Rates spark: Data still holds the key

The US debt ceiling is creating a lot of noise, but rates markets are reversing the March repricing on the back of the banking turmoil. Fears of a severe credit crunch have abated, macro data has not shown signs of economies toppling over, all while inflation remains stubbornly slow to decline. As before, the key lies in the data.

Back to pre-SVB levels?

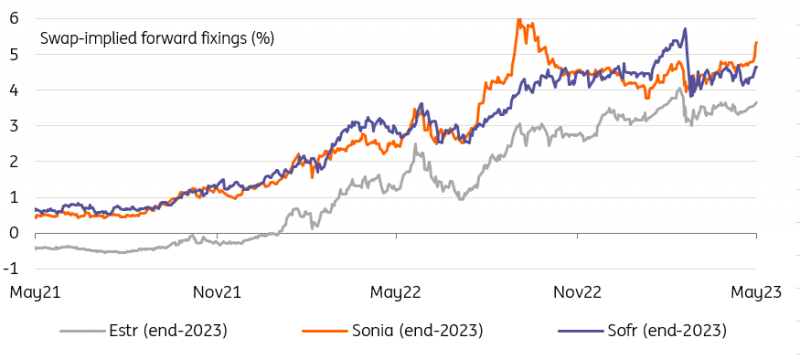

Markets are in the process of taking valuations back towards those that prevailed just ahead of the Silicon Valley Bank collapse. UST 10Y yields have broken above 3.80% again, and that 4% level does not look so elusive anymore. Especially the past two weeks since the last central bank meetings have seen a steady shift higher of hike expectations and/or pricing out of subsequent cuts, the re-flattening of yield curves also signalling some reassessment by markets of where we stand in the current hiking cycles.

The starkest example of the recent repricing was witnessed in the UK in the wake of the latest inflation data. The sell-off in rates continued yesterday with markets now discounting 110bp of additional hikes by year-end taking the Bank rate to at least 5.5%. Even before the UK inflation data certainly struck a nerve this week, fears of a severe credit crunch have abated and macro data did not show any signs of an economy toppling over. At the same time, disinflationary tendencies in the underlying measures are only slowly materialising, if at all.

Credit crunch fears have abated, macro data did not topple over, and inflation remains stubborn

The repricing elsewhere has been notable as well. Take the Fed: A 25bp hike is now almost fully priced by July, the forward fed funds rates are peaking just above 5.30%. Year-end that rate is seen at a bit over 4.9%, implying 40bp of cuts from the peak. In early May, no hikes were priced but three cuts fully discounted by the end of the year. Just ahead of the SVB collapse the peak OIS rate was at 5.5% for July.

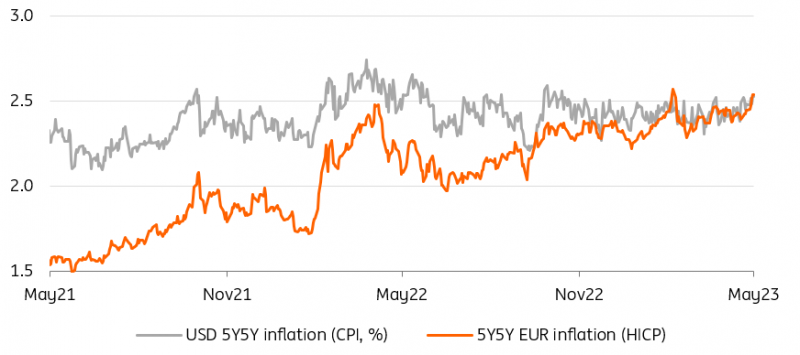

In the eurozone markets are back to pricing more than two further European Central Bank hikes with the peak in OIS forwards at just below 3.75%. Before SVB we peaked at around 4%. Alarmingly for the central bank, market inflation expectations as measured by the 5y5y forward inflation swap have topped 2.5%. The last time we topped these levels it wasn’t the ECB’s intervention that brought them down, but the collapse of SVB itself.

The question is what could halt this repricing this time around as yield levels are looking increasingly elevated. Of course there are the tail risks to consider, but by nature hard to price. It only serves to underscore the central banks desire to maintain maximum optionality. A US default would be a high impact event. But outside money markets at least, it is for now more noise than an actual drag on risk sentiment. Banking tensions have faded, but as before things can suddenly break especially should rates rise further. General profitability concerns within the sector are not going away and will weigh on credit supply.

Central banks are seen tightening again

Source: Refinitiv, ING

Next week’s data could provide some relief

The key, as before, is in the data. One can have a view like ours, that eventually data will turn and force central banks to cut starting late this year. But until then markets will still follow the steady beat of the key releases. The coming days will bring a few of these, and they offer a chance to provide some relief amid the sell-off.

It starts with the core PCE data today, the Fed’s favoured inflation measure. Thislooks set to remain elevated, which could keep the market on edge about a possible June interest rate hike.

The highlights will come next week, with flash inflation data for May from the eurozone. While the headline rate is seen dropping from 7% to 6.4% year-on-year, the core rate is seen budging only marginally. Consensus is pencilling in 5.5% after the 5.6% year-on-year for April.

The US job market data will top off the week. Here the consensus is looking for a softer figure of 180k added in non-farm payrolls in May versus 253k last month. The unemployment rate could nudge up to 3.5% while average hourly earnings for the month are seen up by 0.3%, after 0.5% previously.

Markets' longer term EUR inflation expectations have trended higher

Source: Refinitiv, ING

Read the original analysis: Rates spark: Data still holds the key

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.