Payrolls and earnings in focus as sentiment starts to improve

Market Overview

With the prospect of tariff exemptions and a thawing of tensions with North Korea, risk sentiment has improved as markets look ahead to today’s crucial payrolls data. Donald Trump is getting exactly what someone with his personality must love, the feeling that markets are moving just because of him. Of course this is not entirely true, but the strange way that the issue of trade tariffs are being implemented means that market sentiment is swinging first one way and then the other. Initially, a sell-off on fears of protectionism, market sentiment has now picked up again as the White House has opened the concept of exemptions for certain countries. A narcissist would just love the concept that trading nations will now effectively have to beg with the US to be allowed an exemption (although quite how the Chinese and EU will react to this prospect remains unclear for now). Not only that, an apparent thawing of relations with North Korea has suddenly appeared from almost out of nowhere. Trump will meet Kim Jong Un in a summit due to take place before May to discuss North Korea’s nuclear programme. This is odd to say the least, and for me, is likely to be merely a delay tactic by Kim. However, risk appetite has subsequently improved, driving the Japanese yen and gold lower. Although the US 2 year yield has ticked higher, the 10 year has barely budged but the dollar has rebounded. Equities have also responded well in Asia overnight. However, we also move into another volatility factor today with Non-farm Payrolls and crucially earnings growth on the agenda. The longer end of the yield curve is sensitive to inflation expectations and surprises on wage growth will be key to how it moves. Once more risk appetite could be dependent on US earnings growth.

Wall Street closed mildly higher last night with the S&P 500 +0.4% at 2739 whilst Asian markets have responded well to the news about North Korea, with the Nikkei +0.5% (helped by a weaker yen). European markets are a touch more cautious in early moves ahead of payrolls. In forex there is also an air of caution ahead of payrolls, but the yen is the main underperformer. In commodities, gold is lower by $3 amidst the improved risk sentiment and stronger dollar; whilst oil is looking to form support.

Payrolls are the big focus for traders today but initially there will be a passing glance at UK Industrial Production at 0930GMT which is expected to improve back to +1.8% for the year having dropped to 0.0% last month. However this release will come and go with barely a blink of an eye as the main event is the US Employment Situation report at 1330GMT. Headline Non-farm Payrolls are always a massive driver of markets and are expected to remain at 200,000 (200,000 last month) however in the wake of the strong ADP number on Wednesday this increases the potential for an upside surprise. Despite this though, Average Hourly Earnings will take the main focus after such a big upside surprise last month. The market expects earnings to grow +0.2% for the month but due to strong comparatives this would be a slip for the year on year data back to +2.8% (from +2.9% last month). The unemployment rate is expected to drop slightly to +4.0% (from +4.1%) which means that the U6 Underemployment data will take on added interest given that the U6 has risen for the past two months to 8.2% last month. The participation rate has now been at 6.7% for the past four months.

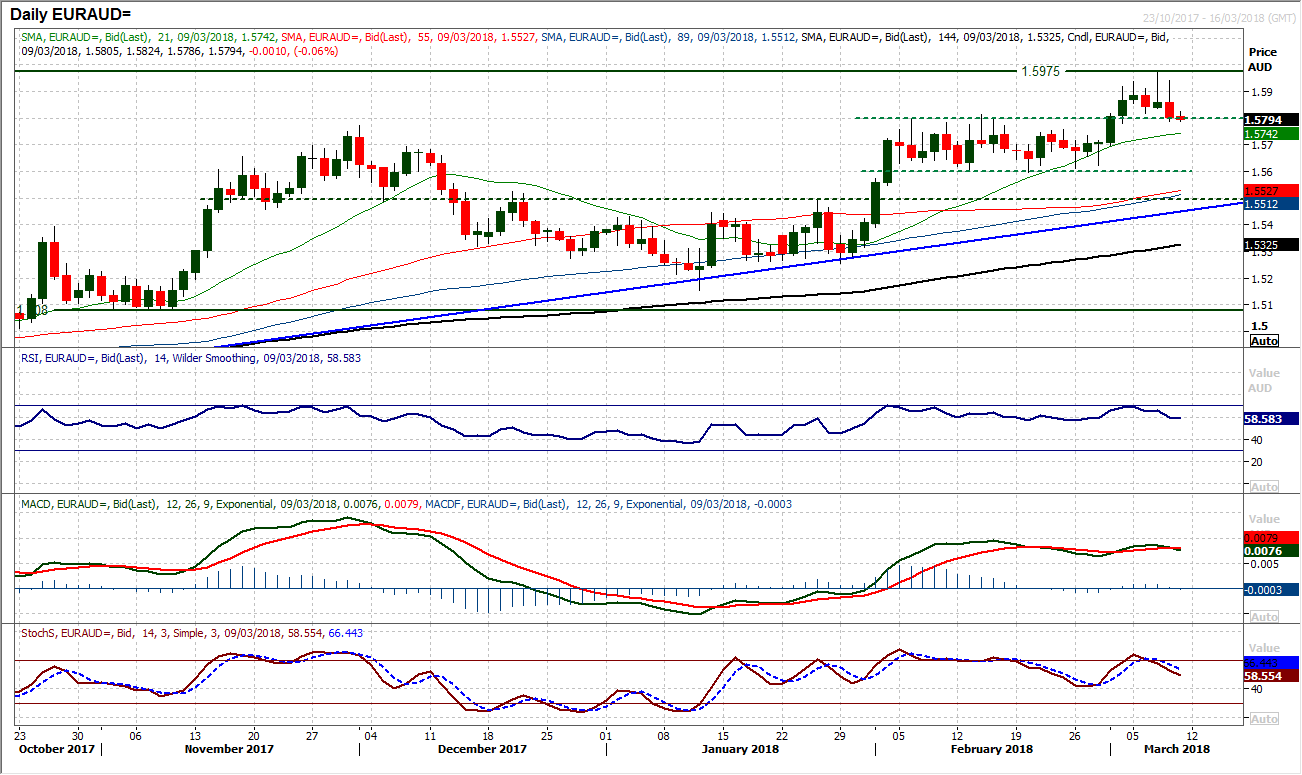

Chart of the Day – EUR/AUD

The breakout above 1.5800 implied a target of 1.6000 and the rally came within 25 pips of hitting its target before a correction set in on Wednesday leaving a highly questionable candle. However, a strong bear candle followed that in the wake of the ECB meeting and has now changed the tone of the near term outlook. Blending both of the last two candles would form one strong shooting star candle and suggests the bulls have lost impetus now. A near term correction could now begin to set in as an unwinding move within the medium term bullish outlook could now form. This is now the third corrective candlestick in a row. The daily indicators are strongly configured but have moved into reverse with the RSI and Stochastics in decline. The hourly chart shows a completed top pattern of implying 150 pips of correction back from 1.5820 as intraday rallies are now being sold into. With the market consolidating around 1.5800 early today, quite how it deals with this breakout support will be key for the near term outlook. A decisive closing break back below 1.5800 would increase the corrective momentum. There is initial support at 1.5780 with the next support at 1.5710. There is now a band of resistance 1.5820/1.5850.

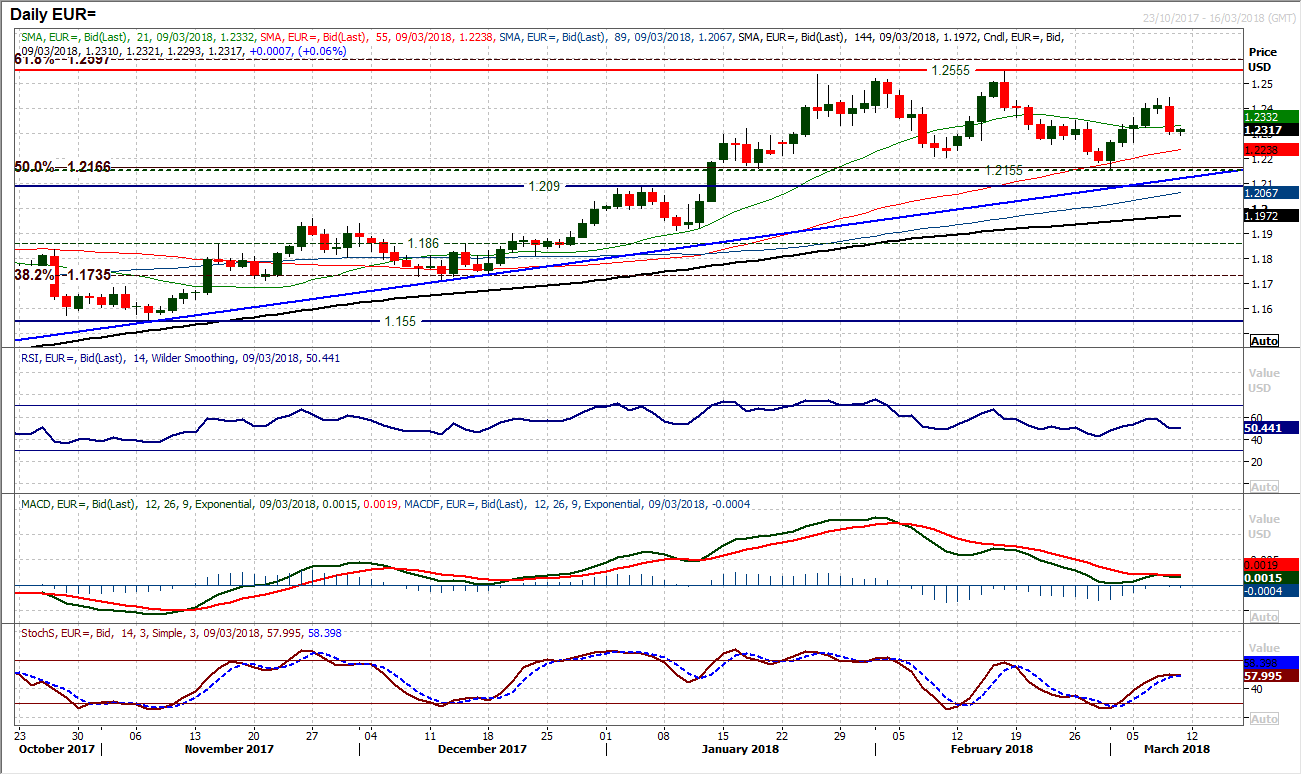

EUR/USD

ECB monetary policy always increases the volatility on the euro and subsequently EUR/USD had a 150 pip range yesterday (Average True Range is currently 9 pips). Mario Draghi was a trigger to sell the euro in the press conference and the euro subsequently sold consistently into the close to end the day around 100 pips lower. This formed a big bearish engulfing candle (bearish key one day reversal) and completely changes the near term outlook. This is a significantly corrective candle that has been posted again and heaps pressure on the downside now. The momentum indicators are now moving into reverse and the concern comes with the MACD lines which are threatening to pull back lower again with the Stochastics the same. There is now significant resistance at $1.2445 from yesterday’s high and the importance of today’s reaction will be key. Another bear candle and the market will begin to think about the reaction low of the previous key reversal at $1.2155. However it is Non-farm Payrolls today to add into the mix of volatility. Initially the market is consolidating but there is support on the hourly chart at $1.2267 and a breach would re-open the downside. Resistance sits again at the near term pivot around $1.2360.

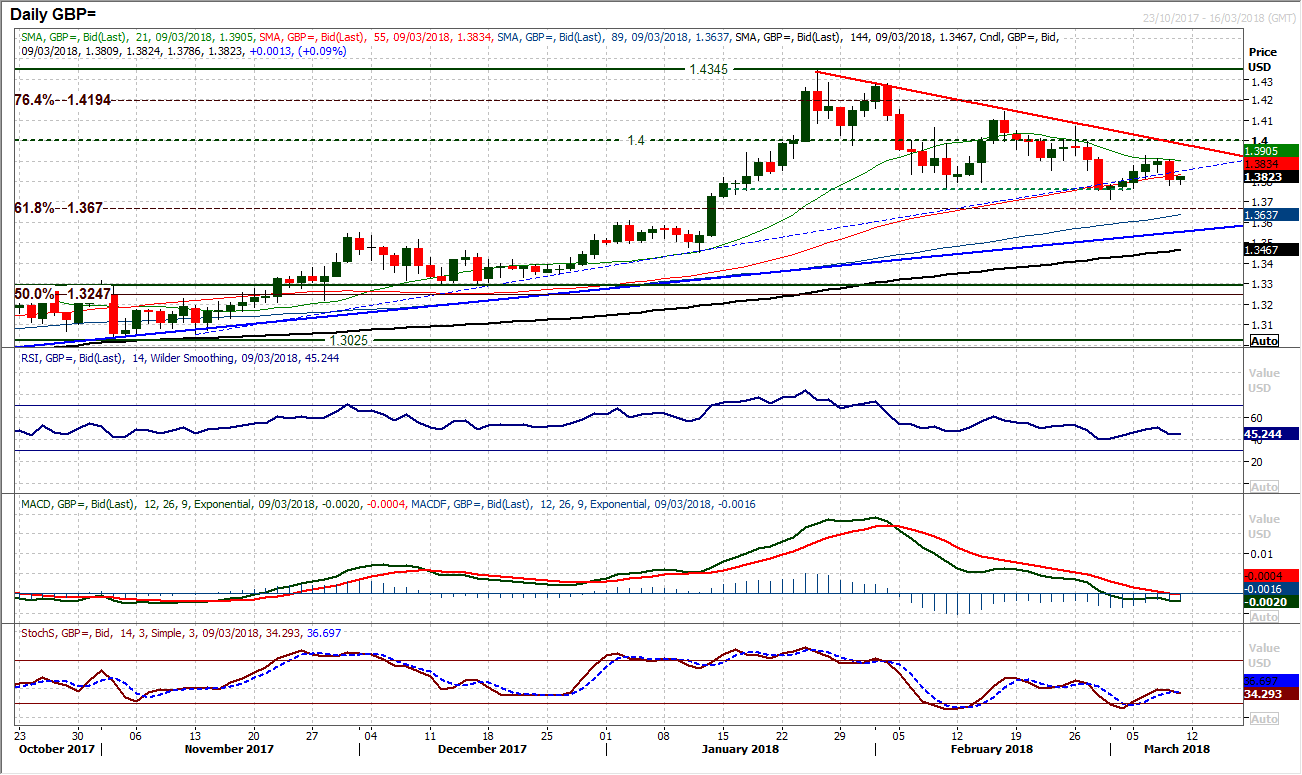

GBP/USD

The creep higher again been sold into as Cable seems to once more found a rally sold into. The market formed a strong negative candle yesterday, losing 90 pips on the day and leaving resistance at $1.3930, with the 21 day moving average becoming an interesting basis of resistance now (currently just above $1.3900). The buyers will be concerned that once more this potential lower high comes with little improvement on the momentum indicators having taken place before the deterioration seems to be setting in. The RSI has rolled over at 50, with another lower high on the Stochastics (which look increasingly negatively configured) whilst the MACD lines never even got going in a recovery. The hourly chart shows momentum also negatively configured now and there is near term resistance at $1.3855/$1.3865. A move below $1.3765 initial support would re-open the recent key low at $1.3710. Non-farm Payrolls will add extra volatility today too.

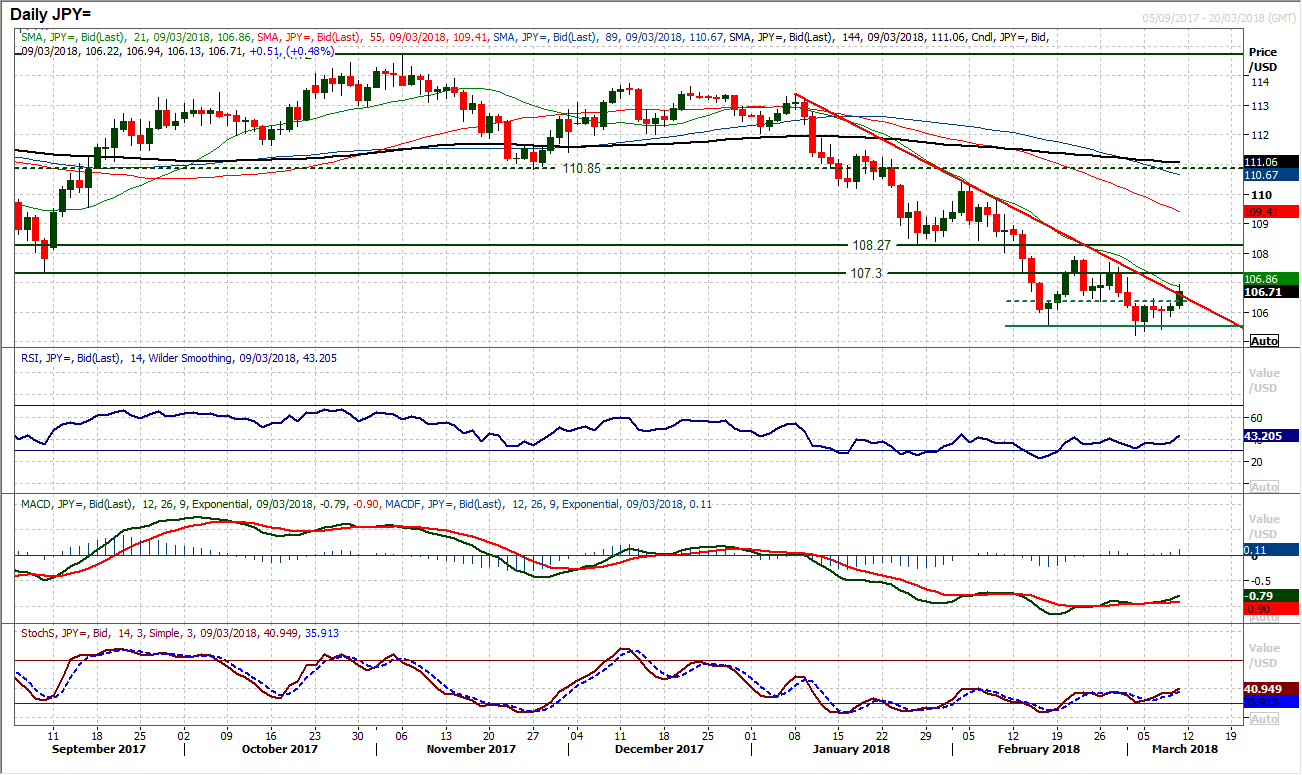

USD/JPY

The market consolidated for much of yesterday’s session (all whilst the dollar made gains against the euro and sterling), but overnight there has suddenly been a shift in sentiment. The announcement that Kim Jong Un will meet with Donald Trump has improved risk appetite and seen safe haven flows turn negative, meaning the yen has weakened. This means Dollar/Yen has jumped early in the session in a move that has breached the eight week downtrend. Although some of the early gains have faded, it will be interesting to sell if this rally is a sustainable move or whether it will be sold into again. An initial breach of resistance at 106.35 will have been welcomed by the bulls but a change in trend would need a breach of 107.65 at least, and above 107.90 to be confirmed. Initially the RSI and MACD lines have ticked higher but far more needs to be done to continue the improvement. The 106.35 pivot now becomes supportive today and the market has Non-farm Payrolls to contend with. Initial resistance is the overnight high at 106.95 and then 107.10. Yesterday’s low at 105.87 now becomes a near term higher low and is added importance. Given how reactive this pair is to payrolls, the outcome of today’s session could be crucial for the near to medium term outlook.

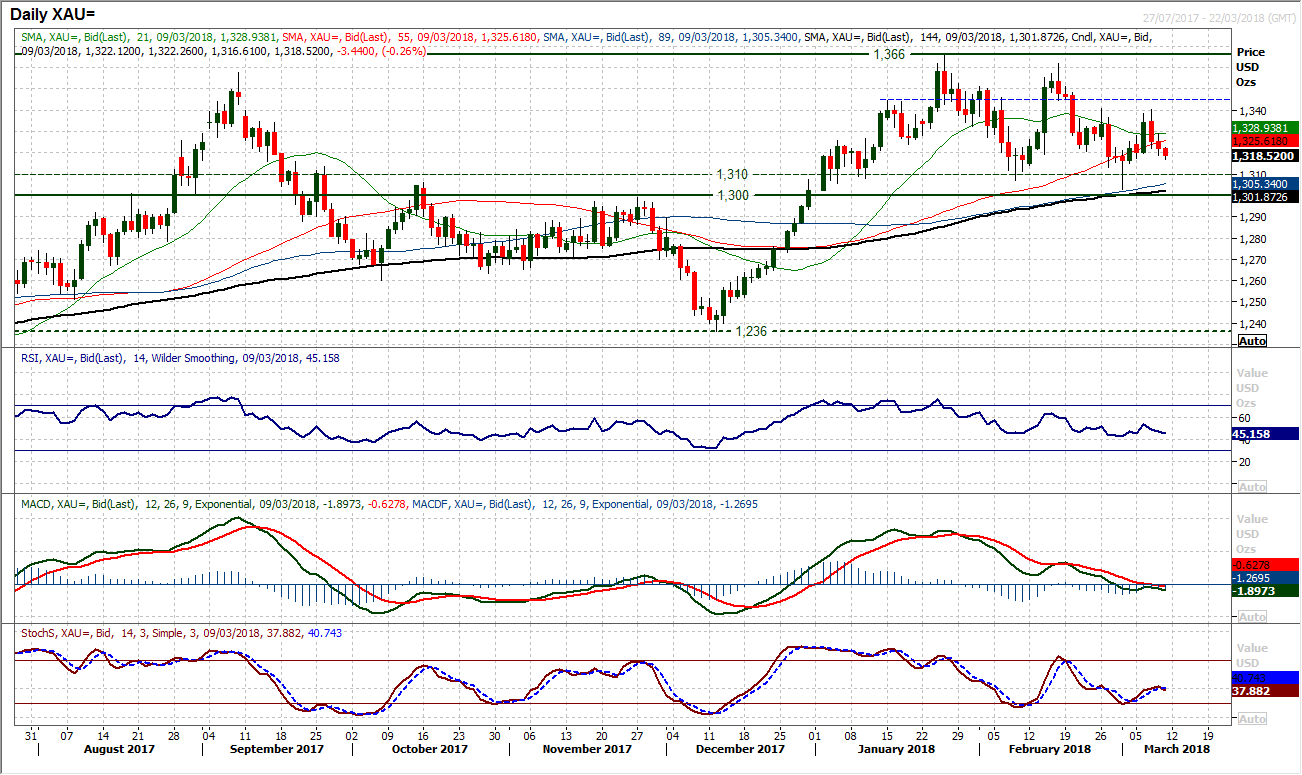

Gold

A strengthening dollar is weighing on gold once more, but it is becoming apparent that the market is unable to sustain a solid trend now. With the recent rebound fading at the resistance around $1341 a run of negative candles is building up as the move is reversing. Momentum indicators are neutral at best but are threatening to take on a slight more negative bias again. The near term support at $1317 Is creaking and this is something that is preventing a retreat back into the key long term pivot band at $1300/$1310 once more. The hourly chart shows a run of lower highs and lower lows building, with $1322 initially and then $1329 resistance. How the market responds to the volatility of payrolls today could be key to the outlook. The Average True Range on gold is currently around $13.

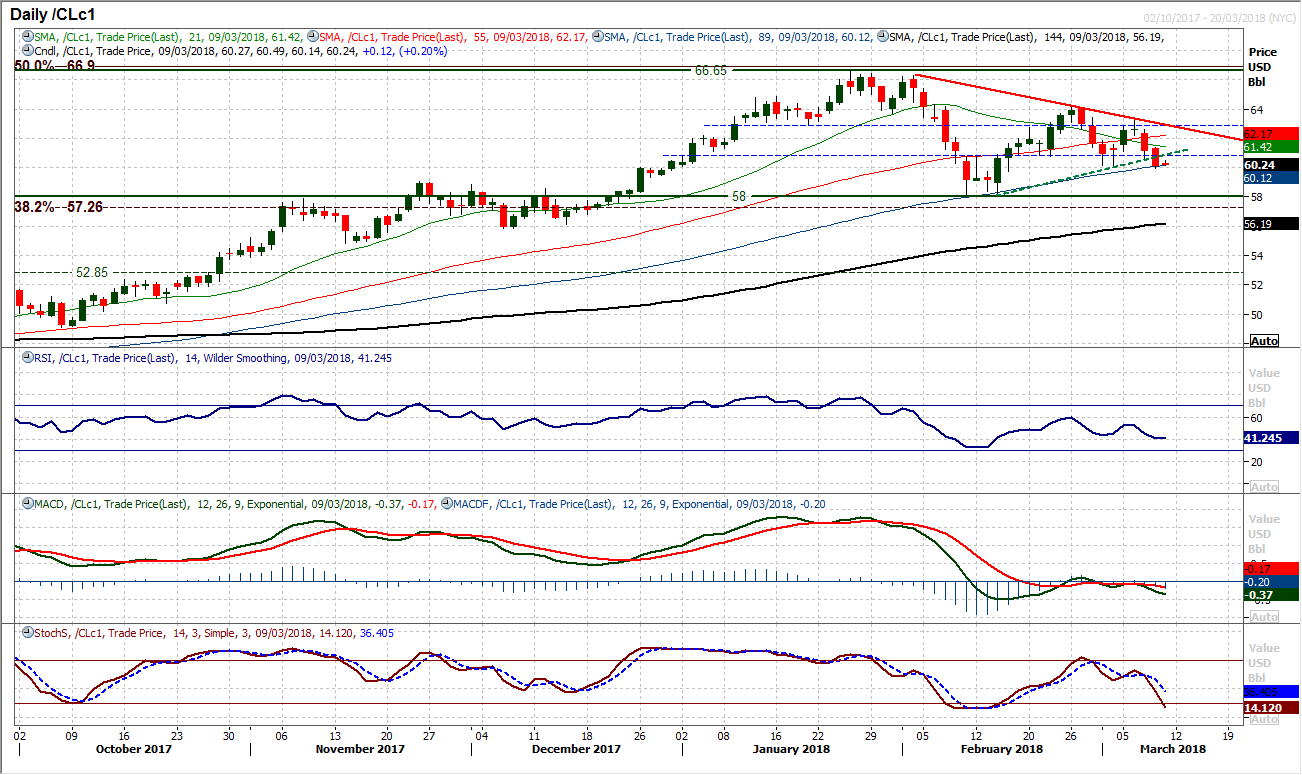

WTI Oil

The bears are looking stronger again as the market has broken down from a four week symmetrical triangle. A second consecutive strong negative candle has also breached the support of the early March low at $60.20 which on a closing breach now opens the key February lows $58.10/$58.20. There is a deterioration in the momentum indicators with the RSI finding downside traction at a three week low and the Stochastics also ticking decisively lower. The hourly chart reflects this deterioration with the market posting a series of lower highs and lower lows, trading under all the moving averages and with negative configuration on momentum indicators. This shows the market now selling into intraday strength, with near term resistance $61.10/$61.45.

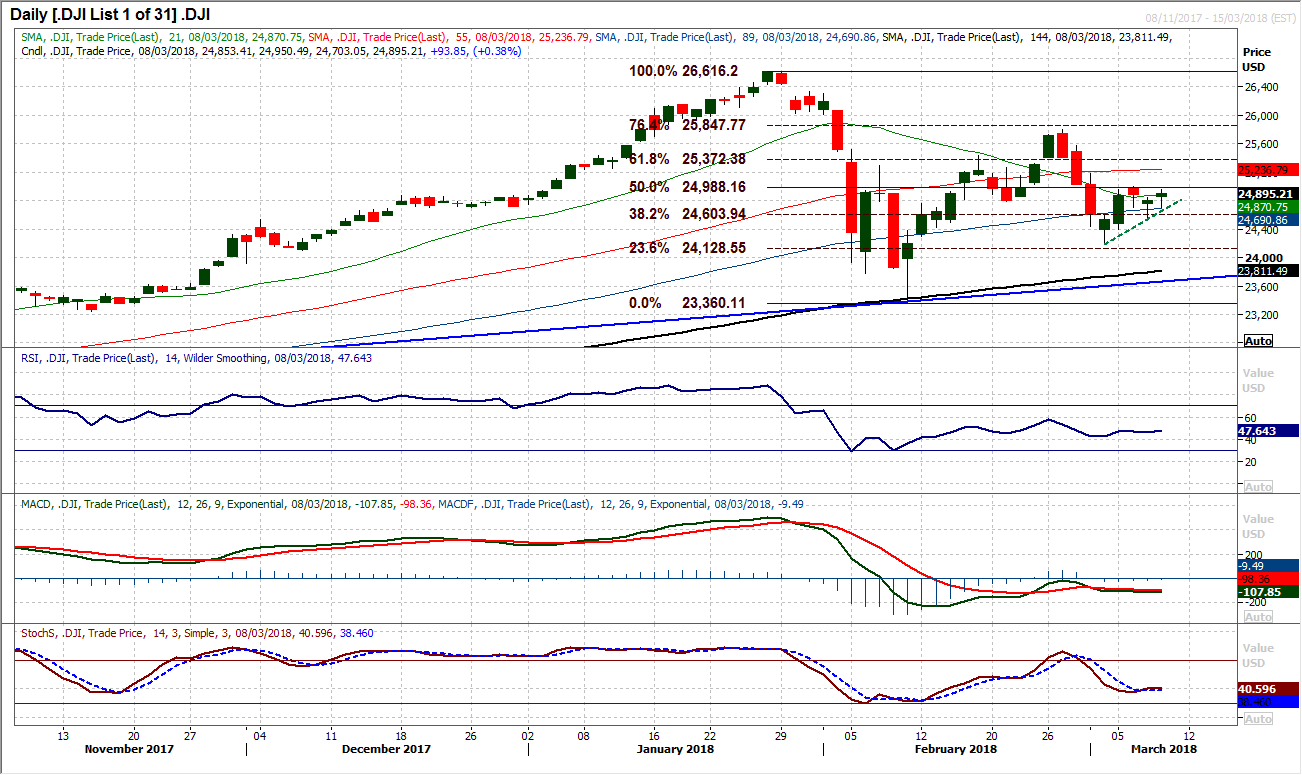

Dow Jones Industrial Average

The volatility of February continues to recede as the market closed yesterday with a daily range of just under 250 ticks, well below the Average True Range of 411 ticks. This subdued but positive session means that the Dow continues to trade below the resistance of the 50% Fibonacci retracement at 25,988 which has capped the gains throughout this week. The hourly chart shows how the market has been consolidating, with the RSI oscillating between 40/60 and the MACD lines hovering around neutral. Near term direction will be taken from a break above the 50% Fib level, with a consistent 26,000 handle a decisive move. The 38.2% Fib level at 24,603 is a basis of support that needs to be breached. Either level broken on a closing basis would drive the direction.

Author

Richard Perry

Independent Analyst