gloom Sanity seems to prevail, at least so far this week, with no new contagion fears weighing on sentiment. Realised volatility in rates remains elevated, with double-digit moves in basis point terms on the 2Y-10Y segment of main developed market curves on Monday. This is also reflected in still high implied swaption volatility, celebrating lower banking worries but dreading a return of inflation angst. Our base case is indeed for further improvement in sentiment as no new news hits the system, and as contagion fears ebbs. This is not to say we’re expecting a return to the pre-Silicon Valley Bank (SVB) state of play, however.

This is clearest in the US where the negative impact on credit, a good chunk of which is provided by regional banks, is increasingly certain. Commercial real estate has emerged as a key area of concern as it accounts for a disproportionate amount of lending in this sector. All this is to say that our already cautious outlook on the US economy has been reinforced by recent events. We’re looking for one last hike in this cycle, and expect the Fed will be in a position to cut rates by year-end.

In this light, the drop in US market rates makes sense. Even after yesterday’s sell-off, 2Y Treasury yields ($42bn of which will be auctioned today) hover around 4%. This level has proved a magnet since the breakout of the SVB crisis and a decisive break below would require the curve to price more than the three 25bp cuts we’re forecasting for this year, and which the curve is currently pricing. This is far from impossible, but this would require data to catch up to the economic gloom in markets, or further bank contagion. The path of least resistance seems to be higher yields for now, but setting up for a more meaningful drop when rate cuts come into view.

Implied volatility can remain elevated - On banking stress and on high inflation

Source: Refinitiv, ING

Tightening is making its way through the eurozone economy Even if we’re right in expecting a gradual improvement in sentiment, it is likely euro rates will also continue dancing to the tune of banking news. The tone of ECB communication has remained hawkish in the face of stubbornly high core inflation (and also expected to accelerate in Friday’s March report) and resilient sentiment indicators. For instance, Isabel Schnabel and Luis De Guindos both highlighted the importance of underlying price pressure over the weekend. There are signs that the tightening already announced is making its way through the financial system, however.

Euro rates will continue to dance to the tune of banking news

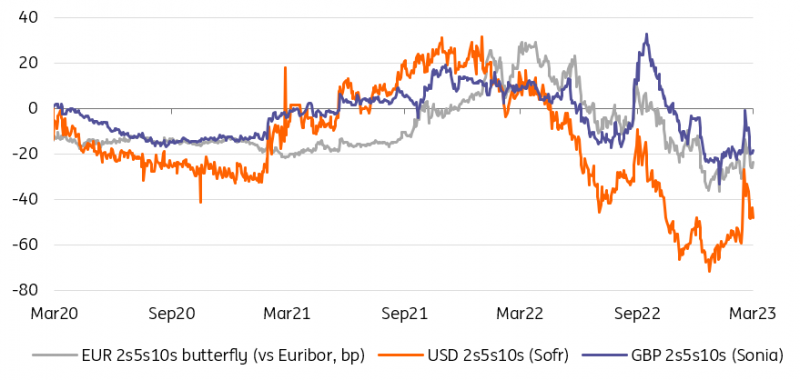

Contagion fears from the US appear contained so far but, even prior to the SVB failure, February data showed bank lending to households and firms dampened by monetary tightening. This has failed to show up in inflation data so far, and European wage dynamics may yet take some time to reflect this. This means the scope of cyclical re-steepening, led by the 2s5s segment, and resulting in a cheapening of the 2s5s10s butterfly, is more limited for European yield curves, at least for now, and compared to their US peer. The 10Y Bund appears unable to drop below the 2% line, and indeed, we feel more comfortable with 2.5% as a level for this year. This is the equivalent of above 3% for 10Y swap rates.

Further cheapening of the 5Y sector on the cards as central banks near the end of their tightening cycles

Source: Refinitiv, ING

Read the original analysis: Rates spark: No news is good news for rates

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.