Rates spark: Caution still prevails

The BoE has dealt a temporary setback to hawkish bets, but only inflation will show when it eventually pulls the trigger. In any case, we expect this cycle to be shallow. Supply pressure will be felt by EUR rates in the coming days, it should prove temporary. Next week’s US job report is the first one since the June FOMC, meaning a bias towards a hawkish reaction.

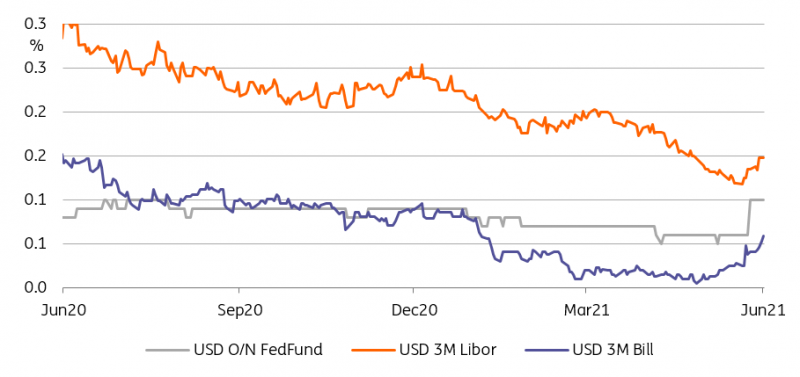

Liquidity continues to pile back at the Federal Reserve

Another day, another amount in excess of USD 800bn returns to the Federal Reserve through the reverse repo facility. At 5bp it's more attractive than it was at zero percent. But that's not the central driver. Rather its the best and simplest attainable amoung alternatives. General collateral repo is trading in the 3bp to 4bp range, and bills out to 3 months are trading at sub-5bp. Those rates are higher than they were. Before the Fed hiked the rate on excess reserves and the reverse repo rates by 5bp apiece, the front end was trading in negative territory. Now, at least, the front end is not negative. But at the same time not at elevated enough levels to take liquidity away from the preferred 5bp at the Fed for money market funds that need to post with an ultra front end label on.

The IOER/RRF hike has lifted US money market rates away from 0%

Source: Refinitiv, ING

It is also noteworthy to see that 3mth Libor has risen too. It's now at 15bp, up from the circa 10bp area seen before the Fed technically hiked by 5bp. So a material effect is being seen right along the front end, for both asset and liability managers. At the same time, the fall in longer tenor rates since the Fed, especially beyond 10yrs (to the 30yrs), implies that the overall interest rate impulse since the Fed has been towards an easing in interest rates. Ironic as the overall tone from the Fed was hawkish, yet despite the mild uptick on the front end, the more important 30yr mortgage rate has dipped, in fact loosening the overall monetary policy stance coming from interest rates.

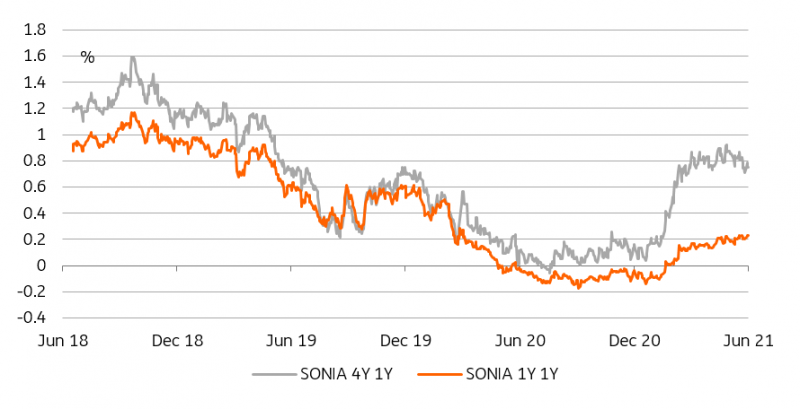

BoE: Down but not out

The reaction to yesterday’s BoE meeting was unmistakably dovish, predictably. We would be wary of reading too much into the BoE sending no new signal on the timing of the first hike. What can be said is that early hike bets looked overstretched in the run-up to the meeting and that some healthy retracement was probable. Beyond that, the first hike in 2022 is still a possibility but would depend on inflation failing to decline in line with the path projected by the Bank. As in other jurisdictions, the next few months will be key.

A shallow BoE hiking cycle means there is an implicit cap on front-end GBP rates

Source: Refinitiv, ING

In any case, the UK is not the US, and any BoE tightening cycle should be a lot shallower than at the Fed. There is always the risk of faster growth and inflation than projected but these seem more like near-term risks to us. This means that there is an inherent cap on short to medium-term GBP rates. This is all the more true given that Governor Bailey indicated the BoE intends to let its balance sheet run down at the same time as it hikes. This in effect reduces the scope for increasing rates as balance sheet reduction is in effect an alternative means of tightening policy.

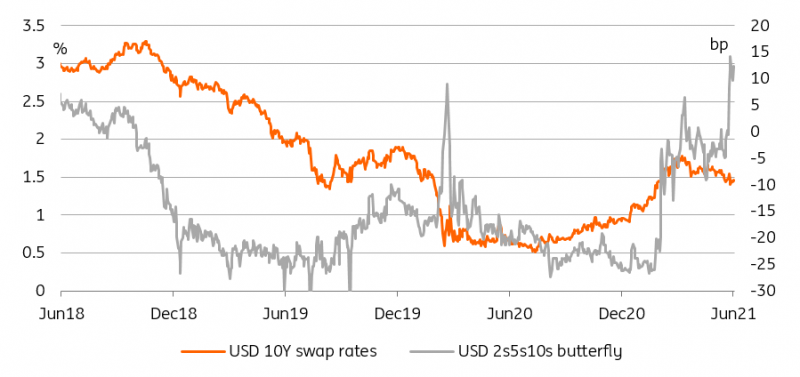

EUR rates to remain a beacon of stability, USD rates in play

EUR rates remain caught between the diverging influences of supply and a dovish central bank. In the end, we think to carry trades will win. The second NGeu deal looms large at the start of next week but beyond a short-term jump in rates/yields, we suspect investors would see any concession as a buying opportunity. With Eurozone CPI expected to roll over next week, and under a barrage of dovish talk from governing council members, we expect to carry traders will retain the upper hand.

Fed hike expectations but stable long-end rates bode well for other markets

Source: Refinitiv, ING

To be sure, the June US job report next Friday will shine new light on how patient can the Fed can afford to be. This will be the first report since the June hawkish warning shot which means market reaction might differ slightly from what prevailed in 2Q. In short, the US market might take a soft print as less of a sign that the Fed’s caution is warranted, and as more of a hint that its hand may be forced by price pressure earlier than it would like to.

This means upward pressure on the 3-5Y part of the curve is less likely to subside. At the very least, this points at greater popularity for short-term hawkish Fed hedges, even if their carry cost seems prohibitive as structural positions. The impact needs not be destabilizing for risk appetite more broadly. Proponents of stable markets can point at still strong curve flattening impetus at the long-end to justify allocation into higher-yielding assets.

Read the original analysis: Rates spark: Caution still prevails

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.