Rates spark: How not to rock the boat

The ECB meets today. The press conference will be an exercise in avoiding the tapering debate but rates markets are increasingly focused on rate hikes. Record US inflation comes as demand for carry trades is on the rise.

ECB: All lights flashing green

The ECB can breathe a sigh of relief as it meets today. Most economic indicators are flashing green: the vaccination campaign is on track, optimism is at a record high, and reopening promises solid economic growth in the second half of the year. The same is true on the financial front: government yields and swap rates are low, even more so when compared to inflation, and credit spreads are tight.

In that context, it wouldn’t be entirely surprising if the ECB decided to pare back the raft of measures it has in place to support the economy, but our economics team thinks they won’t. Fair enough. As ECB officials have argued in the past, the cost of removing accommodation too early outweighs that of removing it too late. There is also the fact that most see the risk of an inflationary spiral as negligible.

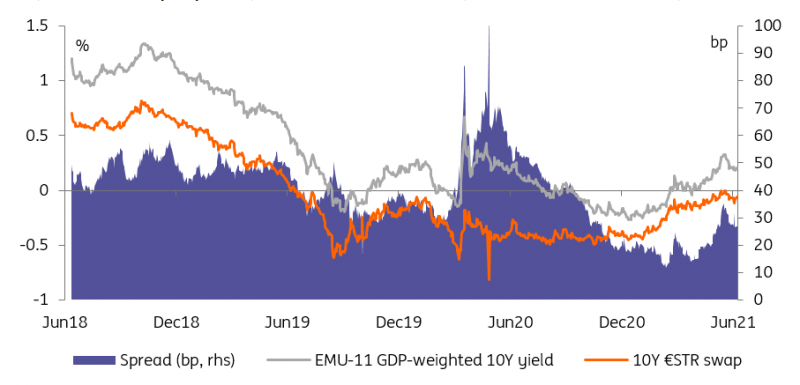

Government yields and swap rates are well contained, espcially compared to inflation

Source: Refinitiv, ING

Strong demand for bonds but beware of economic forecasts

That state of play has triggered renewed interest in carry trades, especially in higher-yielding markets. In Eurozone sovereign bonds, this has happened as Italy and Greece opportunistically returned to primary market with syndicated deals, with Italy also due to carry out auctions today. Tight sovereign spreads should be sustained in our view, in fact we see 10Y Italy-Germany crossing 100bp later this year, with the help of the ECB. The same cannot be said of low ‘core’ interest rates as the recovery takes hold and boosts appetite for riskier assets.

Of course this meeting presents its own set of risks. With markets hooked on monetary stimulus, any hint of withdrawal later this year could upset the current status quo. This is particularly true as markets were led to expect the ECB to delay the tapering debate by another quarter. Any hint, wittingly or not, to the contrary could still send EUR rates into a tailspin. This is particularly true in light of the rally observed across EUR bond markets this week.

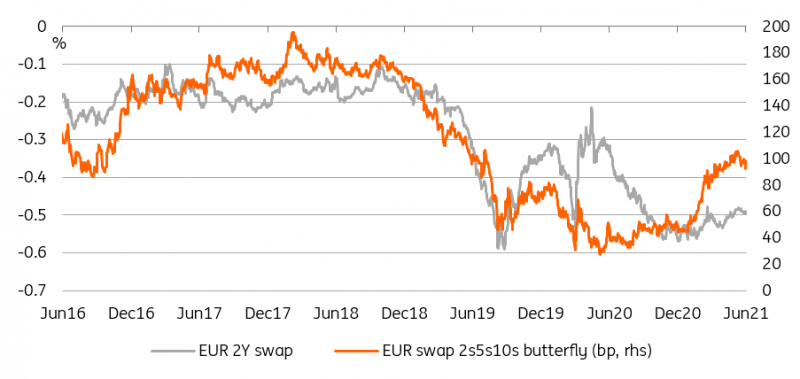

This level in the EUR 2s5s10s butterly is normally consistent with higher rates

Source: Refinitiv, ING

One corner of EUR rates markets that isn’t entirely discounting ECB inaction is the belly of the swap curve, shown with the EUR 2s5s10s butterfly above. Increasingly, maturities relating to the few years starting in 2023 are pricing the beginning of a sustained hiking path by the ECB. This timing implies roughly two years for the ECB to end both asset purchase programmes (PEPP and APP), not a decision it will take lightly. It also implies inflation returning sustainably to target by the time of the first hike. In that respect inflation forecasts published today, especially relating to 2023, will have a strong signalling value, even if we expect President Christine Lagarde to be wise enough to dismiss any tightening discussions.

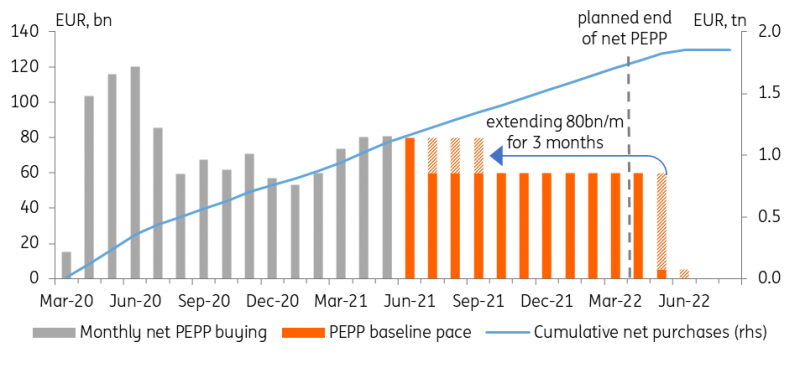

More PEPP buying now means less is left for later

Source: ECB, ING

Today’s events and market views

Even if it is misguided with a medium term outlook in mind, the strength of demand for carry trades makes us side with those expecting further drops in interest rates. All of this could end in tears in case of an upward surprise in US CPI today, for instance if the YOY headline measure rises above 5%. However, price action these past few days have shown a strong bias toward ignoring economic data.

Italy (3Y/7Y/20Y) and Ireland (16Y/24Y) will carry out auctions today, a timely affair after this week’s rally has taken rates lower and spreads tighter, and ahead of the ECB meeting.

Read the original analysis: Rates spark: How not to rock the boat

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.